Categories:

Fiscal Policy

Macroeconomics

We’re still debating how extra government spending influences the short run economy. How it influences the long run is a more important question but that’s a topic for another blog post.

Recently there’s been some buzz that multipliers are on the big side. At the American Economic Association Meetings, Yglesias had this to report:

Two papers I saw presented this morning took very different approaches to reach a similar conclusion–inside a currency union there can be big fiscal policy multipliers.

How big are the multipliers in these papers? How much is an extra dollar of spending (or an extra dollar in tax cuts, or a mix) predicted to boost short-run income?

Paper 1, coauthored by IMF Chief Economist Olivier Blanchard, who is always worth reading, finds that in the years since the financial crisis, the multiplier in Europe is about 1.0 units larger than previous estimates. But since previous multiplier estimates were so small, the new multipliers they find are still modest. An IMF report that builds on this paper infers that “multipliers have actually been in the 0.9 to 1.7 range since the Great Recession.” I’ll call this 1.5 to be on the safe side.

So an extra dollar of austerity (some mix of tax hikes and spending cuts) shrinks the economy by $1.50. (Wonkish: They used a wise, clever methodology based on forecast errors). Crudely, you could sum up their result by saying that when government shrinks by a dollar not only does the private sector fail to rehire those workers quickly, but the private sector actually shrinks by an extra $0.50.

Paper 2, by Daniel Shoag, looks at differences in spending across U.S. states. His estimating trick, a good one, which I’ll summarize with intentionally provocative language: Some states were in a good position to raid pension coffers during the financial crisis, so they did. That meant fewer immediate spending cuts, fewer immediate tax hikes. Since “ability to raid” is partly a matter of pure luck, it’s a decent natural experiment.

Shoag found that an extra dollar of government spending raised in-state income by $1.43. A multiplier of 1.4.

My view: 1.5 and 1.4 are not big multipliers. If a dollar of government spending or tax cuts genuinely boosted the short run economy by two or three dollars, I’d call that big: At that point, even if the government spending was purely wasteful, you’d be substantially growing the private sector in a big, obvious way. A prominent freshman economics textbook by Case/Fair/Oster says that “in reality, the multiplier is about 2,” but reality has been disagreeing with that assessment lately.

A multiplier of 1.5 or 1.4 is unimpressive as a grand argument for stimulus. Three reasons:

1. Deadweight loss of future taxation. We’ve gotta pay for this stuff someday, and actually-existing taxes distort.

2. Hurried stimulus is bad stimulus. Don’t forget the tiny tiles.

3. The flypaper effect and other public choice-style distortions caused by stimulus. (True confession: I would’ve rooted for ARRA had it included a permanent moon base.)

And a meta-reason for seeing 1.5 and 1.4 as “not big”: Both of these studies are based on crisis and post-crisis time periods—precisely when Keynesian spending multipliers are supposed to be at their biggest. If these are the big numbers….

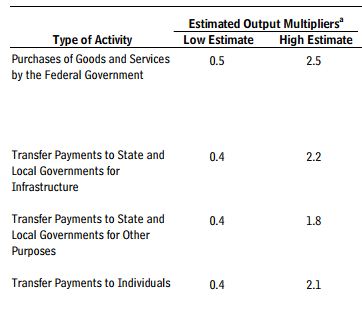

But we don’t have to go by my personal views on what is “big,” or in Yglesias’s terminology, “high.” We can use the CBO’s views on the subject. Here are their high and low multiplier estimates for the four fiscal actions with the biggest short-run bang for the buck:

That’s a great thing about CBO: They give a range, they admit their uncertainty about their multipliers. And notice that in all four cases the “high” estimates–2.5, 2.2, 1.8, 2.1–are bigger than the values of 1.5 and 1.4 that recent studies found in the US and Europe.

And remember: The two studies Yglesias reports are based on the effects of stimulus and austerity during and after the financial crisis, the precise time when economic slack is supposed to massive, the precise time when the government should be able to snap up unemployed workers quickly, the precise time when surprise layoffs should send multiplier shockwaves through the economy.

