David Card has a new study arguing that immigration has basically no effect on the wages of domestic low-skilled workers. This confirms his earlier results on the famed Mariel boatlift, when Castro freed 125,000 Cubans to flee to Miami.

Is this result theoretically possible? How can the supply of labor increase, but leave wages unchanged? Card has little patience for these questions:

As the evidence has accumulated over the past two decades that local labor market

outcomes are only weakly correlated with immigrant densities, some analysts have argued that the

cross-city research design is inherently compromised by intercity mobility of people, goods, and

services. Underlying this argument is the belief that labor market competition posed by immigration

has to affect native opportunities, so if we don’t find an impact, the research design must be flawed.

A better answer, though, would have been to go to the blackboard. Card’s results are theoretically possible. All that is necessary, as Figure 1 shows, is that labor demand be infinitely elastic, i.e., horizontal.

Figure 1: Infinitely Elastic Labor Demand

Notice: When the Supply curve shifts out, the quantity of labor sold increases, and wages stay the same.

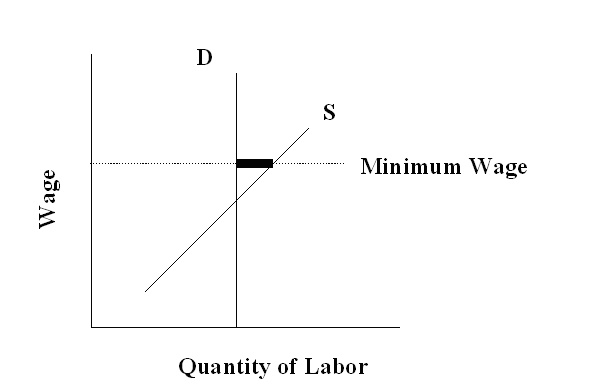

But this gets me thinking. Card is of course the co-author, with Alan Krueger, of the legendary study of the fast food industry in Pennsylvania and New Jersey showing that the minimum wage does not reduce employment. Their book goes further, debunking earlier studies that found the opposite.

Is this result theoretically possible? How can the minimum price of labor increase, but leave employment unchanged? Let’s go back to the blackboard.

In turns out that Card and Krueger’s results are theoretically possible too. All that is necessary, as Figure 2 shows, is that labor demand be infinitely inelastic, i.e., vertical. (The thick horizontal line between S and D at the controlled price is a labor surplus, but note that the quantity of labor purchased remains unchanged).

Figure 2: Infinitely Inelastic Labor Demand

Notice: When the minimum wage goes up, workers want to sell more labor, but employers want to buy just as much as before.

David Card has a higher IQ than me. He taught my graduate micro class, and put me in my place, fair and square. But taken together, I have to conclude that his research on immigration flatly contradicts his research on the minimum wage. His results for immigration imply that labor demand is infinitely responsive to price; his results for the minimum wage imply that labor demand is not responsive to price at all.

You could say that my former teacher has two sets of results for two different kinds of markets. But in both cases, he’s focused on markets for low-skill labor. Lots of immigrants from the Mariel boatlift presumably got jobs at McDonald’s. He’s not looking at two different markets; he’s looking at roughly the same market from two different angles.

What gives? I think Card’s work on immigration is closer to the truth than his work on the minimum wage. But it’s not because the immigration studies are well-done and the minimum wage studies are not. The quality of Card’s empirical work is uniformly high. I simply find his results for immigration more intrinsically plausible.

Why? As a theoretical matter, demand is highly inelastic under two main conditions:

1. Total expenditure on the good is a small fraction of one’s budget.

2. There are no good substitutes for the good.

In the market for low-skilled labor, neither assumption is credible. Labor expenses are usually the main cost of doing business. And you only have to peek over the counter at McDonald’s to see how easily machines can replace men.

These simple observations are the main reason why I think immigration does not reduce domestic wages much, and the minimum wage has a substantial employment cost. It would take pretty strong empirical evidence to change my mind. A bunch of studies finding that labor demand is either infinitely elastic or infinitely inelastic don’t come close.

READER COMMENTS

spencer

May 20 2005 at 8:49am

“peak over the counter at McDonald’s to see how

easily machines replace men”

This is the entire problem with your analysis of the impact of the minimum wage– it ignores this possibility.

A rise in the minimum wage has 3 alternative responses, not one.

1. Fire the employee.

2. Raise prices.

3. Raise the employees productivity.

In reality all three happen and this is why

no one has been able to clearly demonstate the impact of a minimum wage hike.

As a society what we want is alternative three, give the employee more capital and so eliminate low productivity jobs by turning them into high productivity jobs.

