If you hang around economists long enough, you’re bound to hear the word utility. They don’t mean it in the original (at least 500 years old), usefulness sense of the word, as in the utility of electric power to wash and dry clothes. They mean it in the late 19th century sense of “the instrinsic property of anything that leads an individual to choose it rather than something else” (Oxford English Dictionary).

In everyday conversations among students newly infatuated with economics, you’re likely to hear such phrases as “whatever gives you more utility” or “depends upon your utility”. Their jargon comes straight from classroom lectures on utility maximization, the theoretical workhorse of economics. Utility maximization is a model of choice in which a mathematical function for utility, representing an ordinal ranking of outcomes, is maximized subject to a given set of constraints. W. Stanley Jevons’ contribution to the marginal revolution in the late 19th century was to use utility maximization to explain why the price of water is low, even though it is absolutely vital for life, and the price of diamonds high, even though shiny stones are inutile for life. The revolutionary insight for resolving the apparent paradox was that it is not the usefulness of water or diamonds consumed in total that determines its value, but the intrinsic value from consuming the marginal (an additional) unit.

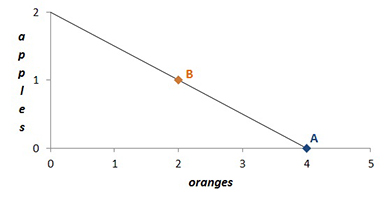

Consider the following example of this analysis at work. Suppose a consumer has a budget of $4 and is deciding how many apples and oranges to purchase.

The price of an apple is $2 and the price of an orange $1. Our consumer can choose to buy 4 oranges and 0 apples (point A) or 2 oranges and 1 apple (point B). (Of course, she also has the option of 0 oranges and 2 apples.) What will our consumer do? We presume she will pick the bundle that she considers the best for her. Suppose she picks bundle A. She could have chosen bundle B, but didn’t. She prefers 4 oranges and no apples to 2 oranges and 1 apple. Why she doesn’t want any apples, we don’t know and we don’t care. That’s between her and herself and not relevant to understanding consumer choice in markets. We could not predict ex ante specifically what she would do, but as economists say, our consumer has revealed her preference for oranges over apples (on this trip), subject to her constraints.

A key feature of this analysis is that it is ex post facto: we first observe what a consumer does, the outcome, and then based upon what has been revealed we can rationalize (by S. N. Afriat’s 1967 theorem) what happened with the existence of a utility function. Whatever this function is, the numeric value it yields with the inputs of 4 oranges and zero apples is greater than the numeric value with inputs of 2 oranges and 1 apple. Of course, economists also prove logical propositions by first assuming a utility function exists. What we assume when we do is that a person acts consistently in a way that can be rationalized ex post from observation.

This all makes sense and is the foundation for how we understand choice in markets. But then in the late 1990’s and early 2000’s when experimental economists moved away from studying markets to game theory, they regularly observed some odd choices in the laboratory. For example, 67% of people would choose $25 for themselves and $15 for another person over $40 for themselves and $0 for another person (replicated here). Suddenly, economists began to care what these people were thinking and feeling because all good economists rely on the axiom that people prefer more money to less money. Yet these people robustly revealed their preference for less money. As students of intermediate microeconomics are well aware, standard economic choice ignores such ordinary human considerations of fairness, altruism, inequality aversion, guilt, among many others. Economists were in crisis. Worse still, another study found that 97% of people chose $40 for themselves and $0 for another person over giving any of that $40 to another person. Yes, 97% (replicated here as 100%). Of course the experimental designs and protocols are drastically different in what precedes the final decision, but why the huge discrepancy? Sometimes people clearly care about more money to less and other times they do not.

Along came behavioral economists to the rescue. Their solution was fairly simple: augment the utility function with parameters to “reunify” psychology with economics. Sometimes people clearly don’t only care about money, so put in some parameters for fairness, altruism, inequality aversion, etc., that would generate more utility from being fair, kind, equitable, you-name-the-norm-or-sentiment.

