Categories:

Finance: stocks, options, etc.

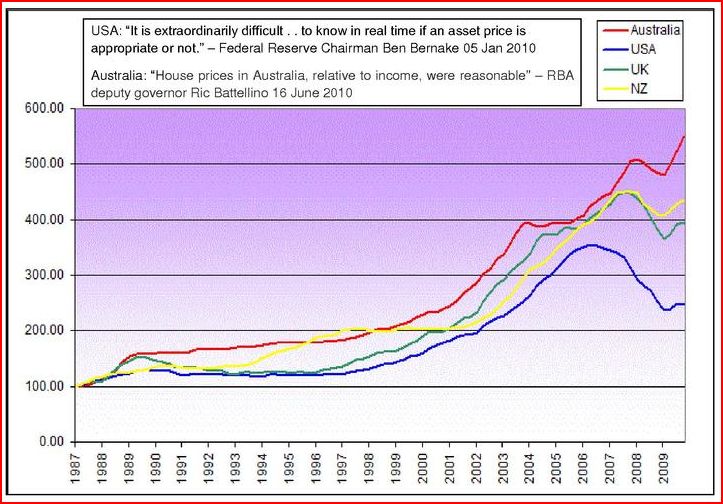

Knowing what you now know, suppose that you could pick one year between 1987 and 2010 to buy a house in the U.S. The catch: It’s a one-time deal, and you have to hold the house until 2010. When you’re not in real estate, you get the T-bill rate instead.

Do you buy at all? If so, when?

Once you’ve got your answer, take a look at Sumner’s graph, and see if you’ve got second thoughts.

{kind=link}

My answer’s in the comments.

READER COMMENTS

Bryan Caplan

Sep 7 2010 at 1:11am

Eyeballing Sumner’s graph, it seems like given the constraints, my decision to buy in 2000 was almost perfectly timed. I’m very glad I didn’t stay out – even after the price dip, I managed to keep roughly half of my capital gain.

Brandon Reinhart

Sep 7 2010 at 1:17am

I bought a house in Austin, TX around 2006. I think the decision turned out well, but had I known what was going to happen I might have gotten a much better price in 2008. I bought a condo in Seattle later in 2009 and am renting out the house. (Job relocation.)

After looking at the graph: great, I bought my house at the peak of pricing! Austin seems to have weathered the shock well and as long as I can find good tenants I’m planning on keeping the property…so although I bought at a bad time I feel like I have plenty of options.

I’m more worried about selling the condo. The Seattle market has been hit harder than Austin and there are a lot of properties on the market. I think it’ll take longer to recover here than in Austin and since I would like to move into a nicer house in a couple years I may be lucky to break even on the condo.

On the other hand, if I can rent both properties I think I’ll be in a strong long term position. People always need a place to live and I like to aggressively pay down my mortgages.

Staying optimistic in Seattle…

😀

Tim

Sep 7 2010 at 2:02am

Bought my house in 1998. Perfectly timed for the area I live in and the former owners made the idiotic decision of accepting my offer of their offer price immediately. They had three higher offers within days. And thus began the massive runup in house prices in my area.

The property peak at 4 times what I paid for it. It’s now only “worth” 3 times what I paid for it. Based in similar local sales within the last 6 months – that number appears accurate.

Liam

Sep 7 2010 at 2:04am

My guess was 1987 as I figured it had to be the lowest price. However I was 21 at the time and couldn’t even afford a carboard box. 🙂

I wish they had included Singapore in that graph. I would love to se how it fairs since there are two different real estate markets here. There is the Public Housing Market (~85%) where people can buy, sell, rent their 99 year lease and then the Private Property Market.

I used to own an HDB (Housing Development Board) unit and recently the price of those has been rising dramatically so that the Government recently introduced a Stamp Duty for all properties if sell in less than 3 years. Also if you buy an HDB you have 6 months to sell your private property. Even if that property is abroad. Though if you have a property abroad I don’t know how they would know.

geckonomist

Sep 7 2010 at 3:50am

And what would have been the return on the T-Bill rate investment since 1987 ?

Brian

Sep 7 2010 at 7:30am

It’s still early. Let’s see how you feel about this decision in 24 months.

mdb

Sep 7 2010 at 8:35am

I picked 1998, would have been the best year. I should say I started looking for my first house in 1996 (didn’t buy till 2001), so I had pretty good idea of when prices took off.

Sean

Sep 7 2010 at 8:39am

The trends might be clearer if you used a log graph.

mark

Sep 7 2010 at 9:57am

I guessed 94 which was the right time in my region. It looks like I did all right. But I have a big problem with all housing price measurements that show any kind of a profit to the homeowner. I believe they all vastly understate the cost of maintaining a house. I believe most people don’t properly account for that. I believe very few people truly make money on a house anymore. There was a period, when due to simultaneously favorable demographics and the expansion of federal support, a prior generation did. But I think that is gone for my lifetime. I believe housing is better viewed as a consumption good that you can resell in used condition, like a car.

Floccina

Sep 7 2010 at 10:00am

I bought in 1992 and that worked out very well for me.

Troy Camplin

Sep 7 2010 at 10:15am

Assuming the current price is what the market price should actually be at this date, then it looks to me like the bubble began around 2000. One might look at Fed interest rates around that time.

David R. Henderson

Sep 7 2010 at 10:37am

Bryan,

I don’t get it. You’re like the judge in a beauty contest who awards the prize to the first contestant he sees without seeing other contestants. What was the T-bill rate, as “geckonomist” asks? 1987 looks like a contender too.

Tim da Silva

Sep 7 2010 at 12:22pm

Bryan, I have to say that if we are looking at the same graph the “perfect time” was about 1997. It appears after that the graph moves up and consequently you are paying more for the same asset. The issue with all of this first is we don’t know the pay out of T-bills in ‘87,97,00 or any given year for that matter. An other issue T-Bill are not the same as housing. T-Bill’s as an asset are relatively safe and historically not been a toxic asset. The same can not always be said for housing(e.g if you bought a house in Las Vegas in 2007). Also you need housing(at least for a first house) for shelter whether you rent or buy( the same can not be said for T-bills). It would also be interesting to see what the difference was in rents relative to the same time periods. If for example they mimicked the housing graph and were relatively flat between 1987- 1997 then 1997 was the optimal time to buy.This is because it allows you liquidity up until that point, the price is still low and you don’t need to hold on to it for too long to see ever increasing returns that were flat in the ten years prior to 1997 . However if rent increases too much,it may make more sense to buy in 1987 and hold on.

-End Result: Much more data is needed!!

Sol

Sep 7 2010 at 4:47pm

Must say, this graph doesn’t look anything like the actual story with my house: purchased in 2001, sold in 2010 for about 70% of the 2001 purchase price (not factoring in inflation).

David Shemano

Sep 7 2010 at 6:22pm

Bought my house in 1999. It worked great because we cashed out a significant amount of stock for the down payment (roughly half of the purchase price), and the market peaked in early 2000. Therefore, we could not have purchased any later as real estate prices went up and the stock market went down.

John Turner

Sep 8 2010 at 12:07am

Based on inflation adjusted numbers I’d go with 1996 or 1997. The real increase in prices from 1996 to 2000 is about equal to the real increase from 2000 to 2010.

See here for graph.

Comments are closed.