Categories:

Macroeconomics

Some theories of the business cycle say that booms and recessions are caused by shocks to the supply of key inputs: a wave of new high-tech ideas, a rise in oil prices, big changes in labor law. In supply-side stories, it’s easy to understand why a recession happens: You just can’t make as much stuff. Other “multipliers” or “propagation mechanisms” may amplify the effect but the first shock is to the supply side.

Other theories of the business cycle focus on shocks to the demand for goods and services: People get cautious, firms get worried, governments get terrified, so they hold back on spending. After hearing a demand-side story anyone who has taken a few weeks of economics should ask, “Why don’t businesses just cut prices and sell the same amount?” In response there are many tales of how it takes a while for businesses to cut prices even though there’s lots of unsold stuff on the shelves—stories of price rigidity, of sticky prices. In these demand-side stories–whether Monetarist, New Classical, or sticky-price Keynesian–stuff goes unsold even though workers are willing and able to supply inputs, even though firms stand ready to meet orders for goods. If firms and workers produced the stuff, it just wouldn’t sell: Prices are stuck too high.

I think both the supply side and demand side stories have a lot to be said for them, and real life is likely a mix of both plus some of neither, but that’s not what I’m here to write about today. Instead, I’m here to remind you that one popular brand of Keynesianism–sticky wage Keynesianism–should be lumped in with the supply side theories of recessions rather with the demand side theories. Sticky wage Keynesianism says workers hate wage cuts so much that businesses dare not cut wages, even in a competitive market. There are a lot of stories about why wages don’t fall during a recession revolving around fairness norms but I’m here to talk about the effects of that wage rigidity not the causes.

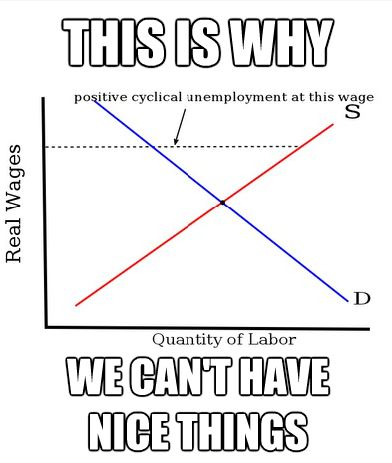

In sticky wage Keynesianism, demand for goods falls because of, say, bad news about the stock market. Since businesses want to sell stuff, rational individual firms cut their prices in response to bad news. But if firms cut their prices while keeping worker wages fixed, firms find workers more expensive than before–workers become more expensive in terms of goods. Because workers–a key input–become more expensive, firms rationally decide to produce less stuff.

It’s basic microeconomics: If the price of a key input rises, you’re quite likely to produce less output. That’s the heart of sticky-wage Keynesianism.

You can see now why it’s a supply-side theory: If, magically, some extra output showed up in a company’s inventory, in a sticky-wage Keynesian world it would sell and probably sell quite quickly because end users are starved for output: there’s no failure of “effective demand” for final goods in a sticky-wage Keynesian world. The reason there’s so little output during a recession according to sticky-wage Keynesians is because high wages make output too expensive to produce.

Sounds like a supply-side theory to me.

Yes, it’s a supply-side story that can be fixed by raising the demand for goods–by printing money, by ordering more government goods–but these solutions are ultimately Rube Goldberg devices for raising the price level so that workers become cheaper so they can go back to producing output. The core economic story in sticky-wage Keynesianism is about firms that are rationally deciding to produce less output not because of a fall in demand for goods but because of a rise in costs.

[Source]

{kind=link}

I think supply-side failures are important to the business cycle, and the sticky-wage Keynesian channel is one of those supply-side failures. But I’m no business cycle monocauser: I suspect there’s some straightforward demand failure going on during recessions as well.

For discussion: There are no overstocked shelves in a simple sticky-wage Keynesian world. Do you think we live in something a lot like that world?

READER COMMENTS

Rob rawlings

Mar 17 2013 at 11:27am

I have a question on “If, magically, some extra output showed up in a company’s inventory, in a sticky-wage Keynesian world it would sell and probably sell quite quickly because end users are starved for output”

Wouldn’t it only sell if firms further reduced the price ? And wouldn’t this cause firms to reduce employment further? The reason for the original price and output reduction was reduced demand so I’m not sure how increasing the stock of the good will help.