For example, Ernst Fehr, Holger Herz, and Tom Wilkening in the June, 2013 issue of the American Economic Review examine “The Lure of Authority“. They conduct an experiment in which a principal can delegate or not to an agent the authority to choose a project. The projects generate different amounts of money. Do people have a preference for authority and power? Let’s summarize what they find in a similar, but rough graph:

Instead of apples on the vertical axis, either the principal retains the authority to pick the project (a = 1) or he does not (a = 0). On the horizontal axis are the real monetary payoffs associated with having the authority or not to pick the project. Fehr et al. find that in many of the decisions, well more than half, people choose bundle B over bundle A with monetary payoffs y1 < y2. This is how they lay out their conclusions in the introduction (p. 1327):

Our empirical data indicate that a disutility for being overruled appears to be an important driver behind their reluctance to delegate….If…a principal experiences a nonpecuniary disutility from being overruled, her behavior after these two outcomes [see the paper for the details] may differ…Thus, a disutility from being overruled appears to be an important nonpecuniary factor behind the reluctance to delegate.

They employ a utilitarian model of ex post regret aversion to explain why some people don’t always pick a greater amount of money (y2) over lesser amount (y1). In econospeak, this sounds like a reasonable conclusion.

Let’s apply this summary to an orange and apple consumer who picks bundle B over bundle A.

Our empirical data indicate that a disutility for being without an apple appears to be an important driver behind her reluctance to only buy oranges…A principal experiences a noncitrus-y disutility from being without an apple…A disutility from being without an apple appears to be an important noncitrus-y factor behind the reluctance to only buy oranges.

Whoa Nelly! What just went wrong? We’re riding the same utility maximization workhorse, but the conclusion doesn’t make a lick of sense with the apples and oranges of intermediate microeconomics. Why can’t we make the same conclusion about choices with apples and oranges that we can with authority and money? Note the following differences in the two cases:

- Behavioral economists care about why somebody chooses bundle B and not bundle A. We assign a non-market meaning to point B in the authority experiment that we do not assign to observing bundle B of apples and oranges. How the person feels in the authority experiment is the reason why we are interested in it. In contrast we couldn’t care less how the consumer feels choosing a bundle of apples and oranges. We don’t care what is going through the mind of the apples and oranges consumer because fairness, altruism, and the like aren’t relevant for the understanding (that) choice in markets.

- Behavioral economists do not care why somebody chooses bundle A and not bundle B. The default assumption is that people prefer more money to less. The article is rather silent as to why some people are unwilling to give up $y2-$y1 for authority even though why someone does not accept a lower payoff for control would appear to be part and parcel to understanding authority. For our consumer of apples and oranges, we also do not care why somebody chooses bundle A, but we also make no assumption about the reason for that choice.

- We condition the observed bundle of apples and oranges, whatever it may be, on an exogenous and observable pair of prices and a budget. Changing the price(s) and budget is the second half of the lesson in intermediate microeconomics; it’s why the utility maximization model was first constructed. In the authority experiment there is nothing observable or external to the problem on which we can condition the choices of the participants.

Before the first participant made a decision in their experiment, Fehr et al. infused bundle B with the meaning of a preference for authority. Why else conduct the experiment? That isn’t the ex post facto tool of utility maximization. That’s ex ante facto, and the problem with ex ante facto is that for a fact to be facto the event must first occur. Otherwise it’s pure speculation. It is a fact that some people chose bundle B in the experiment, but Fehr et al. conflate that observed fact as a fact of why those people chose bundle B. Fehr et al.’s reason why (“experienc[ing] a nonpecuniary disutility”) is emphatically not a fact, just as experiencing a noncitrus-y disutility is not a fact. Fehr et al. inserted their own why into the experiment by imparting that meaning to bundle B before they conducted the experiment.

