I’m associated with the “pro-inflation” crowd because of my advocacy of monetary stimulus over the past 5 years. This is actually sort of ironic because I’m an inflation hawk who was trained at the University of Chicago in the late 1970s and haven’t significantly changed my views on monetary policy over the past 35 years. Thus the fact that I’m now viewed as a pro-inflation dove tells you more about the state of macroeconomics circa 2014 than it does about me. I’d be happy with even 4% nominal GDP growth, level targeting, which would result in roughly 2% inflation, on average.

People are becoming increasingly aware that NGDP growth in America since 2008 has been too low (lower than 4% on average), and that the problem in Europe has been even worse. That means monetary policy should have been more expansionary, even if it seemed highly expansionary to people who aren’t familiar with the fact that low interest rates and a big expansion of the monetary base don’t mean easy money.

I suppose there is a danger that things will eventually swing too far in the other direction, and people will begin advocating more inflation than is desirable. So let me point out one fallacy that seems to be increasingly common—the idea that the “Great Inflation” was both necessary and helpful. It was pure waste. Here’s a alternative view from Ryan Avent, discussing earlier posts by Steve Waldman:

This, as it happens, is basically the story that Steve Waldman tells about America in the 1970s, noting:

I don’t dispute that monetary contraction could have prevented the inflation of the 1970s. But under the demographic circumstances, the cost of monetary contraction in terms of unemployment and social stability would have been unacceptably high.

Mr Waldman brings with him another important piece of the puzzle: wage rigidities. Because wages were rigid, the adjustment needed to put everyone in the demographic bulge to work would have been long and painful.

I don’t think that’s correct. If the rate of inflation had been 5% points lower in the 1970s, I believe the rate of nominal wage growth would have also been about 5% points slower, and the unemployment rate would have been about the same. The actual inflation rate (about 8%) involved at least 5% points of pure waste—a wage-price spiral that discouraged saving and investment, and did not promote employment.

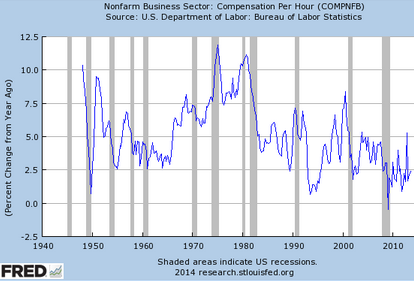

Take a look a the graph showing wage increases in the US. Things were unstable in the early 1950s, perhaps due to the Korean War, but then settled down to 3% to 4% wage gains in the late 1950s and first half of the 1960s. Then with the advent of the Great Inflation, wage growth increased sharply and stayed high until 1981. So wages were pretty flexible over a period of 16 years, even if one year wage changes are somewhat sticky.

PS. Much of Ryan’s post is excellent, particular the comments on the British labor market.

READER COMMENTS

Kenneth Duda

Jan 23 2014 at 9:59am

Scott, I think you are exactly right here. The point I’d add (I’m a bit surprised you didn’t say) is that if 1970’s-level inflation had been needed for real wage adjustment, then we would see low nominal wage growth in a high-inflation environment, i.e., rapid real wage adjustment. That sort of data would support high inflation in my view. What you actually see in the 1970s is high nominal wage growth in a high-inflation environment, which means, as you said, there was more inflation than needed — pure waste.

-Ken

Kenneth Duda

Menlo Park, CA

sourcreamus

Jan 23 2014 at 12:16pm

What I don’t understand about NGDP level targeting is how we know what level is correct. If pot is legalized and everyone stays home to get high instead of going to work then RGDP is going to tank. Does this automatically mean we need more inflation? Conversely, if cold fusion is invented and the economy takes off, does that mean we need deflation?

What am I missing?

If China had set their goal at 4% growth they would have really tight monetary policy. I know 4% is historically right in the pocket, but how do we know if will always be right?

Nathan Smith

Jan 23 2014 at 1:38pm

re: “Conversely, if cold fusion is invented and the economy takes off, does that mean we need deflation?”

Seems to me the answer is: Yes.

They say deflation is bad because of downward nominal wage stickiness. Employers are afraid to cut nominal wages. Deflation means that without nominal wage cuts, real wages rise. So employers will fire workers whose productivity is merely steady rather than rising.

But in a boom, that’s a feature, not a bug. Interest rates are positive, so you don’t need to worry about the zero lower bound. You want workers to be reallocated from sectors where productivity is stagnant to rapidly growing, labor-hungry industries. Mere inertia will slow this reallocation. Downward nominal wage stickiness spreads the new wealth across the economy in the form of lower prices/higher real wages– saving workers the bother of negotiating for their share– and accelerates the reallocation of labor. Debt-deflation could still be a problem, but that’s why the government shouldn’t use taxes and subsidies to encourage people to get themselves indebted.

Am I right?

But, two questions.

1. Given that the government doesn’t seem likely to create an NGDP futures market anytime soon, is NGDP targeting currently feasible?

2. Is targeting asset prices a feasible substitute? You could think of QE over the past couple of years as getting stock market valuations back up to historical trend, no? Stock market valuations seem like a crude proxy for NGDP futures, since the value of stocks depends on the expected trajectory of future (nominal) profits. Stock markets are very easy to observe. What if the Fed made “sustainable asset price growth” its target?

