During late 2012, market monetarists like myself argued that fiscal austerity in 2013 would not slow growth. We based that on an idea that was relatively uncontroversial as late as 2007 (even among New Keynesians)—monetary offset. If the central bank targets inflation, or NGDP, or inflation plus output gaps, it will try to completely offset the effect of any change in fiscal policy on aggregate demand. But with the onset of the Great Recession both Keynesians and conservatives stopped believing what they previously believed. Suddenly New Keynesians thought fiscal stimulus was expansionary. Old monetarists started talking as if low interest rates meant easy money.

Early in 2013 both

Mike Konczal and Paul Krugman indicated that 2013 would be the year when market monetarism finally got tested. It was quite a test, as the actual fiscal austerity was even greater than the Fed anticipated when it adopted QE3 and forward guidance in late 2012. This point is uncontroversial; even Keynesians talk about the unprecedented drop in the cyclically-adjusted deficit in 2013.

We don’t yet have all the 2013 data, but it’s clear that market monetarism passed the test with flying colors. Job growth through November occurred at a faster pace than 2012. During the first three quarters of 2013, real GDP growth is running well ahead of the pace in 2012. These are the sorts of statistics usually cited by Keynesians as barometers of the effect of austerity on demand. Oddly, Keynesians don’t seem to understand their own (AS/AD) model. Real GDP is a lousy indicator of aggregate demand, as it can just as easily be affected by shifts in aggregate supply. The appropriate indicator of AD is not real GDP, nor is it inflation, it’s nominal GDP—total spending in the economy.

Mark Sadowski sent me to a recent post by

Mike Konczal. I was looking forward to reading his admission that Keynesianism had failed and that market monetarism was now triumphant. Thus I was disappointed by what I saw:

2013. The year we won the argument but lost the war. It’s better than losing both the arguments and the war, I suppose.

2013 brought us a fiscal deficit that closed far too fast, NGDP growth and inflation falling compared to previous years, and unemployment completely falling off the political radar at the same moment the argument that the deficit was a worry collapsed. Before there were elaborate arguments about how the unemployed were this or that, or uncertainty was causing the one thing and the other. Now it’s just quiet out there, yet the economy remains below potential. The collapse of the counter-Keynesian position didn’t revitalize a position of aggressive action; it just left a void.