In intermediate microeconomics, to say that our apple and orange consumer experiences a noncitrus-y disutility from being without an apple isn’t merely speculation; it is nonsense. So why does it sound somewhat reasonable to say that a principal experiences a nonpecuniary disutility from being overruled? Because from ordinary human intercourse both Fehr et al. and the reader recognize, in the sense of becoming aware again, that people tend to like being in control. (It’s also one reason why we enjoy watching Game of Thrones.) But that recognition of the everyday human experience, by the authors and readers, is not a scientific fact of the experiment and is thus the reason why utilitarian behavioral economics does not provide a scientific explanation of human action.

Utilitarian behavioral economics falters because it undiscriminatingly accepts the fact that different environmental stimuli may appear to call for the same response (say, choosing the larger monetary payoff) and that the same stimuli sometimes appear to call for different responses. By employing a method that focuses on outcomes, utilitarian behavioral economics misses the scientific problem raised for explanation, viz., the perception of the situation is as much a response to the environmental stimulus as it is a reaction. Hence, it is an error for behavioral economists to use their own perceptions as elements of the scientific explanation of their subjects’ actions.

Parts of this essay are drawn from my article entitled, “Social preferences aren’t preferences.”

READER COMMENTS

Greg Ransom

Oct 3 2013 at 1:59am

Read Stanley Wong’s book on Paul Samuelson and Revealed Preference and then get back to us.

This reification of “‘utility” as a thing chosen and maximized actually is a fraud — it actually makes no sense and has nothing to do with reality and causation and causal explanation.

It’s a way of talking about a mathematical construct — a deeply misleading way,

UnlearningEcon

Oct 3 2013 at 3:06am

As Joan Robinson observed, this is completely circular. We assume people are maximising utility, and then whatever they do is evidence of this maximisation.

All these behavioural examples show is that utility doesn’t really make sense. As neuroscience shows, people have conflicting parts of the brain and their opinion of decisions changes over time and based on other people’s perceptions. So there’s a lot more going on than utility.

Tracy W

Oct 3 2013 at 4:26am

I’m perhaps being stupid, but what’s logically wrong with making the statement about disutility from being without an apple as a reason why someone doesn’t only buy oranges? The statements are bad writing as they state a simple idea in an involved way but I can’t see how “the conclusion doesn’t make a lick of sense”.

Tracy W

Oct 3 2013 at 4:40am

Is your objection that Fehr et al don’t independently establish the existence of the non-pecuinary disutilities?

If so I’m inclined to agree. I’m finding it more and more noticeable how seldom scientists who report on other people’s irrationalities speculate as to how their own irrationalities might be affecting their results. Nor do they seem to be in the habit of asking why their test subjects made their choices.

Adam

Oct 3 2013 at 1:05pm

Response to column seems a little confused, but it’s easy to get lost in the long read. The intro point about apples, oranges and utility is really beside the point.

The big point is the behaviorist rationalize their results ex post. The last paragraph says it well:

That is, behavioral economics is unscientific because it avoids prediction and testing. Instead, it offers ex post rationalization in pseudo-scientific language.

Eric

Oct 3 2013 at 1:58pm

In the article, you state that social motives are not observable without actions and thus we should not speak of them apart from actions.

At the moment, Bart Wilson is not observable to me. All I’ve ever seen of him is some writing and a picture on a web-site. However, I infer his existence as the most likely model. I could be wrong. Tyler Cowen could be playing an elaborate joke on everyone. But I consider my inference as to Bart’s existence pretty solid. Though he is revealed only through the Internet, I would not feel I was going beyond the proper in speaking of him apart from the Internet.

All observation requires inference and selection of a model. There is a great gap between photons lighting up a photo-detector or a retinal cell and seeing an event (for example, seeing a person electing not to take a ($10,$10) payout and pass control to another person). This gap is filled by inference. Computer vision and speech recognition research have made that extremely clear.

