Categories:

Money and Inflation

I’d first like to thank David for his very kind introduction. It’s an honor to be invited to do a stint as a guest blogger at one of my favorite blogs. I do plan to keep my other blog (TheMoneyIllusion.com) going, but at a reduced rate. I won’t be able to answer all the comments at both blogs, but will answer some.

I always get a bit annoyed when I hear people talk about investors putting money “into” markets. I suppose that at an individual level this might make some sense. You could take some of your money and purchase stocks. But is the money actually going “into” the stock market? If so, where does the stock market keep all the money that people invest? In a box? Or does money simply go through markets, as the person selling me the stock is presumably taking an equal amount of money out of the market?

On October 19, 1987, a record number of shares of stock were purchased on Wall Street. Does this mean that investors put a lot of money “into” the market that day? If so, why did stock prices fall by 22%?

Some might argue that the phrase “putting money into a market” is a harmless metaphor for describing rising asset prices. But why not just say “rising asset prices”? And I’m not at all sure that it is harmless. I also see people discuss monetary policy from the perspective of where the money goes, not just the supply and demand for money itself. And yet if existing money doesn’t actually go into markets, then newly created money doesn’t either.

Of course central banks generally inject new money by purchasing assets. So the effect of monetary policy might depend in some important way on the choice of assets being purchased. After all, doesn’t the law of supply and demand predict that an increased demand for an asset will raise its price?

At a recent conference Larry White mentioned that Milton Friedman had argued that the gold standard was wasteful, as it led to a higher real price of gold and thus socially unproductive gold mining activity. Larry pointed out that real gold prices actually rose after the government stopped buying gold at $35 an ounce. Friedman had forgotten that switching to a fiat money system might lead to higher inflation, which would encourage more private demand for gold (as an inflation hedge.)

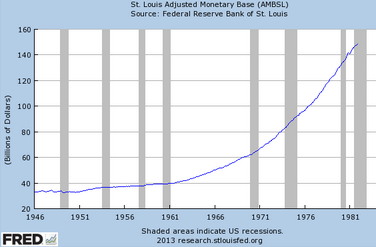

The same process may occur when the Fed purchases Treasury securities. During the 1950s the Fed purchased relatively few Treasuries. Then during the 60s and 70s there was a dramatic increase in the rate at which the Fed bought Treasury securities. So what happened when the Fed put all this money “into” the Treasury market? Surprisingly, T-bond prices plummeted between the 1960s and early 80s. This occurred because monetary policy doesn’t just affect the Treasury market, it also affects the “money market”. And by ‘money’ I mean the monetary base, the type of money directly produced by the Fed. The base began increasing rapidly in the 1960s and 70s, boosting inflation and nominal GDP (NGDP) growth, which pushed nominal interest rates sharply higher. So talk of the Fed putting money “into” markets is not a harmless metaphor for rising asset prices, it can lead to very serious errors. People think that monetary injections boost NGDP because they raise bond prices, whereas they actually boost NGDP even more on those occasions where the policy reduces bond prices.

READER COMMENTS

Ebsim

Jan 1 2014 at 10:54am

Could the rise in housing prices that soon plummeted be seen as natural cyclical matter then.

Personally I believe that it was caused by poor regulatory policy that created the incentives for just housing to rise. Whether it was the large amount of small lending institutions or FDIC insurance. I would hardly say it was deregulation but it definitely was the poor structure of regulatory institutions that prompted it.

Just one question Scott. Could the Federal Reserve then boost the value of housing if it buys mortgage back securities as part of QE?

John Thacker

Jan 1 2014 at 10:54am

There is a sense in which money goes into or out of a market, when there are stock offerings or buybacks, or IPOs or companies taken private. But yes, that’s not what people generally mean when they say it. (Even though it is an important point in realizing why the aggregate investor does not actually achieve the market return.) Usually they’re talking about people shifting from savings accounts or bonds to equities.

Eric Falkenstein

Jan 1 2014 at 11:03am

I’m really scared about the unprecedented nature of current macro policy. Learning by doing at this scale will be costly. That is, interest on (excess) reserves is basically neutralizing the Fed purchases, monetizing the Federal debt yet keeping High Powered Money constant. I have a feeling when that becomes untenable, the money-multiplier will rise again.