You are looking at the world in a static context

while in a dynamic context there are many more alternatives.

Boonton

May 20 2005 at 9:50am

You could say that my former teacher has two sets of results for two different kinds of markets. But in both cases, he’s focused on markets for low-skill labor. Lots of immigrants from the Mariel boatlift presumably got jobs at McDonald’s. He’s not looking at two different markets; he’s looking at roughly the same market from two different angles.

Is he really? Here in NJ there appears to be quite a few immigrants doing contractor type work…building decks, painting, home improvement etc. The McDonalds are well manned by the slacker offspring of our native white yuppie class. There are some exceptions, Dunkin Donuts & some gas stations seem to be well manned by immigrants but I suspect many of them are family owned buisnesses with either owners working or their extended families pitching in.

As for substitution, let’s think about this. Only to a degree can McDonalds replace the workers with machines. The business is already highly automated with a lot of expensive capital. To add yet another labor saving machine will involve significant cost…how much gain would there be? If the min. wage was raised to $7/hr from $5 the differential in labor cost for a 40 hour week 52 week year is $4,160. Any capital addition to substitute machines will have to cost less than that per year to make sense. Keep in mind also that the min. wage is reduced every year due to inflation so the prospects of trying to sell a labor saving machine to a min. wage enterprise is even more difficult.

Wal-Mart is another example. How much room is there to really add a labor saving machine that would, say, restock goods on the floor? You’re talking about something that probably needs the intelligence of a Star Wars droid. Can Wal-Mart get that at less cost than it would suffer with a $2 hr increase in the min. wage?

spencer

May 20 2005 at 11:36am

Why would you expect a real world example to ever find that the supply of labor is either infinitely elastic or inelastic?

I find it difficult to even imagine how that could exist.

dsquared

May 20 2005 at 12:34pm

His results for immigration imply that labor demand is infinitely responsive to price; his results for the minimum wage imply that labor demand is not responsive to price at all.

Surely his point is that *both* his results imply that the supply curve/demand curve Marshallian partial equilibrium model is not a good way to think about labour markets?

And surely he’s right. In order to make all these statements about elasticity, you basically have to ignore the fact that labour is not bought and sold in a spot market. It is bought and sold on the basis of multi-period contracts (often implicit contracts with a large element of trust) in negotiations between people who have conflicting incentives and very little information about each other’s intrinsic qualities.

As a result it is not surprising that labour markets are not usually in spot equilibrium and thus that comparative static equilibrium models do not describe them well. And so Card’s two results are consistent and both go to show the same point; wages do not move to clear the labour market in response to a supply shift and demand does not move to clear the labour market in response to a wage shift, because the labour market does not, typically, clear at all.

(btw, on a technical note I think that you are grossly overestimating the substitutability of machines for men in unskilled tasks. The substitutability is likely to be radically different for different tasks, and the *marginal* elasticity of substitution would be the important one. Unfortunately, this marginal elasticity would quite possibly not exist as the production function for even something as simple as a hamburger would be very unlikely to be continuous, smooth or well-behaved in any other way.)

Asif Dowla

May 20 2005 at 1:06pm

Bryan:

One could easily generate the result of figure 2 by assuming monopsony in the labor market. If the policy maker sets the minimum wage where the Marginal Factor Cost curve intersect the labor demand curve you will get the result of same employment without the highly suspect assumption of infinitely inelastic supply curve. Maybe your teacher was assumping the labor market for hamburger flippers are monosonic–not a bad assumption as fast food resturants are the major employers of these types of workers.

Ike Coffman

May 20 2005 at 2:05pm

Spencer writes:

A rise in the minimum wage has 3 alternative responses, not one.

1. Fire the employee.

2. Raise prices.

3. Raise the employees productivity.

There is also a fourth possibility: the employer accepts less profit. I am wondering if this response has not been considered because it is so rare, or is it simply unimaginable?

James

May 20 2005 at 11:52pm

This could happen too, no doubt. If one of the employers is a monopolist it’s not unlikely at all. A greater portion of the monopoly profits will go to wages. At a firm that’s bringing in an economic profit right around zero before the minimum wage hike, this isn’t a sustainable response.

James

May 21 2005 at 12:33am

Boonton,

McDonalds has recently been experimenting with kiosk style restaurants. I’ve never been to one. A friend of mine told me that they have one restaurant in MS that is totally automated. Machines make the food, take the customer’s order, the whole works. The building is basically a vending machine. When my friend ate there, he said the manager was in the back by himself not doing much of anything.