That a motive is not something which directly affects sight, sound, touch, taste, or smell does not make it unobservable, it just means that we need to rely on more remote (and thus more uncertain) chains of inference to know about it and to discern whether it is a useful inclusion in our model.

MingoV

Oct 3 2013 at 6:44pm

Economic/sociology lab studies often have serious flaws. People in the wild do not react the same as people in the lab. Here’s a more realistic scenario: You’re walking in a city and find a blank envelope containing eight $5 bills. Would you split the money with a nearby pedestrian? My prediction is that almost everyone would say no. The ‘found money’ scenario is essentially the same as the lab scenario, but the results would differ greatly.

Scenario 2: Same as above but the date is December 22. You find the envelope containing $40 half a block before you reach a Salvation Army Santa Clause soliciting donations. When you get to the Santa, would you put any of the found money into the collection pot? I predict a full variation of responses from donate all to keep all, but I’m only guessing.

True field studies have been done on these topics, and those studies generate better data.

y81

Oct 3 2013 at 9:58pm

Is the concept of utility still a big part of economics? As a former econ major, I was intrigued to note that my daughter’s freshman econ textbook (Mankiw) barely uses the word.

Bart

Oct 4 2013 at 8:22am

@Eric

Not all inferences are of the same kind. Inferences about natural phenomena, like photons, consists of relations of the external world. Inferences of another’s motives involve one’s own history of sociality and can’t be extirpated from an observed action, for “the only criteria of what constitutes a social motive is the sincerity with which the individual asserts he has one.”

Matt

Oct 12 2013 at 12:12pm

Could you please answer questions above by Tracy W? (These seem like very good, thoughtful questions.)

Bart

Oct 15 2013 at 9:09pm

Sure, Matt and Tracy W.

Is my objection that Fehr et al don’t independently establish the existence of the non-pecuinary disutilities?

Yes, and not only that they don’t, but that they can’t. There is no criteria, independent of the action that the participants take, to establish what a non-pecuinary disutility is.

Noelle

Oct 16 2013 at 9:13pm

There are many psychological factors that come into play when evaluating consumer behavior. In your apples and oranges example, behavioral economists could argue a range of said factors: taste preferences, mood, personality differences, etc. Mr. Wilson mentioned, “we don’t know and we don’t care.” He’s right. These individual differences are not large enough to have a huge impact on consumer demand. Economists are focused on the generalized view of consumer behavior. These include the expectations that consumers will behave rationally in their decisions to maximize utility, preferences for choosing certain products (like he said, nobody cares why these products are chosen so long as these products are being purchased), budget constraints, and the actual price of goods.

On the topic of authority and pecuniary factors, other, more complex factors must be considered when running an internal cost-benefit analysis. These factors have biological, psychological, and social implications. To operationalize morality, MIT neuroscientists, Liane Young and James Dungan, agreed that emotion and theory of mind are both involved with moral cognitive processes. As a result, scientists discovered that they needed to focus on the “engagement of the ‘emotional brain’ and the ‘social brain’” rather than specifically look for the “moral brain” (1).

Interestingly, as one would expect, neuroscientists were right about the emotional brain. Young and Dungan report that, “the ventromedial prefrontal cortex (VMPC), which projects to limbic, hypothalamic, and brainstem regions known for encoding emotional value of sensory stimuli, is directly linked to moral judgments” (3-4). Moral decisions are typically influenced by emotion. If all moral decisions were rational, then the market would never shift. Ergo, theory of mind, or “beliefs and intentions,” plays a huge role in the social brain. So, in simple apples or oranges decisions, you could say that the market has no room for behavior differences. However, when it comes to judging beliefs (authority and power) and intentions (monetary payoffs), I think behavioral economists have a rightful place in their science.

Young, Liane, and James Dungan. “Where In The Brain Is Morality? Everywhere And Maybe Nowhere.” Social Neuroscience 7.1 (2012): 1-10. Arts & Humanities Citation Index.

Comments are closed.