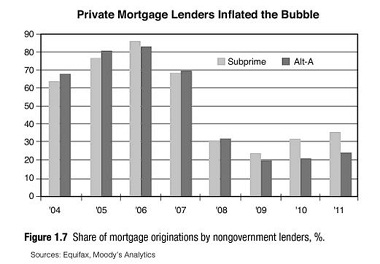

Trick question: None, zero, zilch. By law, Fannie and Freddie can’t originate loans–they can only buy or guarantee loans that have already been made by actors in the private sector. This is no small point, but it’s a point that Zandi leaves blurry at best in his book Paying the Price which I reviewed for Barron’s here ($ probably). Here’s a key graph from the first few pages of the book:

f mortgages aren’t originated “by nongovernment lenders” aren’t the rest originated “by government lenders?”

I’d probably expect to see Fannie and Freddie’s total book growing, with the private sector growing even faster. Fannie and Freddie light the fire, then the bubble-prone private sector takes it from there. The result? Fannie and Freddie’s holdings of new mortgage backed securities (MBS) would grow in dollars, shrink in percentages. Just like in real life:

READER COMMENTS

Steve Sailer

Dec 4 2012 at 11:44am

The housing bubble started to get out of control in 2004, but the catastrophic years were 2005-06. Fannie Mae was sidelined by accounting woes in 2004, but in either December 2004 or early January 2005 struck a deal with Angelo Mozilo of Countrywide to come flooding back in, leading to Countrywide’s January 13, 2005 press release promising a trillion dollars of lending to minority and low income buyers by 2010.

http://www.nytimes.com/2008/10/05/business/05fannie.html?pagewanted=all

Everybody wants to put a partisan or ideological spin on these events, but it’s gone largely overlooked that the man at the top, George W. Bush, accepted some blame for the disaster of his Ownership Society strategy in his 2010 memoirs:

“At the height of the housing boom, homeownership hit an all-time high of almost 70 percent. I had supported policies to expand homeownership, including down-payment assistance for low-income and first-time buyers. I was pleased to see the ownership society grow. …: This precarious structure was fated to collapse as soon as the underlying card—the nonstop growth of housing prices—was pulled out. That was clear in retrospect. But very few saw it at the time, including me.”

Bush appears to feel genuinely bad about how he messed up.

Floccina

Dec 4 2012 at 12:37pm

Those charts make the GSE’s look like suckers who came late to the game an blundered on.

kebko

Dec 4 2012 at 12:38pm

“But very few saw it at the time, including me.”

Yogi Berra, Thomas Friedman, and George W. Bush. They make it seem effortless.

Ann S

Dec 4 2012 at 12:55pm

In the late 1990s, Fannie and Freddie were publicly boasting about their success at inducing banks to lower their mortgage lending standards, and their intentions to keep working to get all banks to accept lower (eventually zero) downpayments, reduce documentation, etc.

Franklin Raines, head of Fannie, wasn’t saying that GSEs were trying to somehow crowd out private lenders through lower standards (which they couldn’t do anyway if they didn’t lend). His stated goal was to induce all US banks to adopt lower standards. He was publicly given credit for it at the time.

Ann S

Dec 4 2012 at 1:54pm

Your point about Fannie and Freddie not originating these loans yet still influencing their existence reminds me of a point I’ve seen made on the CRA (Community Reinvestment Act). Some people argue that the CRA couldn’t have had much effect because so many of the subprime loans were originated by, for example, Countrywide, which wasn’t subject to the CRA.

This ignores the fact that banks could satisfy the CRA requirement by buying loans originated by others, and Countrywide advertised certain loan pools as having been designed to satisfy banks’ CRA requirements.

egd

Dec 4 2012 at 2:02pm

“Bush appears to feel genuinely bad about how he messed up.”

And yet despite all the rhetoric of “not repeating the failures of the last administration,” there are plenty who are refusing to learn from his mistake.

Foobarista

Dec 4 2012 at 3:09pm

Frankly, in the old scheme, anyone with a bit of cash could originate loans. All you had to do was to provide enough doc to pass the various tests and F/F would buy the loan, generating you a nice profit of a few percent. There were millions of storefront mortgage operations across the country that originated loans and sold them by the truck-load to F/F.

The key here was you could effectively massively leverage your available cash, since F/F would buy your note quite quickly, so the interval your cash was “out” was often just a few days (between when you paid the seller and when F/F bought your note, and you always knew if F/F would buy it ahead of time, so there was no risk).