Michael Byrnes

Jan 23 2014 at 3:30pm

The Fed could start targeting the level of NGDP tomorrow if it wanted to (it obviously does not want to, at least not yet).

Their next statement could include a graph with the targeted trend line for NGDP, FOMC estimates of NGDP, and this statement, “The committee judges that an NGDP growth path of(see figure)is consistent with its statutory dual mandate of stable prices and low unemployment. Monetary policy will remain accommodative as long as expected NGDP growth is below this trend. In the future, the committee will pursue a monetary policy that is consistent with the committee’s stated objective.”

A futures market would be useful to 1) bind the Fed so that it is not free to arbitrarily change its policy goal and 2) provide better information so as to allow more precise targeting of NGDP.

But the main benefit of NGDP targeting is preventing big swings in NGDP such as were seen in the 1930s, the 1970s, and in 2008-09.

As to what the target should be… Scott usually suggests 5% because that is roughly the rate of NGDP growth that we saw during the 20 years prior to the 2008 crash. People are used to (over the long term) 3% real growth and 2% inflation, so a 5% target would be consistent with the expectations of the public.

I think some people have suggested 6%, but it cannot be too much higher than that because that would just lead to more inflation. It could be lower than 5% – that would require that people adjust to lower long-run inflation expectations, but people would adjust eventually. I think you would want it high enough that NDGP growth stays positive even in the event of a nominal shock. (Realistically, NGDP targeting will dampen but not eliminate nominal shocks).

Exactly what the target should be is less important that sticking with the target once it is adopted. People will be able to adjust to any official policy target between more easily than they could adjust to an ever changing policy target. For example, a bank would offer different interest rates on 30 year mortgages if the target was 3% versus 6%. Changing from 3% to 6% (or from 6% to 3%) would either increase (or reduce) the real cost of the loan to the borrower. Better to choose a target and stick with it.

Scott Sumner

Jan 23 2014 at 3:57pm

Kenneth, You are right. That’s what I had in mind, but I forgot to spell it out clearly. Good point.

Sourcreamus, You can make a pretty good argument that NGDP/labor force is a better target than simple NGDP. I’ve tended to focus on NGDP for simplicity, and because year to year changes in labor force growth tend to be pretty small, at least when NGDP growth is stable. But one could imagine labor force shocks that create exactly the sort of problems you mention, in which case NGDP/LF would be a superior target.

Nathan, Yes, if there is very strong productivity growth then deflation may be justified. I’d recommend Less Than Zero by George Selgin.

If there is no futures market, the Fed should target its own internal forecast of NGDP, and do level targeting. Asset prices may be useful in constructing their internal forecast.

Michael, Good comment—I agree.

John Becker

Jan 24 2014 at 1:49am

Any theories on why compensation changes year over year have narrowed into such a tighter band?

Scott Sumner

Jan 24 2014 at 10:05am

John, Ever since 2009, NGDP growth has been running at a fairly stable 4%

sourcreamus

Jan 24 2014 at 11:51am

Thank you for the answer, does that work for other types of shocks too? Does the target have to be historical rate of growth plus 2%?

You know alot about China, but would it have been a good idea in 1979 for them to fix a target at the miniscule amount of growth they had in the past plus 2%? How would that have worked once their economy took off and started growing by 10% a year?, they would have needed negative interest rates at 7% a year for years.

Likewise, what happens if Robin Hansen is correct and we are on the verge of a high growth era and we suddenly get sustained periods of high growth and have to have a deflationary policy for long periods.

It seems like the target should be different depending on how well the economy is doing as a whole. If that is true then discretion about inflation rates may be important and rules such as level targeting not a good idea.

Michael Byrnes

Jan 24 2014 at 1:13pm

sourcreamus wrote:

“Likewise, what happens if Robin Hansen is correct and we are on the verge of a high growth era and we suddenly get sustained periods of high growth and have to have a deflationary policy for long periods.”

If prices are falling because of something that is happening on the supply-side – real goods and services are produced and delivered more cheaply – that’s not a problem, it’s a good thing! It means greater real income even if nominal income is unchanged.

The problem comes when prices fall because of a nominal shock. In this case, economic activity falls. Instead of producing more goods and services at lower cost, less is produced, and firms, on net, cut back on production and staff. This is what happened in the 1930s and again five years ago.

Level targeting, of the price level or NGDP, would prevent (or minimize) nominal shocks.

But an NGDP level target seems preferable, because it would allow inflation to fall in response to rising productivity. With a target of 5%, instead of 3% real growth and 2% inflation you would maybe get 3.5% or 4% real growth with lower inflation.

A price level target might be more procyclical than NGDP: for example under a 2% price level target, rising productivity would call for more accommodative monetary policy(to keep inflation from falling below target) than an NGDP target (which could allow inflation to fall as long as nominal income remained on target). Conversely, supply shocks may have greater negative impact under a price level target (since they may put some upward pressure on prices that limits the monetary policy response) than under a NGDP target.

Comments are closed.