Garrett M. Petersen

Mar 17 2013 at 2:02pm

An interesting thing about this supply-side theory is that it suggests a supply-side solution. The “stickiness” of wages is not exogenous, it’s a consequence of institutions. Restrictive labour laws, unions, regulations that create barriers to entry for new firms, all these make it more difficult for wages to fall.

Garett Jones

Mar 17 2013 at 3:30pm

@Garrett: Indeed! One wonders why the unemployed workers don’t get hired by startups for 5% less, one hears stories about pride….

Rob: You’re right about the direction, but a quick calculation suggests that it’s possible for the price fall to cause only a small fall in supplied output…

The point I’d reemphasize is that no goods go unsold in a sticky-wage Keynesian (or sticky wage Monetarist) world.

Hazel Meade

Mar 17 2013 at 7:18pm

I’ve noticed this contradiction as well.

Liberals are constantly complaining that wages paid to middle class Americans have eroded since the 70s, and yet they advocate inflationary monetary policies that will erode those wages still further.

If you truly think that American workers are underpaid and should be getting pay raises, then you should be advocating in favor of gradual deflation.

Glen Smith

Mar 17 2013 at 8:03pm

5% less of what? In my field, the mediocre are the most likely to be employed.

perfectlyGoodInk

Mar 17 2013 at 8:25pm

Garrett M. Petersen: The “stickiness” of wages is not exogenous, it’s a consequence of institutions.

Partially. While prices of commodities can adjust easily, people tend to take a price as a measure of self-worth and are insulted by an employer who suggests they take a wage cut. This usually leads to them jumping ship or a drop in their morale and thus their productivity.

But this only explains wage stickiness, not price stickiness. I don’t find price stickiness anymore satisfactory an explanation than exogenous shocks everywhere. Both New Keynesian and New Classical paradigms to me seem hindered by adaptive/rational expectations where preferences and expectations are statically and independently formed rather than dynamic and socially influenced.

KnowPD

Mar 17 2013 at 9:05pm

I loved the post but I’m not sure how to respond because I don’t understand the question.

“I suspect there’s some straightforward demand failure going on during recessions as well.”

Agreed. However, I reject the crude Keynesianism of Krugman – i.e. all our woes are an absence of aggregated demand. The question, then, is where is the middle ground? I have seen no plausible arguments that in light of wage stickiness that the market would have unfulfilled demand, but perhaps I’m wrong. How does the market respond to wage stickiness? Is that what you’re asking? I have no clue..

Jim Rose

Mar 18 2013 at 3:57am

I always wonder why exogenous shocks in RBC theory was unacceptable yet waves of optimism and pessimism among investors and the animal spirits and sticky wages and sticky prices were not exogenous shocks in Keynesian theory?

Himanshu Sanguri

Mar 18 2013 at 2:08pm

Keynes theories are pragmatic in presence of a sound regulating body like a government or central bank. All the recessions till date, like US- 1930 and 2009, Euro recession have their breeding ground in the marsh of corrupt, impractical and loose economic policies. Demand and Supply equilibrium has always been tipped off as an aftermath, rather being the harbinger of recession. USA recession of 2009 was due to wrong policies of federal bank that disturbed all the dimensions of sound US economy like demand, supply, wages, employment etc. Same goes with Europe recession, that was propelled due to the bad fostering of newly born Euro zone.

Ekkehart Schlicht

Mar 19 2013 at 5:46am

You write:

“There are no overstocked shelves in a simple sticky-wage Keynesian world.”

This seems incorrect to me. If demand goes down and wages remain as they are, you get excess capacity: All firms would like to sell more than they do, and keep their workforce employed. This is precisely what we observe.

As an aside: it would be perhaps better to speak of sticky wages and prices here, because if there were flexible prices you would not observe excess capacity.

Keynes

Mar 20 2013 at 10:06am

[Comment removed pending confirmation of email address. Email the webmaster@econlib.org to request restoring this comment. A valid email address is required to post comments on EconLog and EconTalk.–Econlib Ed.]

Comments are closed.