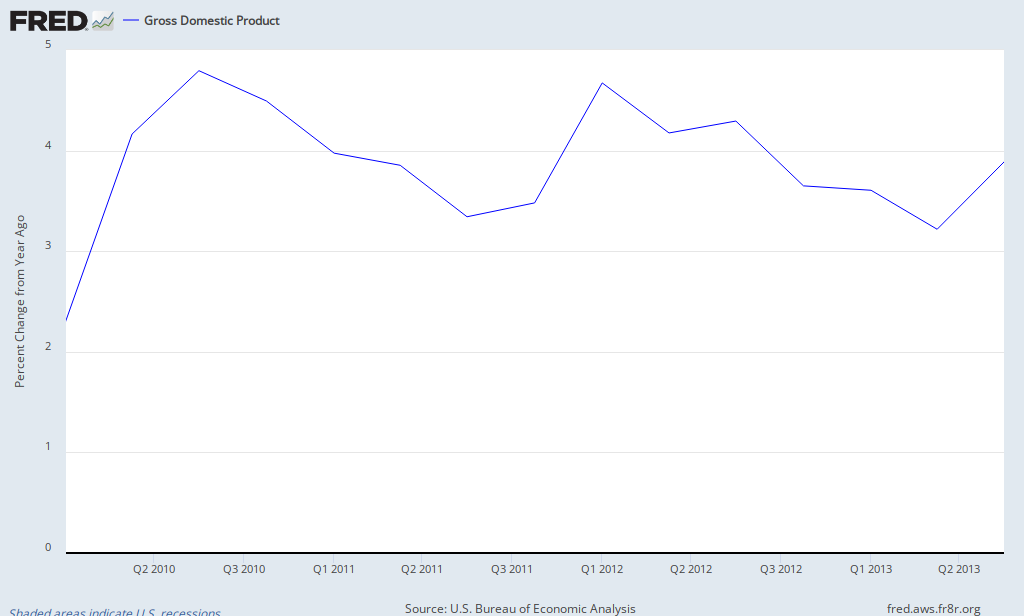

That sure doesn’t sound like an admission of defeat. Inflation is of course irrelevant to this issue, but NGDP is the right metric—give Konczal credit on that point. Unfortunately he has the data wrong. NGDP grew by 3.8% between 2011:4 and 2012:4, and is growing by 4.0% so far during 2013 (the fourth quarter is also expected to be strong.) That’s not much better than 2012, but market monetarism wins even if the two numbers are about equal. The speed up in jobs, RGDP, and NGDP growth is a disaster for the Keynesian model, suggesting a near-zero fiscal multiplier. Monetary offset worked.

It doesn’t matter how often John Cleese Eric Idle Michael Palin says the parrot is just resting; it’s still dead. And it doesn’t matter how many times Mike Konczal says that growth slowed in 2013—it accelerated. Keynesianism is not resting;it’s dead.

PS. I expect Paul Krugman to come up with a more plausible excuse. But will Keynesians stop claiming to be “reality-based”? Will they stop accusing conservatives of being “faith-based?” Don’t count on it.

{kind=link}

READER COMMENTS

Hunter

Jan 3 2014 at 9:59am

To be completely pendantic it was Eric Idle’s character that said the parrot was resting. John Cleese’s character was the one complaining that like Keynesism the parrot

“has ceased to be. He’s expired and gone to meet his maker. He’s a stiff, bereft of life, he rests in peace. If you hadn’t have nailed him to the perch he’d be pushing up the daisies. He’s rung down the curtain and joined the choir invisible. This is an ex-parrot!”

SG

Jan 3 2014 at 10:15am

Terrific post, Scott.

Here’s Krugman making a prediction that the sequester would cost the US 700,000 jobs in 2013.

http://www.nytimes.com/2013/02/22/opinion/krugman-sequester-of-fools.html

I suppose he could make the argument that absent the sequester that we really would have seen an extra 58,000 jobs every month last year, but when you take into account the fact that the Federal Reserve’s no-taper announcement in September explicitly said it was “taking into account the extent of federal fiscal retrenchment” such an argument becomes laughable.

[comment edited with commenter’s permission–Econlib Ed.]

RPLong

Jan 3 2014 at 10:22am

Wait a minute. Something’s not right here. Clearly NGDP growth accelerated YOY throughout 2012, but then it [NGDP growth] very clearly decelerates starting at 2013Q1. From there, relative to 2012, it is slower.

I am confused as to why Prof. Sumner refers to 2011-2012 growth when Konczal is very clearly talking about 2013. What am I missing?

Nathan Smith

Jan 3 2014 at 10:25am

My take on Keynesianism was here:

http://www.american.com/archive/2013/february/calling-the-keynesians-bluff

However, I think Old Keynesianism will persist as an “old time religion” until we find something else tidy enough to replace it in the undergrafuate macro textbooks. After all, Lucas and others were laughing at it thirty years ago. It has no predictive successes to its name. None. Mundell showed why it doesn’t work in foreign open economies. Foreign closed economies are generally not big anf capitalist enough for it to be relevant. so only the US economy is in play. There’s a kind of popular Legend the New Deal got us out of the Great Depression and that it vindicates Keynesian economics. But since the economy never really recovered during the Great Depression, but only regained its 1929 level in 1940, the 1930s look more like a cautionary tale than a triumph. WWII is sometimes used as a data point in favor of Keynesianism, but it would imply a negligible or negative multiplier, and anyway consumption shrank and we had price controls and everything was abnormal. Then in 1946 the Keynesians predicted disaster and we had a boom instead. This is the theory that never worked.

Scott Sumner

Jan 3 2014 at 10:34am

Thanks Hunter, I fixed it.

RPLong, You misread my post, I am comparing 2012 growth with 2013 growth. I’m not examining 2011 growth at all. Growth rates in GDP have risen steadily over the past 4 quarters, from a low level in late 2012.

And growth accelerated in 2013:Q1

Nathan Smith

Jan 3 2014 at 10:35am

But here’s my challenge to Scott Sumner: what should we put in undergraduate Principles of Macro textbooks instead of the Keynesian model? I have switched textbooks repeatedly since I began teaching principles 3 years ago in an effort to find the least embarrassing chapters on business cycles. I know use Tyler Cowen’s and Alex Tabarrok’s textbook. However, even that uses an aggregate demand — aggregate supply model. if someone could write a few chapters to replace that, I would consider using the rest of Tyler Cowen’s textbook and substituting in a few chapters by someone else to avoid teaching stuff I don’t really believe in.