Scott Sumner

Jan 1 2014 at 11:33am

John, I see your point. I’d still prefer to say that money goes through a market during a buyback (corporation to public), and that wealth goes out of stocks and into other assets in that case. And as you say, that’s not usually what people mean by money going into markets. Stocks often rise on buybacks, even as “money flows out.”

Eric, I actually worry that money is still a bit too tight (although much less too tight than in 2009.) But on your specifics I agree. The policy of interest on reserves and a bloated monetary base was a bad idea—NGDP level targeting would have been better. That would not have required a bloated base.

James

Jan 1 2014 at 1:17pm

“There is no advantage from getting the money first.”

If the money exceeds the market value of whatever the Fed is buying, there most certainly is an advantage. E.g. if a bond is trading at X and the Fed buys that bond for X+Y, then the initial receiver’s purchasing power is increased by Y.

If Sumner’s claim were correct, it would be a mystery why anyone is willing to enter into transactions with the Fed’s open market desk. Why would anyone exchange a bond for cash if the transaction were no more advantageous than exchanging a dollar for four quarters?

Patrick R. Sullivan

Jan 1 2014 at 1:49pm

‘…if a bond is trading at X and the Fed buys that bond for X+Y….’

Has that ever happened? And the reason people trade bonds for cash is that cash is more liquid; you can use cash to buy anything from a loaf of bread to a Porsche.

Michael Byrnes

Jan 1 2014 at 2:10pm

James wrote:

“If the money exceeds the market value of whatever the Fed is buying, there most certainly is an advantage. E.g. if a bond is trading at X and the Fed buys that bond for X+Y, then the initial receiver’s purchasing power is increased by Y.”

As is the purchasing power of anyone else who owns a treasury bond, as the bond now trades at X+Y.

But, Sumner’s point is that this effect is small compared to the effects of raising the monetary base, which will cause bond yields to rise (and prices to fall).

Mike Freimuth

Jan 1 2014 at 3:03pm

James, you wrote:

“If Sumner’s claim were correct, it would be a mystery why anyone is willing to enter into transactions with the Fed’s open market desk. Why would anyone exchange a bond for cash if the transaction were no more advantageous than exchanging a dollar for four quarters?”

But this logic seems to imply that it is a mystery why anybody ever trades any financial asset at the market price. If people are only willing to sell at prices higher than the market price then there can’t possibly by such a thing as a market price or even a market.

The market price of a security isn’t fixed like the price of a dollar in quarters. It is determined by what people (on the margin) are willing to buy and sell it for. When the Fed buys them, this price may change but it does not always increase and when it does increase it does not make the people who sell to the Fed any better off than the other holders of the security who do not.

Jordo

Jan 1 2014 at 4:34pm

This blog post is all over the map. Literally, as it culminates with the idea housing markets across the globe might rise and fall in unison. With regards to predictions made by the law of supply and demand, the operational phrase is “all other things being equal”. There’s increasing demand for plenty of things that do not have ever increasing price growth. Like computers or “organic” food. The idea gold is purchased as a hedge against inflation might make a good sales pitch for a broker, but its poor economics and has zero track record of success–what is the exit strategy from ‘the hedge’? Compare the performance of gold, diamonds, and copper to the aluminum that encases ipads worldwide. Would it follow that encasing ipads in gold and diamonds would have the same effect on the price of the raw material as it does for aluminum?

Dustin

Jan 1 2014 at 5:08pm

Eric

Why? Fed pays IOR whether they are the required or excess variety – both at .25%. In other words, if banks lent against the mountain of ERs, they would simply become RRs, and the banks would still collect the same IOR as total reserves would remain unchanged. Even if the Fed only paid IOER, does .25% sound more appealing than market credit rates (even when accounting for the business costs of lending)?

I’d argue that the bloat – neutralization as you called it – is due to other factors such as 1) uncertainty regarding the Fed’s tolerance of inflation (which would occur if credit activity against ERs increased), 2) uncertainty regarding the duration of the injection of the reserves (highly correlated to tolerance for inflation), and 3) lack of credit demand (result of current deleveraging and beyond the Fed’s control).

Jon

Jan 1 2014 at 5:22pm

There is a bit more to the sense in which the term is used: whether quantity is perceived to be buy side or sell side determined.

In that way a burst forward or back of the price level can be said as money flowing in to or ought of markets in the sense of Market cap going up or down due to price changes.

