Categories:

Economic History

Monetary Policy

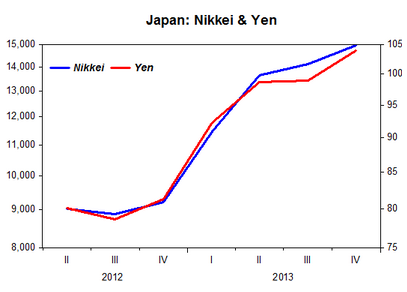

Back in 1933 the US had experienced years of deflation and nominal interest rates were close to zero. FDR sharply devalued the dollar over a period of 10 months, and stock prices closely tracked the value of foreign exchange during this period of monetary stimulus. Last year the Japanese did the same, and Marcus Nunes has a great post showing that the results were pretty similar. Here are some of his graphs:

That certainly looks like a positive correlation. Some people will say; “QE only helps the asset markets, it doesn’t boost NGDP.” I don’t know how something could dramatically impact stock prices without impacting nominal spending, but in any case NGDP growth picked up in Japan last year.

Others will ask; “What makes you think higher NGDP growth will lead to higher RGDP growth?” This does:

READER COMMENTS

Brian

Jan 17 2014 at 10:20am

Maybe I’m missing something, but I don’t see where the import/export graph shows faster growth for imports. The increases look about the same to me.

Otherwise, it’s a very interesting look at the effect of current Japanese policy. Things seem to be working as advertised.

Scott Sumner

Jan 17 2014 at 11:44am

Brian, The graph shows rates of change, not levels.

Brian

Jan 17 2014 at 2:17pm

Scott,

Thanks. That makes more sense. I think, though, that the axes would benefit from some labels. For example, I didn’t think the import/export graph was rates of change because the numbers are do high. Are these annual %, so that imports increased at ~27% annual rate in month 10, for example, or do the numbers show something else?

Marcus Nunes

Jan 17 2014 at 7:12pm

Brian

Sorry for my incompletness. The data are growth rates %YoY. Notice how both imports and exports showed no growth, taking off as soon as “Abenomics” takes effect. Exports rise (devaluation) but imports rise even faster (the income effect)

Greg Jaxon

Jan 20 2014 at 1:02am

What you’re calling an “income effect” could also be a dishoarding of yen-denominated assets in favor of hard assets or non-yen-denominated holdings that have to be imported.

Comments are closed.