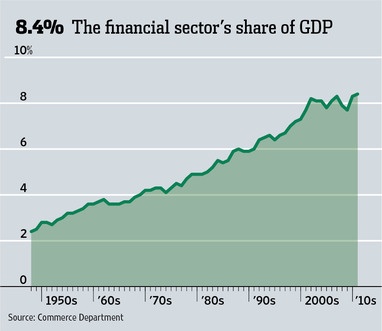

The U.S. financial sector is now 8.4% of GDP. It grew from about 2% of GDP in the late 1940s to about 8% in 2000; it’s been roughly flat since. From the Wall St. Journal:

My question: Suppose buy-and-hold investment strategies were near-universal. To be more specific, suppose 90% of all investment dollars were used to robotically purchase the market basket, then hold these assets until retirement. In this scenario, would the finance sector dramatically shrink?

Intuitively, it seems like it should. The thick market for buy-and-hold dollars would drive management fees below index funds’ already low rates. And if almost no one tries to time the market, it’s very hard for sophisticated insiders to get rich. There aren’t enough fools left for the “greater-fool” strategy to be amount to a large share of GDP. In such a world, it would be hard for the value-added of finance to exceed a few percent of GDP.

Of course, if you’re the only active trader left in a buy-and-hold world, finance could be very lucrative indeed. Just adjust your portfolio every morning when you read the newspaper and you’ll clean up. But in my scenario, there are still plenty of competing active traders. They only control 10% of the dollars. But that leaves an army of financial sophisticates competing to fleece a relatively small pool of suckers.

Still, finance is not my area. Am I missing something important? If so, what?

P.S. I am well-aware that buy-and-hold was very rare in the 40s, 50s, and 60s. My conjecture is that finance’s share of GDP skyrocketed despite the rise of buy-and-hold investing.

READER COMMENTS

James G

Nov 13 2013 at 11:10pm

I think the biggest thing you’re missing is that finance isn’t big because retail investors want to actively trade their portfolios. Think of the IPO business, corporate loan facilities, derivatives trading (where derivatives are used to hedge actual business risk), etc. Maybe in an i.i.d. world that would actually be feasible.

david

Nov 13 2013 at 11:14pm

I believe it was Fama himself who pointed out that to buy an actual “market basket” in the economic sense of the term, you cannot just buy a bunch of equities. The capital market includes a vast array of other kinds of capital: complicated partial rights to real estate, forex, assorted hedges against real risk (futures/etc.).

So you would need someone to do the legwork in constructing financial instruments that would represent all of these derived values: constructing derivatives and other market-making activity. It is this legwork which would entail economic activity.

honeyoak

Nov 14 2013 at 12:10am

You have to realize that the finance sector is much bigger than the equity markets. Insurance, Banking, Derivatives, Debt are not amenable to buy and hold strategies.

BC

Nov 14 2013 at 12:12am

James G is correct. I don’t know what fraction of the financial industry actually manages active investments. Investment banks allow corporations to access the financial markets (IPOs, bond issuances). Even if most investors were passive, there would still be a need for securitization, e.g., turning mortgages into mortgage-backed securities since mortgages are part of the “market portfolio”.

Also, you might be surprised how much of finance consists of back office and compliance people whose main job is to do the accounting and ensure compliance with all the regulations.

Think of retail banks. The portion dedicated to “active management”, i.e., evaluating credit-worthiness of borrowers and setting interest rates on savings accounts and loans, is actually small relative to the rest of the bank, which is required just to keep the bank operating.

8

Nov 14 2013 at 1:32am

The financial sector exploded in size in Wiemar Germany during the hyperinflation. If you look at the financial sector as a share of the S&P 500 Index, it grew rapidly from the 1980s into 2007. Post-crisis it collapsed, but thanks to QE it has grown back to the second largest sector. It tracks the growth of total credit outstanding.