MingoV

Jan 1 2014 at 6:57pm

Much Ado about Nothing

“I’m putting my money into the market” is a casual term for “I’m investing in stocks and stock funds.” It is not a statement about how the electronic codes that represent money zip around the world or where the money codes are at the end of their electronic journey.

My profession is lab medicine, and I could come up with a few dozen examples in which physicians misuse phrases related to lab tests. I’d be considered a jerk if I complained about this and requested physicians to use exactly correct phrasing.

Eric Falkenstein

Jan 1 2014 at 7:57pm

Dustin: I agree that excess reserves are treated the same as regular reserves, but I think the interest on reserves is exactly why there is an unprecedented amount of excess reserves. So, paying T-bill rates on reserves makes choose reserves over T-bills, which then takes than HPM out of the loop.

Philo

Jan 1 2014 at 8:07pm

“As a first approximation, at the macro level it doesn’t much matter what the Fed purchases. Nor does it matter who gets the money ‘first’. There is no advantage from getting the money first.”

I take this to be a swipe at the Austrian theory. As I understand that theory, it applies to secret injections of money by the monetary authority–to situations in which the authority is expanding the money supply in a fashion that no one anticipated, and where virtually no one is aware of what the authority is doing. Of course, as soon as the new policy became widely known there would be a sharp general rise in the price level, but Austrian analysis applies rather to the time before the news leaks out. During that time there will be a *gradual* rise in prices, as the recipients of new money spend it (and the secondary recipients in turn spend it, etc.). Those items that the first recipients most want to buy will be the first to have their prices inch up. While this process is going on, Austrians seem to feel that money *ought to be worth less* than it actually is worth, since the monetary authority is tricking people into overvaluing money. Those who *spend* money during this time are getting *more than their money’s worth* in return; this will be so until such time as the authority’s policy is widely understood, or at least until the hot-potato transactions occasioned by the injection have caused the value of money to decline to its proper level. So people who get new money *and spend it* will be getting an unfair advantage; but, of course, the same is true of people who have old money *and spend it*. (And people who *hold* money, new or old, will be unfairly harmed by the inflation.)

Perhaps the new/old difference is supposed to be that, since *the authority ought not to have expanded the money supply in this fashion*, people with new money ought not to have had it, and so ought not to have been able to buy things at the existing prices: at best (?), they should have been able to buy at the inflated prices that will prevail in the future, those that are *fair*, given the increased money supply (actual and prospective?). On the other hand, it is right that people with old money should have had that money, which they ought to be able to spend at the existing prices. But the distinction so drawn is morally dubious.

This (what I take to be) Austrian analysis has little application nowadays, when there is widespread sophistication about monetary policy and the monetary authorities are under close scrutiny by the media.

James

Jan 1 2014 at 8:39pm

Freimuth:

Ordinary participants trade in the asset markets because both sides expect to benefit in some way. No mystery. It IS mysterious to believe that anyone would do business with the Fed if the open market desk’s asset purchases benefited or harmed all bond holders equally.

To be clear, my views on price discovery in financial markets are entirely mainstream and in any case, a discussion of my views is a change of subject from Sumner’s erroneous claim that “There is no advantage from getting the money first.” Even if my views on price discovery are confused, that doesn’t make Sumner’s error go away.

TallDave

Jan 1 2014 at 9:41pm

Heh, I suppose that’s only interesting to monetarists but kind of neat to think about where the money actually goes.

Interesting too to think of what happens when the $1000 of Apple stock that Grandma glommed onto back when it was illegal for most people to buy it is sold for $100,000 — wealth creation and liquidity preference effects.

TallDave

Jan 1 2014 at 9:57pm

James,

Why would anyone exchange a bond for cash if the transaction were no more advantageous than exchanging a dollar for four quarters?

Because everyone’s perceived value is a little different. One person would rather have the bond, the other would rather have the cash. That’s not really an argument that the cash side of the transaction is objectively better (if “objectively better” even has real meaning in an economy of individuals for whom utility is in the eye of the beholder).

OTOH I do think the Fed can and does appreciably distort markets through OMOs. Then again, the Fed also distorts markets to a much greater degree merely by favoring us with delicate hints as to their future behavior. They could probably avoid most QE just by adopting a more sensible target.