Such an approach may not present a cost savings over just hiring people. The order process, on the other hand, is cheaper to automate. A touch screen can take orders from 6am to midnight, 365 days a year. That’s 6570 labor hours, assuming a person is a productive as a machine at taking orders. At minimum wage, it costs more than $40,000 per year to buy that much labor. The costs of the order taking machine are less than half of that according this story.

Not much with present technology, but stock replenishment is only a tiny part of the labor cost of running a large retail chain. WM and several other large retailers have found that the checkout process, one of the larger chunks of the labor costs at a retail chain, is very easily automated. These have been common in Wal-Marts and Home Depots in Florida for at least the last three years.

spencer

May 21 2005 at 7:24am

“You only have to look over the counter at McDonal’s to see how easily machines replace men”

You write this as if it is a bad thing and a very undesirable outcome.

But as a society isn’t this exactly the thing we want to happen?

It is the way we raise productivity and our standard of living. Yet, you act as if this is a horrible consequence.

The Walmart example talked about a couple of times in the comments is interesting. Over the past decade retail productivity growth –lead by WMT — has been growing extremely fast — apparently faster then manufacturing productivity.

And parallel to this, average hourly earnings in retail as a percent of total average hourly earnings has been improving — after falling sharply in the low productivity era. This is what better productivity says should happen and is what

justifies improving real wages.

But the earlier comments on employment by WMT are in sharp contrast to this real record.

But it does raise some interesting guestions about how we achieve productivity growth.

We typically think about improving producivity

stemming largely from experience and on the job rtraing. Yet, WMT has over 50% labor turn over,

something very different from standard thinking.

WMT apparently achieves its strong productivity growth by breaking every job down to very small components so that experience or training does not matter.

Shivering Timbers

May 21 2005 at 7:27am

Once agian I am impressed to see far more insight in the comments than in the post itself. Dsquared, I think you’re right on the money, so I’ll avoid repeating you. But I will make one additional point:

When data fails to match the theory, there are two possible responses: either the data is wrong, or the theory is wrong. Data is subject to error, so it is reasonable to question it. But in economics, where the theories are (at best) extremely crude approximations and (at worst) nothing better than handwaving arguments, I’m surprised that anyone bothers to make an argument like the one we saw in this post.

Remember that as fundamental as it is to economic theory, nobody has ever actually managed to measure a real-life supply curve. As reasonable a construct as they seem, supply and demand curves may in fact be as accurate an approximation as saying that the stars are points of light affixed to a giant sphere surrounding the Earth. As an empirical and mathematical science, economics has yet to catch up to the level of Newton and Galileo.

Steve Miller

May 21 2005 at 8:34am

Spencer: “You write this as if it is a bad thing and a very undesirable outcome.”

I think you misunderstood him. :shrug:

Steve Miller

May 21 2005 at 9:08am

And isn’t that what perfectly inelastic demand means, that 100% of the wage increase is paid by the employer, with no reduction in the number of workers employed? The questions relevant to the Card/Krueger study are:

1) Is the new minimum wage especially binding? (If it is not, then one would expect Card and Krueger to be correct, that a modest increase in the min wage will not create much observable unemployment.)

2) Is the demand for labor especially inelastic in that market?

One potential problem with the studies done in NJ and TX at fast-food restaurants is that only employment at those surveyed restaurants was measured. Employment increased at those restaurants after the min wage increase — okay. But in both NJ and Texas after the 1990-91 min wage increases, teenage unemployment increased. That suggests only that the wage wasn’t binding, or labor demand was less elastic, or increased overall, in the fast food industry, but not among other minimum-wage employers. The overall effect was still an increase in unemployment among low-skilled workers.

James

May 21 2005 at 3:55pm

dsquared,

All of this is true of bond futures.

Yep. No one will buy or sell less than the going lot size.

The conflicting incentives are the whole point of exchange. Each side values what he receives more than what he parts with.

Again, just like the market for bond futures. Do you believe that bond futures markets clear?

dsquared

May 22 2005 at 1:03pm

Sadly, unlike futures contracts which are created ex nihilo and extinguished by a reversal of the trade, workers can neither be created at the drop of a hat nor vaporised when not required. Among other points of difference.

Bernard Yomtov

May 22 2005 at 2:42pm

Sadly, … workers can [not] be vaporised when not required.

Having once had an employer who decided I was not required, I don’t really consider this to be a sad situation.

Otherwise I agree with D^2, and find him unusually mild. Among other things, it is my impression that one of the functions of a futures exchange is to eliminate the risk of trading with someone about whose “intrinsic qualities” we know nothing.