Imagine if Vegas casinos gave out credit like water. Then, when gamblers went bust and couldn’t pay, the Federal Reserve would buy poker chips from Caesar’s and the casinos could hand these out to the gamblers again. You’d see the gaming sector of the economy grow steadily.

mobile

Nov 14 2013 at 3:20am

Buy-and-hold dominates already dominates the investment world (the passive/active AUM ratio at the large investment management companies I’ve worked at is about 70/30), but it’s getting a bigger share of a much bigger pie, so-to-speak. The rise of buy-and-hold occurs at the same time as the rise of pension plans, defined contribution plans (401k/Roth IRAs), increased global trade, and other innovations that have made the world’s exchanges accessible to middle class Americans. America also has a leadership role in global finance, so there is a lot of in-sourcing of services to the American financial sector as the same trends play out in other countries. None of this is particularly bad.

mobile

Nov 14 2013 at 3:30am

Active trading need not be a zero-sum game, either. Active traders can benefit at passive traders’ expense, and in fact this is easier to do in thin markets dominated by passive traders. Consider being able to manipulate the price of a stock on the day that an index is recomputed with a small capital investment — you are then exerting control over massive flows of investment over the next 3-12 months.

Don

Nov 14 2013 at 7:08am

Buy and hold is only an effective investment strategy if there are lots of active traders. The only way financial markets can be efficient is if there are lots of people who don’t think they’re efficient and go around looking for bargains. That’s what makes the bargains vanishingly difficult to find, which is what efficiency is.

OneEyedMan

Nov 14 2013 at 7:58am

I’m with honeyoak. Equity secondary trading is actually a pretty small part of the Finance, Insurance, and Real Estate (FIRE) industry. Secondary offerings are pretty small fraction of the total and shares are near infinitely lived assets. Debt has to be rolled over and insurance contracts expire. That makes those parts much larger. Even the quantities are very different, public equity in the USA is 18T while non-financial debt is more than 40T.

I’m not so sure that Don is right that markets have to be efficient for a buy and hold strategy to work. In general the returns on riskier and more illiquid assets are actually higher than liquid assets, so less efficient markets might actually be more profitable for long holding period investors at the cost of shorter holding period investors.

What would worry me more about a huge shift to buy and hold investing is what it would do to executive behavior and new equity offerings markets. Who would fire the bad CEOs without takeover threats and the like? Diffuse buy and hold investors seems unlikely. And buy and hold seems to preclude opportunistic buying as well as selling, thus making it much harder to list new shares. But if we think about shifting to from th 70/30 passive/active split to 95/5 that seems workable in both dimensions, especially if that 5 group has additional capital to deploy when needed.

Bostonian

Nov 14 2013 at 8:26am

I’ve read that the average holding period of stocks has declined over the years, and a post “What the Decline in Stock Holding Periods Means for Investors” at Seeking Alpha has some data confirming this. Even if you have no stock selection skill, it makes sense to harvest tax losses by selling stocks on which you have a loss. These losses can offset capital gains and up to $3000 of ordinary income. The same is true at the asset class level. If you have a large loss on an S&P 500 index fund, sell it and buy something similar, such as a fund tracking the Russell 1000.

Methinks

Nov 14 2013 at 9:26am

“Fleece a relatively small pool of suckers”? You are right. Finance, and especially trading, is definitely not your area. Yet, as an economist, you should be able to see your obvious error.

Finance, and especially trading, is very much “my area”.

If there are very few sellers relative to buyers the sellers can demand buyers cross an enormous bid/ask spread to transact. That increases volatility, diminishes returns and increases the cost of capital.

The giant size of that spread will attract people who realize that they can make a lot of money by offering securities as well, so they begin to compete for that enormous edge. The only way to compete is to show a better price (either a higher bid or a lower offer). If the other party finds my price acceptable, he will hit my bid or lift my offer. I can’t force anyone do transact with me. Does that sound like I (or any other liquidity provider)am “fleecing” anyone? Or does it sound like the liquidity providers you accuse of “fleecing” are taking risks with their own capital to provide a commodity called “liquidity” that the market willingly pays for?

Liquidity reduces the bid/ask spread, lowers volatility, aids in price discovery, keeps prices close to fair value and reduces the weighted average cost of capital. In other words, it reduces the risk of owning securities. Does that sound like “fleecing”?