John Goodman

Jan 1 2014 at 10:19pm

Good piece, Scott. Do you remember that “putting money into the market” was how John Kenneth Galbraith explained the Great Depression.

I’m serious. Galbraith thought money went into the market instead of into productive investment.

And this from an economist at Harvard?

Bob Murphy

Jan 1 2014 at 10:57pm

Scott,

If the various QE programs had focused exclusively on Treasury securities, and not at all on mortgage-backed securities, would that have had any effect on the MBS market?

Roger McKinney

Jan 1 2014 at 11:41pm

I’m not sure what this post is about, other than to nitpick about terminology. But I’ll comment on some statements:

So, where has ngdp growth been hiding these past 5 years?

That’s typical of mainstream econ which has no concept of time. The rest of us live in the real world where there actually is time. The Fed’s inflationary policies are the main reason that people in finance earn such high wages and have garnered most of the increase in real income over the past 20 years. Finance gets the new money first and can buy assets before prices rise.

The addition of capital theory and time in Austrian econ obviously makes it too hard for mainstream economists to understand.

James

Jan 1 2014 at 11:43pm

TallDave:

“Because everyone’s perceived value is a little different. One person would rather have the bond, the other would rather have the cash.”

Indeed, normal participants only enter into trades which they expect to make them better off. According to Sumner, those who sell bonds to the Fed are not made better off by the fact that they are directly involved in the transaction.

You and a few others have strayed into tangents on the details of price discovery but that’s not what matters here. Sumner is claiming that there is no benefit to being an early receiver of new money. Yet we observe a world in which there are financial institutions that seek to be in this position. Maybe Goldman Sachs pay traders huge salaries to sell bonds to the open market desk despite the fact that there is no advantage in doing so. Or maybe Scott Sumner is just mistaken. Which is more likely?

Mike Freimuth

Jan 1 2014 at 11:45pm

James,

People trade with the Fed because they think it makes them better off just like everyone else in every other market. There is nothing special about the motivation which induces people to buy from the Fed. People sell securities because they would rather have the money. Money from the Fed is the same as money from anyone else. This does not require the Fed to offer a special premium over the market price (as I said, it is possible that it would raise the market price but this is different).

Sumner is not making an error and that is the point of addressing your error. If you just assume that Sumner is wrong regardless of your ability to form a coherent criticism then you’re right I guess there’s no point in debating it. But if that is your approach, then why bother making a criticism in the first place?

Mike Freimuth

Jan 1 2014 at 11:56pm

James,

You are conflating two issues. Obviously it’s true that if the Fed, for some reason, pays someone more than what their securities are worth, that this would benefit them. Nobody (including Sumner) is disputing that, that’s just handing out money. I don’t know whether they do this or not but I’m sure that they would say that they don’t and there is certainly no reason that they must do this in order to buy securities.

The issue of whether it benefits someone to get “new” money is separate from whether they get extra money. It certainly does not benefit anyone more to get the “new” money than it would if they go “old” money and since the price of all securities goes up (or down) the same, it makes no sense to say that they are better off by getting the “new” money.

Yes, they may be better off because the Fed’s purchase increased the price of their securities, but this happens whether they sell to the Fed or not.

Dustin Irwin

Jan 2 2014 at 12:05am

Eric,

I see. What I don’t understand though is the claim that IOR reduces the money multiplier – because it is not clear to me that IOR reduces the supply or demand of credit or in any way incentivizes a bank to not lend against ERs. When a bank lends against ERs, money multiplier increases. I claim that if IOR were 0, money multiplier would still have decreased dramatically (ie, demand deposits would still not increase proportionally to the monetary base as exhibited by previous money multipliers).

Mike Freimuth

Jan 2 2014 at 12:32am

Dustin,

There is an important distinction between the behavior of individual banks and the aggregate affect on all banks. When an individual bank makes loans, it drains their reserves. Those reserves flow partially back to them and partially to other banks. This means that if all banks lend more, the total reserves will be unchanged but the amount of lending in equilibrium depends on the individual incentives of each bank. They will stop lending when it is no longer worth it to trade reserves for loans. The higher the IOR, the sooner (less loans) this will occur.