And still, these two new studies presented at the American Economic Association meetings found multipliers that were medium in magnitude. Austerity shrinks the economy modestly in the short run; stimulus grows the economy moderately in the short run.

Modest, moderate, medium: These are words we should associate with the short-run effects of stimulus and austerity.

Open Economy Coda: We can’t just evade the issue by claiming that states within Europe or the U.S. are open economies, so stimulus and austerity leak out, mostly impacting neighbors.

First, people cite these studies as evidence the multiplier is big without using caveats about trade. So let’s note that they’re not that big.

Second, trade isn’t as big as you think–for instance Greece only imports about 1/3 of its GDP (and exports less than that).

Third, stimulus in your state likely poaches workers, materials, and equipment from nearby states, exaggerating the multiplier. Every time an out of state truck delivers materials for a stimulus contract, that’s making the multiplier look bigger than it really is. When my uncle went to Alaska to help build the pipeline in the 70’s, he boosted Alaska’s GDP but didn’t boost Alaska’s GDP per person nearly as much. Open economy concerns cut both ways–so while states within Europe and the U.S. aren’t perfect laboratories, these labs aren’t obviously dramatically understating the size of the short-run multiplier effect.

If the multiplier were “big” or “high” one might well expect these kinds of studies to convince us.

[This post was edited to better reflect the Blanchard/Leigh multiplier estimate: The first draft of this post reported a multiplier of 1.1, now raised to 1.5.]

READER COMMENTS

David R. Henderson

Jan 23 2013 at 3:59pm

@Garett Jones,

This is an EXCELLENT post. When I teach multipliers, this will be on my reading list.

One little correction: I’m willing to bet your uncle did increase GDP per person. It’s simply gains from trade.

Garett Jones

Jan 23 2013 at 4:14pm

Thanks David! Good point on the gains from trade—I slightly rewrote that graf based on your comment….

Joe Weir

Jan 23 2013 at 5:34pm

Am I correct in assuming that the ranges presented in the CBO table are analogous to the lower and upper bounds of say a 95% confidence with the null value (1.0) inside the CI? If so, then there is a pretty good chance that the stimulus shrinks the economy in the short term. What were the CI bounds around the 1.1 and 1.4 estimates in the presentations cited above?

Arthur_500

Jan 23 2013 at 5:45pm

My only question has to do with “austerity.” Government cuts are referred to as austerity and

However, what is privatization?

It is a cutback in government spending replaced by taxpaying citizens doing the same job. You have gubment “austerity” replaced by efficiently delivered competitive services.

Will you lose inefficient employment? One would hope so. However, you would have eliminated all the costs, rents, equipment, etc and replaced them with revenue.

How does this austerity figure in the Keynesian multipliers?

john hare

Jan 23 2013 at 6:53pm

This post reminded me of a pet peeve from the stimulus years.

“Instead of giving all that money to bankers, the government should have just given all of us taxpayers a million dollars each.”

At least half of the people that said that would not be convinced that it was a bad idea. (I mostly avoid calling someones’ opinion stupid.)

The math just seemed to anger them. There were several variations that I heard, and I wonder how many others were out there.

libfree

Jan 23 2013 at 9:16pm

@GarettJones Isn’t there a marginal impact here? I would expect the first dollars of stimulus to be more effective than the billionth.

Andrew

Jan 24 2013 at 10:28am

Some day I hope to learn what that means…

Ken B

Jan 24 2013 at 10:56am

This is an excellent post. One follow up question. Is there a way to break out the effects of infrastructure spending from Martian War/tiny tile spending? My gut reaction is that tiny tile spending has a higher immediate multiplier effect (and larger long term cost) but I’m no economist.

MingoV

Jan 24 2013 at 5:31pm

I read a summary of a recently published paper (I don’t remember the reference) that found short-term multipliers of less than 1.0 and medium-term multipliers of LESS THAN ZERO for debt-funded government spending increases.

Joe Cushing

Jan 25 2013 at 12:42am

I can’t even look at another article about the multiplier. The whole idea of the multiplier is just ridiculous.

Comments are closed.