My job is to provide that liquidity because there’s profit in doing so. The market wants it. Otherwise it wouldn’t pay for it. Where there’s little of it, people pay for it dearly. The more “active traders” their are, the more liquidity providers, the more competition I have, the lower my profit margin and the less risky investing is for everyone else.

So, yes, I’m all on board with your more buy and hold and fewer active traders scenario because with less competition, I can widen my spreads and properly fleece the “suckers”. I can’t do that with competitors constantly bettering my price.

The real fleecing isn’t happening from the active traders committing their own capital to make a profit providing liquidity. It is happening in the below market financing that my firm and other financial firms are receiving courtesy of the Fed. It’s coming from the rents (largely, I argue, competed away at this point) that our lobbies extract like the mixed straddle, which essentially means all options market makers’ profits are taxed at the long term capital gains rate. That mixed straddle treatment is only available to broker dealers. You don’t qualify for that tax treatment in your retail Interactive Brokers account. It comes from the regulatory capture. We professionals will always have a regulatory edge so long as there are regulations. We can do things you can’t. That’s where the fleecing is coming from, not from trading. The trading is the only free market part of finance anymore.

Methinks

Nov 14 2013 at 9:48am

I believe it was Fama himself who pointed out that to buy an actual “market basket” in the economic sense of the term, you cannot just buy a bunch of equities. The capital market includes a vast array of other kinds of capital: complicated partial rights to real estate, forex, assorted hedges against real risk (futures/etc.)

That right there is why the CAPM can never actually be tested. It includes all assets and good luck constructing a portfolio with an adequate sample of every single asset.

Methinks

Nov 14 2013 at 10:10am

Consider being able to manipulate the price of a stock on the day that an index is recomputed with a small capital investment — you are then exerting control over massive flows of investment over the next 3-12 months.

Well, it’s pretty hard to control massive flows of investment with a small capital investment of your own. In fact, it’s impossible. However, if you’re trying to say what I think you’re trying to say, then I think you’re wrong.

Everybody knows what securities are going into an index because they are announced ahead of time and every arbitrageur is putting in market-on-close offers because the mutual funds that are replicating that index will have to buy the securities at the close. So, what ends up happening is that there are so many arbitrageurs putting in market-on-close offers that there ends up being plenty of supply to meet the additional demand and the price doesn’t move or it doesn’t move much. The more traders willing to offer, the smaller the profit in the trade and the cheaper the transaction cost for the index fund. It’s always good to have more “thieves at the table”.

Patrick R. Sullivan

Nov 14 2013 at 12:09pm

Methinks, the lady, doth protest quite effectively.

I notice from the graph that the growth in share of GDP of finance is steady from 1950 til 2000, then it flattens. Should make the ‘It was the repeal of Glass-Steagall that caused the financial crisis.’ crowd unhappy.

mobile

Nov 14 2013 at 12:32pm

The hypothesis here is that the trading of the vast majority of stock is tied up by passive investing rules, and that there are not a lot of arbitrageurs. Manipulating an index at the expense of passive investors is easier and more profitable under these conditions, for certain definitions of “easier” and “profitable”.

Not all index changes are announced ahead of time (Russell publishes “provisional indexes” two weeks ahead of its annual reconstitution date, but the final index constituents are completely determined by prices on the reconstitution date), but even so many index changes are determined by fixed or at least very predictable rules, which just moves your attack date forward by 5-14 days. Most of the price movement associated with an index change occurs when the changes are announced, anyway, as opposed to the effective date of the index change.

josh franta

Nov 14 2013 at 1:37pm

you’re missing a couple of things. it’s interesting to me that an economist wouldn’t know how banks make money or have perspective on relative size of banking versus hedge funds.

first, financial firms that contribute most to GDP are the big guys… JPM, citi, morgan stanley. these are public companies so you can see where there revenues come primarily from. trading is not a majority of their revenues. they [generally] generate most of their revenues on capital markets (corporate financing, ipos, etc), fees (investment banking, merger and strategy advisory, etc) and retail (credit cards, money markets, cds, brokerage, etc).

second, with respect trading activities banks are highly regulated and this is becoming more so because of volkner and others. so even in fixed income where they trade assets for their own or client accounts, the purpose of this trading is to hedge bank and client liabilities, rather than to nakedly speculate with customer deposits. hedge fund assets and revenues are extremely small as a percentage of GDP, maybe 100 basis points for the industry (http://www.quora.com/What-percent-of-GDP-is-the-hedge-fund-industy).

just to put this in perspective, jp morgan alone has about the same assets as does the entire hedge fund industry (~2T).