Dustin Irwin

Jan 2 2014 at 6:45am

Mike,

Yes thank you that is a very important distinction. I understand it as: The loan is likely made on account, which doesn’t impact reserves, though when the loaned money is spent to a deposit holder at a different bank, the reserve of the lending bank likely would be reduced. So this could have an impact then.

In your estimation, is it probable that a bank would forgo a lending opportunity at market rates to favor the IOR? Do you feel that the very large banks would assume such activity to very nearly be a wash as transferring reserves from one to another?

Michael Byrnes

Jan 2 2014 at 7:18am

Roger McKinney wrote:

“Finance gets the new money first and can buy assets before prices rise.”

From whom do they buy such assets?

James

Jan 2 2014 at 8:26am

Freimuth:

Draw your supply and demand curves for securities and identify the price at which the market clears before the Fed gets involved. If the asset market is efficient, then this price is what those securities are worth. Now draw a new demand curve to the right of the old one to represent the Fed’s demand. You’ll see that this price is higher than the one you identified earlier. This difference is a giveaway.

If the Fed pays extra for my securities, this doesn’t make you better off in any way except that you can say your securities are now priced higher. But no one is required to pay more for your securities. If you own a bond and I buy someone else’s identical bond for a small increment over the price that cleared the market before I showed up, you aren’t better off. Same when the Fed does it.

If I get the new money first, my purchasing power is greater because no one has bid up the prices of anything. If you get the new money last, prices are already bid up and you get no increase in purchasing power. So first recipients certainly do benefit.

If you disagree, don’t bother with convincing me. You can go as a consultant to all the primary dealers and tell them that their primary dealing operations are not adding value. See who believes you.

Scott Sumner

Jan 2 2014 at 9:09am

Ebsim, In my view the Fed has little impact on the real price of housing. They can boost the nominal price by creating lots of inflation (as in the 1960-80s).

James, The Fed buys at the going market price, the same price that you can sell to a third party.

MingoV, I think you missed the point. I said the metaphor would be harmless if it didn’t lead to sloppy thinking about causality. But unfortunately it does.

Philo, That may be right. I increasingly try to avoid terms like Austrian and MMT, as whenever I used them in the past people claimed I misunderstood the theory. So I respond to things I read in the blogosphere.

John, Galbraith said many questionable things.

Bob, A small effect, and almost no effect on the macroeconomy (as compared to buying something else). Again, I do think the market for the item bought by the Fed can be affected to some extent, especially when purchases are large, as under QE. But the MBSs bought by the Fed were backed by the Treasury, and hence were close substitutes for Treasury debt.

Scott Sumner

Jan 2 2014 at 9:13am

Roger, Fed policy in recent years has been contractionary. You claim the policy is inflationary, and yet doesn’t boost NGDP. That seems to be a contradiction.

Prices respond immediately to new information, so even people in finance do not benefit.

RPLong

Jan 2 2014 at 9:59am

Good first post, but I am wondering what the thesis statement is. If I had to guess, I would choose this one:

That makes sense to me, but I would like to read something a little more specific. In what sense do [others argue that] higher bond prices boost NGDP, and in what sense is that incorrect [according to Prof. Sumner]?

Patrick R. Sullivan

Jan 2 2014 at 11:04am

RPLong, bond prices–i.e. interest rates–are useless as an indicator of monetary policy and NGDP.

There are numerous forces acting to push and pull on interest rates, Fed policy is only one such force. It’s impossible to isolate just what monetary policy is doing, or has done, to interest rates. If you insist on thinking about monetary policy as working through interest rates you will only confuse yourself.

RPLong

Jan 2 2014 at 11:40am

Patrick Sullivan – Thanks. Actually, I was just trying to get a better handle on what Prof. Sumner’s blog post was about. I readily concede that I am no monetary policy expert, but I think I might be less confused than I may have lead you to believe.

Mike Freimuth

Jan 2 2014 at 3:32pm

Dustin,

Yes, now you’ve got it right. I think that in a world of excess reserves, banks are always operating where they think the marginal benefit of another loan is just equal to the benefit of holding the reserves (this constraint need not bind when a minimum reserve requirement is binding). To put it another way, if they are holding excess reserves, we are observing them foregoing loans in favor of IOR. Lower the benefit to holding reserves and you should see some loans that are not currently beneficial become beneficial and the quantity of excess reserves fall (I believe Scott would call this an increase in demand for money).