So, in your ideal world, what would the undergraduate textbooks teach instead of Keynesianism? Maybe a topic for a future blog post? I’ll keep an eye out for it.

Dustin Irwin

Jan 3 2014 at 11:11am

RPLong

QSA GDP Growth

2011Q1 0.1%

2011Q2 1.4%

2011Q3 1.0%

2011Q4 1.3%

2012Q1 1.4%

2012Q2 0.7%

2012Q3 1.2%

2012Q4 0.4%

2013Q1 0.7%

2013Q2 0.8%

2013Q3 1.5%

http://research.stlouisfed.org/fred2/graph/?id=GDP

You may draw several meaningful inferences, the least appropriate of which is slow 2013 GDP growth relative to 2012.

Stating it another way:

Absolute NGDP growth for only 3 quarters of 2013 (2.3%) matches all 4 quarters of 2012.

Stating it another way:

2013 represents the first occasion of 3 consecutive quarters of increasing GDP growth since the depth of the recession in 2008.

And another way:

2013Q3 represents best quarterly growth since 2006Q1

RPLong

Jan 3 2014 at 11:41am

Thanks, Prof. Sumner. I see the issue now. NGDP growth slowed 3 out 4 quarters in 2012, and grows slightly in the two quarters of 2013 in Konczal’s graph.

However, it is not clear from his post (“…NGDP growth falling compared to recent years…”) that he is specifically talking about 2013 growth in isolation. He links to data with a clear downward trend beginning in 2010.

It’s definitely true that NGDP grew in 2013, but I think that is a bit narrower scope than Konczal’s point.

Just my two cents…

Dustin Irwin

Jan 3 2014 at 11:45am

Correction – 2012 growth was ~3.8%, not 2.3% as I stated above. However, growth was trending down throughout 2012, whereas it has been trending up throughout 2013 since bottoming out 2012Q4.

AD

Jan 3 2014 at 11:55am

Nathan,

From what I can tell, Cowen and Tabarrok’s AD/AS model is consistent with Scott Sumner’s framework, because essentially AD shocks are NGDP shocks, whereas the standard AD/AS in most textbooks is not.

Daublin

Jan 3 2014 at 12:02pm

It’s far from uncontroversial that 2013 was a year of austerity. We spent about as much per capita as during World War II. Even during the brief period of the so-called shutdown, spending was at levels from around 2001.

“…this lower budget deficit for 2013 hardly qualifies as austerity.”

– http://conversableeconomist.blogspot.com/2013/11/goldilocks-fiscal-policy-just-about.html

Gene

Jan 3 2014 at 12:42pm

To be even more pedantic than Hunter, Eric Idle was not in the parrot sketch at all. The shopkeeper was Michael Palin.

Nathan Smith

Jan 3 2014 at 12:49pm

@ AD:

Cowen and Tabarrok do reframe the Keynesian AD/AS model in a way that makes it closer to Scott Sumner’s framework. Maybe this will help a bit: There are two charges that can be made against Keynesian economics, depending on how it’s formulated: that it’s false, and that it’s meaningless. Cowen and Tabarrok’s version shifts from the false towards the meaningless. Of course, the chapters contain plenty of particular facts, say about how Fed policy works, which are meaningful and true; but the overall theoretical framework in which these facts are embedded is intellectually unsatisfying. I don’t feel like I’m lying to students, but I don’t feel that I’m serving them particularly well either. The contrast with the micro material, with supply, demand, and equilibrium, is painful. So much dynamite insight in the first half of the course, more vapid hand-waving in the second half.

Does Scott think that Cowen and Tabarrok’s version of AD/AS is good enough? What else would he want to change?