Keith K.

Nov 14 2013 at 2:40pm

Go back to a gold standard with no central banking and it will plummet back to its 1940’s size (or even smaller).

I mean the whole central planning effect from central banking definitely seems to be a huge contributor here.

Methinks

Nov 14 2013 at 3:54pm

The hypothesis here is that the trading of the vast majority of stock is tied up by passive investing rules, and that there are not a lot of arbitrageurs.

Conservatively, there are over ten thousand arbitrage firms in the this country alone. Some of those firms are Goldman Sachs, JPM and SIG. The vast majority of the firms are smaller shops like mine. There doesn’t seem to be a huge shortage of arbs around. Even if there were a shortage, that doesn’t mean there’s price manipulation.

Manipulating an index at the expense of passive investors is easier and more profitable under these conditions, for certain definitions of “easier” and “profitable”

Words have meaning. “Manipulation” has a very specific meaning. Let’s just imagine for a moment that there aren’t a lot of arbitrageurs in our fantasy scenario. An index announces a rebalancing. The arbs run out and buy the stock. They’re doing much the same thing that retail guys do when Jim Cramer screeches “Booyah! Go by stock xyz”. The increased demand increases the price. Where is the manipulation? You’re not suggesting merely trading on news is manipulation because that would be a silly thing to say, yes?

(Russell publishes “provisional indexes” two weeks ahead of its annual reconstitution date, but the final index constituents are completely determined by prices on the reconstitution date)

How does one take advantage of this information? Are you suggesting that thousands of competitors are colluding to buy up the list to ensure those stocks’ inclusion?

Most of the price movement associated with an index change occurs when the changes are announced, anyway, as opposed to the effective date of the index change.

When most of the price move happens doesn’t matter. There’s also a tidal wave of market-on-close orders on the blessed day. It’s quite fun to watch them stack up on the book, actually.

You made a specific claim of manipulation. So far all you’ve said is that prices of securities move in response to news. I’m not seeing the manipulation.

Hansjörg Walther

Nov 14 2013 at 5:07pm

Other commenters have already pointed out that you miss most of the market. How much of it?

Here’s a back-of-an-envelope estimate:

In the US, assets under management by mutual fund companies are somewhat less than the size of annual GDP ($13T in 2011 and $16.7T, estimate for 2013).

If you think that the financial sector mostly lives off mutual funds, then you would also have to think that they take out like 10% of assets annually one way or the other.

mobile

Nov 14 2013 at 7:47pm

I think we’re talking past each other a little bit.

Yes, of course there are a lot of arbitrage firms. Bryan’s counterfactual is to suppose that the idea that stock picking is unprofitable becomes more ingrained, the supply of profits from “greater fools” dries up, and most of these firms exit or switch to passive investing. My claim is that the rule-based, predictable trading patterns of passive investors are another source of value for active traders. For example, stocks entering the S&P 500 or the Russell 2000 almost always experience a substantial increase in their share price.

When there are lots of firms competing for this value, less value accrues to each firm and in fact much of the value is retained by the passive investor. I don’t think you disagree with that statement.

In Bryan’s future investment landscape, a smaller fraction of the capital is used to determine the consensus value of each asset. Compared to today’s markets, spreads are higher, volatility is higher, and a single agent can have a larger impact on the price of an asset, especially a short-lived impact. In this environment, it is “easier” to, say, target the 2005th candidate on a Russell 2000 provisional index and drive up its price on Russell rebalance day to make it a surprising addition to the index. The index managers are now obliged to purchase the stock and the active trader extracts the value. The existence of this arbitrage strategy (and others that may be more plausible to you) will keep the equilibrium ratio of active-to-passive traders closer to where it is now and farther from where Bryan conjectured it was going.