I’m not sure exactly what you mean by “such activity to very nearly be a wash as transferring reserves from one to another?” I’m not a banker so I don’t have a great sense of the market share that big banks have but I think small banks hold a sizable share of total deposits. In theory, the bigger the share of deposits a bank has the less increasing lending will drain its reserves (in expected terms at least) since more of them are likely to get deposited back in that bank.

As a thought experiment, I would say that if there were only a few large banks, they might be able to benefit by colluding to all increase lending but it seems unlikely that they could manage this with all the small banks. Also, once you start thinking of an industry as a monolith rather than a bunch of individuals (a common mistake by the way) then they would have to worry about changing interest rates, assuming they can’t price discriminate, and the whole analysis would be much different, so now I’m probably veering far off course. That is what happens when I try to answer a question I don’t really understand haha.

Mike Freimuth

Jan 2 2014 at 3:43pm

RPLong,

Regarding this: “In what sense do [others argue that] higher bond prices boost NGDP?”

If you change “higher bond prices” to “lower interest rates” and “boost NGDP” to “mean loose (or expansive) monetary policy” I think you will find that lots of people are saying that all the time. Scott sort of included several points that have been standard fare on his blog in this post but the main one that will probably be carved on his tombstone is “low interest rates don’t mean loose money.” He prefers to judge the stance of monetary policy by the growth rate of NGDP.

TallDave

Jan 2 2014 at 6:07pm

James,

Indeed, normal participants only enter into trades which they expect to make them better off. According to Sumner, those who sell bonds to the Fed are not made better off by the fact that they are directly involved in the transaction.

Sure, but trading with the Fed is not necessarily more advantageous than trading with anyone else. They could just as easily trade at market prices with anyone else.

Maybe Goldman Sachs pay traders huge salaries to sell bonds to the open market desk despite the fact that there is no advantage in doing so.

People are also paid lots of money to trade with entities other than the Fed.

TallDave

Jan 2 2014 at 6:23pm

You’ll see that this price is higher than the one you identified earlier.

But the difference is probably negligible, even for the Fed.

Mike Freimuth

Jan 2 2014 at 7:35pm

James: “You’ll see that this price is higher than the one you identified earlier.”

Dave: “But the difference is probably negligible, even for the Fed.”

Just to be clear, nobody is arguing that the Fed buying an asset doesn’t change the price of that asset, but if it changes, it changes for everyone holding that asset regardless of whether they sell it to the Fed or not.

Also, it isn’t always the case that this increase in demand necessarily increases the price of treasury securities because it also affects expectations about the stance of monetary policy which can have the opposite effect.

Roger McKinney

Jan 2 2014 at 9:09pm

It appears to be a contradiction because you assume that loose policy will automatically raise ngdp. If you don’t assume that, and assume that monetary policy can fail, then it’s not contradictory at all.

Some of us don’t think monetary policy is omnipotent. We want some empirical evidence that it works. The fact of loose policy without ngdp growth provides evidence that policy does not work.

Assuming that policy is tight because ngdp isn’t growing is the fallacy of assuming the conclusion.

Only stock market prices and bond prices respond immediately. CPI takes much longer, up to five years. The econometric evidence is very strong.

And if you don’t assume that monetary policy always works, the fact that ngdp hasn’t grown much is proof that prices don’t respond immediately.

Dustin Irwin

Jan 2 2014 at 9:57pm

Mike:

“To put it another way, if they are holding excess reserves, we are observing them foregoing loans in favor of IOR. ”

Agree – though my feeling is that even if IOR were 0, loans would be foregone. If a bank can’t beat .25%, something is wrong – and I think that something is other factors, including weak credit demand as well as what Scott just said in a recent post at the TheMoneyIllusion: “And monetary stimulus works, if it works at all, only if it is not expected to be withdrawn in the near future.”

http://www.themoneyillusion.com/?p=25730

Roger McKinney

Jan 2 2014 at 11:37pm

In addition, the rise in stock prices immediately after a policy decision isn’t the only price increase. The effect of policy changes takes a while to work out. In other words, while the effect might be immediate, it’s small and the immediate effect isn’t all of the effect.

Also, cpi increases will raise profits much later and cause another round of stock market price increases.

Dustin Irwin

Jan 3 2014 at 10:14am

James: “Now draw a new demand curve to the right of the old one to represent the Fed’s demand.”

