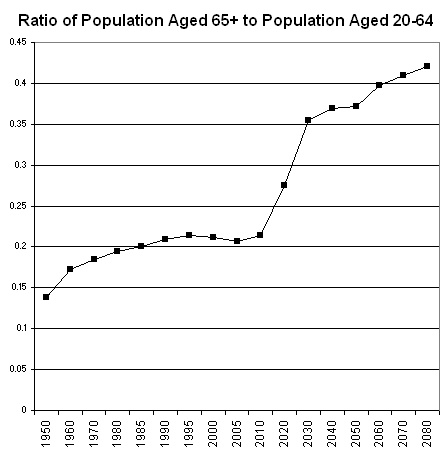

People who are freaking out about the rise in the dependency ratio will normally point to the fact that the ratio of retirees to the working-age population is going to sharply rise. The following graph, taken from Social Security Administration projections, makes it easy to side with the pessimists.

As you can see, by this measure, the dependency ratio has been getting worse for decades, and will approach .4 by 2030.

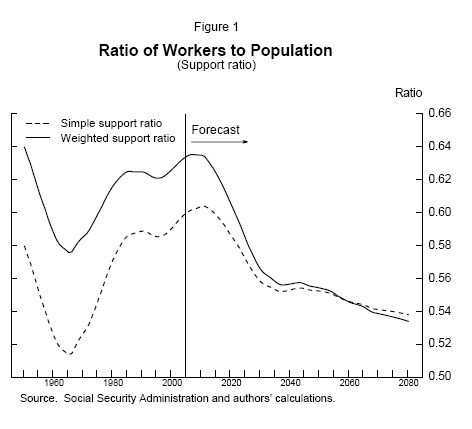

However, the picture looks very different if you compute the more economically meaningful worker-to-population ratio, as Sheiner, Sichel, and Slifman did in the graph below.

By this measure, dependency has been declining for decades. Yes, dependency is going to start increasing, but it will start increasing from an all-time low. In 2030, we’ll effectively be back at the dependency level we had around 1965.

Unless something changes, the second graph shows that dependency will continue to rise throughout the 21st century. But by historical standards, it should be quite manageable even in 2080.

READER COMMENTS

Buzzcut

Jan 28 2008 at 2:25pm

It will be quite managable into 2080 IF productivity growth in 2080 is as strong as it was in 1965.

Is that a good assumption? Kurzweil would say yes. Me? I don’t know, the 1960’s were a special time, one that the economics profession cannot really explain as to WHY the economy was so good in the 1960s.

Sara

Jan 28 2008 at 2:38pm

I wonder though if we aren’t trading “cheap” dependents, kids and women, for more expensive ones. For instance, health care is enormously more expensive for the elderly than for children or young women. Also, children and non-working spouses co-habit with workers while the elderly expect to live in their own homes, drive their own cars, etc.

Sebastian

Jan 28 2008 at 2:42pm

I’m not sure I understand how the characteristics of ‘worker’ change over age with this gragh. Does ‘part-time’ count for example?

Also I see this is the report: “But we

assume that, for the future, consumption weights by age group will be constant, implying

that any increases in elderly health spending are offset by reductions in elderly nonhealth

spending. If society instead chooses to spread the burden of higher elderly health

spending across different age groups, then increases in health care spending will raise the

consumption of the elderly relative to the non-elderly and require a larger cutback in nonelderly

spending than implied by the numbers in our analysis.”

I think the assumption that the increase in elderly health care costs will be paid for by equally reduced elderly non-health care expenditures isn’t likely to hold.

Sara

Jan 28 2008 at 2:51pm

Argh..now I see what that “weighted” means, nevermind. I must read more carefully. Although I agree with Sebastian. The probability that we will “[choose] to spread the burden of higher elderly health spending across different age groups” is pretty darn close to 1.

John Thacker

Jan 28 2008 at 4:07pm

From the paper:

Ignoring the medical costs issue that they mention, this still treats homemakers and other stay at home parents as purely dependents, with only consumption but no production. The value of performing childcare, cooking, and other chores is nonzero. Overall, it’s more efficient to have both spouses working (or else one should quit), but that doesn’t mean that the production of someone at home is zero.

Also, Table 1 in that paper, “Steady-state Consumption Adjustments in Response to Population Aging,” has some really nasty large negative numbers for the column “percentage change in real per capita consumption required relative to 2005 baseline.”

Nathan Smith

Jan 28 2008 at 4:09pm

Much of the discussion in the previous post is applicable here, too. John Thacker and I pointed out that housewives may produce valuable homemaking services, so it’s too simple to treat women’s entry into the labor force as a pure gain and ignore its opportunity cost. Of course, the points about seniors being more expensive than kids is also valid.

I once worked with a huge data set… it was one of the federal government’s data sets, I ought to remember the name… on incomes. I had the task of projecting the lifetime incomes of American workers based on historic trends in income as a function of time, age, sex, education, etc. I tried to do so using various kinds of regression analysis to derive coefficients on various terms which were assumed to be determinants of incomes. I made a strange discovery: if any interaction term between time and age was included, old people dominated the income distribution in the medium-term future. That is, if the coefficient of age as a determinant of income was allowed to vary with time, within the next few decades a large majority of incomes will be earned by the old, e.g., people over 55 or 60. I tried to manipulate the numbers to suppress this strange result, and could do so only by assuming it away by removing the year/age interaction term.