You seem to think that I have made a claim that such index manipulation has occurred or is occurring. I have not made a claim like that, and like you (I think), I am skeptical about claims like that in today’s markets.

methinks

Nov 14 2013 at 10:35pm

Yes, mobile, I did misunderstand you. Of course, I agree that more firms are better than less and for all the reasons you mention.

However, I pick no small nit when I take issue with the use of the word “manipulation”. Trading on information available to the entire market that leads you to believe that demand for a stock will increase is not devious, fraudulant or unethical behaviour. In illiquid markets, a single trader has more impact on the price, but what you describe is not manipulation.

Also, if a trader knows the stock is going into the index, he doesn’t want to drive up the stock with his buying. He wants to accumulate his entire positon and for the stock to go up when he’s done. Otherwise, he’s cutting into his own theoretical edge. No trader wants to move the price of the security against himself.

There are some grey areas like scenarios where a stock might be included and the trader in an illiquid market can try to drive the stock to a certain price, but always at the enormous risk that he’ll be unsuccessful. Even today in index options, since they are cash settled, if there is a single large seller and the options look like they will expire at the money, even a large number of market participants will gun the seller by trying to drive the options into the money at expiration.

kebko

Nov 15 2013 at 12:30am

Bryan, I recommend this recent article:

Jonathan Monroe

Nov 15 2013 at 5:40am

As numerous people have pointed out, the bond market is bigger than the stock market.

Corporate bonds are already mostly buy-and-hold (the bonds are generally sub-10 year maturities, and held to redemption), and mortgage-backed bonds are actually buy-and-hold (because the institutions to avoid lemons problems in the secondary market do not exist), although banks in 2007 lied and said they were liquid in order to game capital requirements.

Methinks

Nov 15 2013 at 8:50am

Jonathan Monroe,

How can that be true? The mortgage market is almost as large as the Treasury market which is the largest and most liquid fixed income market in the world. If the banks lied about liquidity, it was an easily verifiable lie. If the mortgage market was so illiquid and lacked a secondary market, how did John Paulson accumulate such an enormous short position in subprime mortgages? The mortgage market was plenty liquid.

The mortgage market locked up and became very illiquid when reality finally penetrated to market participants. But, that’s a normal reaction to such realizations. When everyone realizes what’s trading is trash and they have to revalue the whole lot liquidity evaporates.

Methinks

Nov 15 2013 at 8:54am

Jonathan Monroe,

How can that be true? The mortgage market is almost as large as the Treasury market which is the largest and most liquid fixed income market in the world. If the banks lied about liquidity, it was an easily verifiable lie. If the mortgage market was so illiquid and lacked a secondary market, how did John Paulson accumulate such an enormous short position in subprime mortgages? The mortgage market was plenty liquid.

The mortgage market locked up and became very illiquid when reality finally penetrated to market participants. But, that’s a normal reaction to such realizations. When everyone realizes what’s trading is trash and they have to revalue the whole lot liquidity evaporates.

dwurren

Nov 16 2013 at 9:13am

Calculating GDP contribution of finance is more of an art. First, GDP contribution is measured by value added contribution. The value added contribution of finance is calculated less interest. What value you assign to interest will affect to a great extent the contribution from finance. In a low interest environment, if finance revenues stay the same, the contribution will go up (I think – I’m not an economist). Second, I don’t believe that the returns on mutual funds or hedge funds are factored into GDP. Those are capital gains, not income, and aren’t included in GDP. The fees from managing mutual funds are included, but those fees are relatively small – the mutual fund industry just isn’t that big. Second, the amount of active capital in the capital markets is relatively low. I did a back of the envelope calculation that the total amount of speculative capital – ie capital chasing alpha, over and above market return – is about $750B. That money is chasing about $150B of alpha. The alpha comes from money losing investors who underperform and from money devoted to purely speculative activities such as futures, currencies, and shorting.

Comments are closed.