Actually it only still represents the good ol’ total market demand – even if the new good ol’ total market demand is largely a function of the Fed’s demand. Primary dealers then increase bid-ask prices accordingly, with little final difference in the resulting bid-ask spread, which represents the primary dealers’ cut. The primary dealer will sell to anyone at that new ask price, Fed or private.

Scott Sumner

Jan 3 2014 at 10:21am

RDLong, I am arguing that for a given money supply, lower interest rates reduce NGDP. I’ll do a post on that soon, not sure which blog.

Roger, I think you misunderstood my comment. You had said that QE is inflationary, but failed to boost NGDP. That’s what I found contradictory.

I favor the creation of NGDP futures markets. In that case the stance of monetary policy would depend on the level of NGDP futures. Obviously the Fed is able to peg NGDP futures prices as high as it likes. I claim that a higher NGDP futures price peg will lead to higher actual NGDP growth.

Yes, goods prices respond slowly to monetary injections, but that has no bearing on anything I said in this post. People who get the money injections first can buy those goods before their price rises. But so can people (like me) who didn’t get the monetary injections first.

You refer to the “fact of loose money” but provide no evidence that money has in fact been loose.

TallDave

Jan 3 2014 at 11:24am

Roger,

So, where has ngdp growth been hiding these past 5 years?

Money has been too tight. That sounds odd (even insane) to people looking at interest rates and QE, but Fisher and Friedman predicted long ago that a successful inflation targeting regime like the Volcker/Greenspan/Bernanke era would over some decades lead to lower interest rates as lower expected inflation was gradually priced in, and QE with the current long-term targeting is like flooring the accelerator while standing on the brake — lots of noise and smoke and gas burned, but not much movement; the markets tend to shrug off temporary liquidity injections except insofar as they provide insight into the long term behavior of the Fed, which is what really matters.

If the Fed targeted NGDP growth, then you’d have a policy in which monetary policy was never too tight or too loose (or at least much less so).

TallDave

Jan 3 2014 at 11:32am

I claim that a higher NGDP futures price peg will lead to higher actual NGDP growth.

That’s very nearly a truism though, I think where we tend to lose people on the right/libertarian side of things is on the connection to RGDP — i.e. that there’s an NGPD path that maximizes RGDP growth as well as employment, etc.

Mike Freimuth

Jan 3 2014 at 3:39pm

Dustin,

I agree, we would probably still have excess reserves at 0% IOR. All I would venture to predict is that they would be somewhat less, I don’t know how much. Somebody somewhere probably has an estimate of the elasticity of supply of bank loans but it ain’t me. What if it were -1% though?

Naturally the quantity and price (interest rate) of loans depends simultaneously on supply and demand. I’ve always thought it was misleading when people on the news complain that “banks won’t lend” they could just as easily complain that “people won’t borrow” but that wouldn’t be nearly as populist.

I think the big issue for banks is the expected risk premium on the loans. I would gladly take out a large loan at .5% interest which would give them a small spread over the IOR but they wouldn’t be wise to give it to me haha.

Barry "The Economy" Soetoro

Jan 3 2014 at 4:57pm

For cripes sakes, of course we would still have excess reserves at 0%.

BANKS DON’T LEND OUT EXCESS RESERVES.

http://www.standardandpoors.com/spf/upload/Ratings_US/Repeat_After_Me_8_14_13.pdf

Dustin Irwin

Jan 3 2014 at 6:23pm

Barry,

No kidding. That was discussed at length in the exchange between Mike and I. Banks lend against ERs (ie, lending on account)… And guess what happens then? ERs become RRs. So no, there doesn’t have to be ERs.

Mike Freimuth

Jan 3 2014 at 9:52pm

Barry,

That is wrong. Here is a detailed critique of that paper.

http://realfreeradical.com/2014/01/04/banks-can-lend-out-excess-reserves/

Dustin Irwin

Jan 5 2014 at 9:56am

Mike

Regarding the negative IOR: I just don’t know. No doubt banks would be more inclined to do something with the money, though I need to get smart on the subject. For instance, if a bank invests in short term securities, are the reserves still reserves?? Though that would seem to have a stimulative effect as well due to boosting asset prices. Maybe some way or another then the -IOR would be stimulative.

Comments are closed.