Maybe it doesn’t mean anything. But I can see a plausible story behind it. The economy is demanding less and less physical strength, and more and more human and reputational capital. As a result, lifetime earnings distributions will become more and more skewed in favor of the elderly. Already people are studying longer. It seems like a Masters is the new Bachelors. People place more importance on the human capital accumulation dimension of jobs, and the opportunities for upward mobility. Maybe in thirty to forty years, a lot of people will spend the first thirty or forty years of their lives, or more, in a sort of education/apprenticeship stage, which will involve both school and work, but which will be chiefly geared towards developing one’s mind and one’s connections and reputation, with a view to high earnings in one’s 50s, 60s, and 70s. The income distribution will look more and more unequal, somewhat misleadingly since much of this will be driven by age, but genuinely too, since by no means all people will have the foresight, discipline, and talent to become one of the well-paid cognoscenti who will earn the bulk of the income… and even some talented and disciplined people may just guess wrong about what skills and connections it will pay off to spend a lifetime developing. So there might be more pressure for redistribution among the elderly, from the few successes to the many semi-failures, who will not be unemployed, but who will miss the upwards lifetime income trajectory that will come to define the upper-middle class.

It’s a possible world. Anyway, it suggests that the dependency may decline, or at least not rise as steeply as projected, for a new reason: an increase in the retirement age, at least for the knowledge class, will be driven by the demands of the market.

John Thacker

Jan 28 2008 at 4:23pm

The paper suggests that we need an immediate increase in the retirement age by at least two years to avoid a 13.7% drop in real per capita consumption in 2025, and that waiting until 2025 to raise the retirement age by two years will still result in a drop by 10.8%.

I don’t see how this is so different from the pessimists. Yes, it’s very manageable if the retirement age is raised or if the rate in benefit increases is slowed soon. However, that’s certainly no reason to claim that there’s no problem, or that avoiding retirement age increases we could deal with the problem easily with much higher marginal taxes or giant cuts in benefits in 20 or 40 years, like so many of the “non-pessimists” seem to be claiming.

hector

Jan 28 2008 at 4:24pm

Another assumption is that people would retire at 65, it is very probable that in 2080, that will not be the case.

Cheers!

John Thacker

Jan 28 2008 at 4:28pm

Another assumption is that people would retire at 65, it is very probable that in 2080, that will not be the case.

It had better not be. We’re already talking about a 25% cut in real per capita consumption (not of retirees’ benefits, of everyone’s consumption) if we don’t do anything until 2040, according to that paper.

The problem is manageable in 2080 if we do something about it before 2080, yes. The paper is not consistent with a claim that the problem is manageable in 2080 if we do nothing about it before then. Raising the retirement age is the easiest way to do that. The paper strongly argues that we should do it now, not later.

Roper

Jan 28 2008 at 10:03pm

Social Security has been the greatest redistribution of wealth that the Modern world has seen.

The reason that Social Security works, is because it is taking money from a very large population and redistributing it to other people who qualify for the social program.

The great cog that keeps Social Security working is the baby boomers. Once the baby boomers begin to retire, their basic population will remain unchanged for quite awhile, and all that time, a much smaller population will have to provide the money to allow Social Security to work.

This is all fine and good as long as the baby boomers don’t stick around too long, but with that percentage of the population living to approx. 75 years of age, that’s a long time for not a lot of people to provide money to a large population. Especially when you compound the fact that the baby boomers earn a very significant percentage of the income in this country.

I do not see Social Security being around throughtout the rest of the 21st century, and I will be even more surprised if it lasts until 2030.

Ross Levatter

Jan 29 2008 at 12:12am

Roper: I do not see Social Security being around throughtout the rest of the 21st century, and I will be even more surprised if it lasts until 2030.

How is that possible? Were you trying to make some rhetoric point? How can your belief that SS will be gone by 2030 be STRONGER (“more surprised”) than your belief it will be gone by 2100 (assuming both beliefs are contemporaneous)??

I can’t graph this… 🙂

dearieme

Jan 29 2008 at 7:55am

The cost of the elderly can be reduced by adopting involuntary euthenasia – Sweden to be first, perhaps? As for the cost of Social Security for the USA: the USA won’t last forever – nothing does.

Michael Stack

Jan 29 2008 at 7:44pm

Maybe I’m misunderstanding but it seems there is a world of difference between sypporting dependents voluntarily (I’m thinking of children and spouses) and supporting dependents through the tax system. The former can provide an even greater incentive to work, while the latter is a heavy disincentive.

Bill Seitz

Jan 30 2008 at 10:31am

Given that the decline is based on women entering the workforce, and given that I believe that mean real *family* income has stayed flat over that time, I don’t see that buying any slack compared to earlier times.

Also, I wish that graph went back another 40 years.

Marty

Jan 30 2008 at 5:03pm

Ah, but we are so much more generous now, than we were in, say, 1960 (to pick the inflection point of the 2nd chart). Generous not only in absolute terms, but relative to average income and the economy.

The chart that matters is what percent of GDP or total personal income is being run through the social security system… I don’t have that handy, but the Social Security trustees do this in every annual report.

And, anyway, it’s Medicare, rather than old age pensions, that is the real long-term budget buster.

Mike

Feb 5 2008 at 1:22pm

This is nonsense. It means that people get to pay the same amount as they would if they had children— but they don’t get the children to support them in their old age.

Or, alternately, you could look at is people who do have children get to pay for both the children AND the seniors, a double whammy.

Comments are closed.