This system is still basically in place; all we’ve done is make the conditions for loan origination harder. Some storefront loan shops still exist, and a few are doing quite well. What made many of the existing storefront operations go out of business wasn’t the RE crash itself, but the crash in mortgage origination, as well as the fact that many of the people running such businesses drank the RE Kool-aid even more deeply than others and got killed there.

Note some useful elements of this business model:

1. Expensive loans are better than cheap ones. F/F paid more for subprime loans than “good” ones. This is why many people who qualified for good loans got sold subprime ones.

2. Interest rates on loans didn’t matter.

3. Other than meeting F/F loan requirements, nothing else mattered about the loan terms, the property, the buyers, etc.

Steve

Dec 5 2012 at 12:06am

Didn’t the F&F loans outperform private lenders? And didn’t the banks lie about the lending standards for many of the loans? What happened in the housing crisis is not hard to figure out if you are willing to accept that sometimes things are not the government’s fault.

Joshua Wojnilower

Dec 5 2012 at 2:26am

Ann S makes a very good point regarding the influence of Fannie and Freddie in lowering lending standards (which I suggested recently regarding the FHA). During the late ’90s and early ’00s, the govt was clearly trying to induce the private sector to lower credit and down-payment standards by providing “buyers of last resort”.

@Steve,

Banks did clearly lie about credit-worthiness for some mortgage, but the question is why? Under normal circumstances, a bank is concerned about the credit-worthiness of a borrower because the risk of default represents a potential cost to the lender. During the housing boom, mortgage originators were willingly falsifying borrowers’ data (e.g. NINJA loans). Had the private sector expected to absorb those costs, it’s unlikely such practices would have taken place on a massive scale. However, since F&F were presumably willing purchasers if times got rough, the losses were expected to be absorbed by the public sector. The expectation of guaranteed liquidity would be expected to increase risk within the system.

Aaron Phipps

Dec 5 2012 at 1:52pm

Thanks Garett. I’ve heard many arguments along these lines but with improper data to support them.

@Steve and @Joshua, I would only add that, in my opinion, the fault of these NINJA loans still can’t be placed entirely on the existence of F&F. True the incentive structure was wrong, but banks still made bad loans. However, the solution comes from changing the incentive structure.

Stefan

Dec 6 2012 at 4:03pm

Much of this information and most of Zandi’s analysis misses the point entirely.

First, the bubble didn’t begin when it popped. It began when it was first inflated. That began in the mid to late 1990s.

Second, it hardly matters that Fannie and Freddie lost market SHARE in a rising market. They were still the top two mortgage securitizers with the next largest private label in a distant third place. They securitized more mortgages than the top ten private labels combined.

Third, it does not matter whether the loans they purchased and securitized were higher quality. They were the market leaders and thus got the choice cuts. The private labels were stuck with the residual market. Also, when the GSEs purchased mortgages, it infused the financial system with liquidity both in the primary and secondary markets. With this liquidity, private players took on riskier loans. So the sale of high quality mortgages subsidized the low quality mortgages.

Also remember that the housing market doesn’t care if the buyer is armed with a conforming loan or a NINJA loan – both loans contribute to the demand and hence price of the same houses.

The affordability features that were begun in the Clinton HUD grew in use. Rather than make an average home affordable to people with modest incomes, they permitted people to bid up house prices to beyond their ability to repay or refinance.

The Federal Home Loan Banks, also GSEs, provided funding to banks to meet affordable housing goals. And as Ann said above, even lenders who were not subject to CRA received subprime credits or other financial gains by originating these loans and selling them, largely to F&F.

As Steve says, F&F were embroiled in accounting fraud investigations from 2004-2006, and that inhibited some of their participation. Still, they held the vast majority of whole mortgages and MBS – more than all 8000 or so commercial banks combined.

As Ann said, F&F were bragging in 1999 about exceeding their affordable mortgage goals and planned to increase it more. And they did lower their mortgage standards near the bursting of the bubble.

They were hardly bit players, and these charts mask their incredible market power. If they had been private firms, the FTC would have been suing them for anticompetitive behavior.

George Bush’s regret is exactly correct. He and his predecessor deserve blame for pushing home ownership as a national policy, permitting dangerous mortgage products, and indirectly providing liquidity through GSEs. This was a government caused crisis. The private sector, as stupid nd greedy as they were, responded to the incentives government gave them. Everyone who got cash for a clunker, got the home buyer tax credit, or put solar panels on their roofs were also responding to incentives that altered their cost-benefit analysis on capital expenditures. Same thing with the housing crisis.

Comments are closed.