Dan

May 22 2005 at 6:22pm

D^2,

So is it the inability of workers to be created and vaporized at will that prevents labor markets from clearing or are you just sidstepping James’ (successful) rebuttal?

James

May 22 2005 at 8:12pm

Dsquared,

My initial point was that the market for bond futures has all of the same characteristics that you use as evidence that labor markets don’t clear.

I suppose now you mean to say that labor markets don’t clear like themarket for bond futures because, according to you, futures contracts are 1) created ex nihilo, 2) extinguished by a trade reversal, 3) characterized by other points of difference that you don’t mention.

Trouble is, 1 and 2 only differentiate labor markets from futures markets if you start with misunderstandings of both. Re: 1, Futures contracts are created out of the ability to bear risk and the demand for a means to transfer that risk. Labor contracts are created out of the ability to work and the demand for the outcome of labor. Re: 2, Futures contracts are aren’t extinguished when a trade is reversed. Ownership just changes hands, or delivery of the underlying takes place. Unless you believe that destroyability of a good is a precondition for a market to clear, the bit about vaporizing workers is a nonsequitur. The good exchanged in the labor markets is labor, not laborers.

I suppose we could argue the finer points of how the market for bond futures differs from the market for labor, but I’m a bit pessimistic as to whether it would bear fruit. Here’s an idea: Just tell us what the necessary conditions are for a market to clear or, depending on which list is shorter, to not clear.

Bernard,

Yes, one of the benefits of some exchanges is guaranteed delivery regardless of counterparty. Is it your belief that labor markets don’t clear because of uncertainty between employers and laborers?

Bernard Yomtov

May 22 2005 at 9:17pm

James,

I don’t profess to know why labor markets clear or don’t clear. My point was simply this: in labor markets it is relevant that the parties know little about each other’s intrinsic qualities. In futures markets it is not relevant. Hence your analogy between labor markets and futures markets is inaccurate, silly even, for that reason among others.

James

May 23 2005 at 12:14am

Bernard,

If by “in labor markets it is relevant that,” you mean relevant to whether or not labor markets clear, your first sentence contradicts your second. If you mean relevant to something else, you’ve addressed some argument other than the one I’ve made.

I picked bond, rather than corn, futures in the original example because any guarantee by the exchange only pertains to delivery of the underlying. The actual value of the underlying debt instrument depends on the issuer whose “intrinsic qualities” remain unknown to both sides of the trade in the derivative market.

Bernard Yomtov

May 23 2005 at 10:56am

James,

There is no contradiction. The relevance is to the behavior of labor markets. Whether it affects the specific question of clearing, I don’t know, as I said. Perhaps a simpler way to say this is that labor markets are more complicated than futures markets by far, despite your attempt at treating them as equivalent. So the sort of simple analysis applicable to futures market may not give a satisfactory picture of labor markets.

As for your selection of bond futures, I see no difference between that and corn futures. Any change in the value of the underlying due to a change in the quality of the issuer, or anything else, will be reflected in price changes between the transaction and delivery. The danger is an adverse price change during that period. So is the danger in a commodity futures contract.

The risk involved in holding the underlying asset after delivery has nothing to do with the futures contract.

Patrick R. Sullivan

May 23 2005 at 12:33pm

Rather obviously labor demand is elastic. McDonalds is now ‘outsourcing’ the order taking. Supermarkets have self-checkout where the customer scans his purchases and feeds his money into a machine.

But the Card-Kreuger study always struck me as silly. They merely called fast food restaurants and asked whoever answered the phone how many jobs there were at the restaurant. That’s not information worth having.

Even hours worked would be insufficient, as you can squeeze more productivity out of a work force by closer (and more demanding) supervision.

And, if the new minimum is still below the market wage, it’s moot.

Mr. Econotarian

May 23 2005 at 1:32pm

The addition of immigrants into a community creates many new jobs through stimulation of novel niche demands (think tacos, pupusas, and pollo campero) as well as increase of existing demands (clothing).

dsquared

Jun 9 2005 at 2:41am

James, futures markets clear automatically by definition. Futures contracts don’t exist until they are bought and sold and aren’t produced.

In any case, futures contracts are standardised to quality and quantity (workers aren’t) and workers are part of the production process (futures contracts aren’t). I have no idea why you claimed that the purchaser of a bond contract has as little information about the commodity he is buying as an employer of labour since this is so transparently wrong. I made a flippant remark because I thought your analogy was so wildly off base.

Futures contracts aren’t “multi-period contracts”, by the way; they expire on a specific settlement date and their term is typically very short relative to the production period.

Comments are closed.