Andy Wood

Jan 3 2014 at 1:04pm

@Gene:

So Eric Idle refused to appear in the parrot sketch, so that, forty-odd years later, he could be even more pedantic than Hunter? I think that’s extraordinary.

jb

Jan 3 2014 at 1:14pm

It would be even better if this was titled ‘Keynesianism is pining for the fjords’

(he also said he was resting, but pining for the fjords is much funnier)

brendan

Jan 3 2014 at 3:58pm

Basically, any idea that a intellectual/political movement has been fighting viciously on behalf of, for decades on end, is un-killable by evidence. Admission of defeat on the deficits-are-stimulative idea amounts to stomping on Paul Samuelson’s grave, by his direct heirs, on behalf of Milton Friedman’s heirs.

Robin Hanson’s “politics are tribal status wars” idea is more depressingly correct than I ever would’ve guessed. I really hope I can age with out succumbing.

[comment edited by commenter–Econlib Ed.]

TallDave

Jan 3 2014 at 4:00pm

Alas Keynesian models’ superior plumage will ever overshadow their paltry concinnity. The fanciful but popular notion that the state can create prosperity at will if the planners are just willing to spend more money resists all empiricism.

Barry "The Economy" Soetoro

Jan 3 2014 at 4:54pm

“The fanciful but popular notion that the state can create prosperity at will if the planners are just willing to spend more money…”

Agreed, this is absurd. However, Scott is basically something equally asburd; “The state can create prosperity at will if the planners are just willing to print enough money.”

Also, 100% chance they buy the assets of the 1% every time. Why?

W. Peden

Jan 3 2014 at 5:18pm

Daublin,

Here we come across my objection to most of the austerity debate: ‘austerity’ is not a term with a standard operational definition, so there is tremendous leeway for claiming that austerity isn’t going on or is going on, depending on whether it suits the argument. Thus, in 2012 when the UK economy was doing badly, people on the right tended to argue that “austerity hasn’t been tried” and people on the left tended to argue that “our (current) policies of austerity are killing growth”. Now, in 2013, people on the right (at least the UKIP-supporting, send-the-foreigners-home, save-marriage and stick-em-up-to-Brussels right) are still arguing that the UK hasn’t had austerity at all, but ever since the UK economy started growing again, I’ve seen some left-wing economists break ranks and claim that Osborne had a fiscal stimulus in 2012 rather than austerity, e.g.-

http://mainlymacro.blogspot.co.uk/2013/12/osbornes-plan-b.html

So whether or not Keynesians think that an economy is undergoing fiscal austerity does seem to depend on whether RGDP is doing badly or not, making “fiscal austerity in zero-interest rate situation causes recessions” a fundamentally meaningless claim, unless Keynesians operationally define ‘austerity’ e.g. “a reduction in the budget deficit/increase in the surplus, cyclically adjusted”.

Scott Sumner

Jan 3 2014 at 6:19pm

Nathan, Some coverage of Keynesianism is needed because most of the world thinks in Keynesian terms. Students need to understand how American policymakers think about the economy. I like the AS/AD model, although I’d prefer the AD curve be drawn as a hyperbola. It’s not a Keynesian model, it’s essentially the model that pre-Keynesians had in mind during the 1920s. It’s the model Keynes criticized in the General Theory.

If market monetarism becomes successful then maybe our model will be added to textbooks.

Cowen/Tabarrok and Mankiw are both good texts.

AD should equal NGDP, either levels or rates of change. They should be called “nominal shocks” not “demand shocks”, it has nothing at all to do with “demand.” Maybe I’ll do a post.

RPLong, I’d suggest not looking at Konczal’s graph, and instead look at the actual data, which is different from his graph. His graph appears to be an attempt to make 2013 look bad. When the correct data is used it becomes clear that growth accelerated in 2013. I don’t know why he doesn’t use the correct data.

Daublin, The point is that Keynesians consider 2013 to be very austere, and hence their model is wrong. You and I may not consider it austerity, but that’s a separate issue.

Brendan! Please insult me with polite language!!

Barry, No, that’s not my view, as you’ll discover if you keep reading my posts. I am a (moderate) supply-sider. Prosperity requires good supply side policies. NGDP targeting won’t help North Korea.

Foobarista

Jan 3 2014 at 6:20pm

It’s hard to see how “Keynesianism” dies – it’s simply far too useful as an intellectual crutch for politicians who want to spend money. How will you argue that hiring a few million more bureaucrats is a wonderful economic investment that will pay off with magic multipliers without Keynesianism?

If you’re a politician, Keynesianism is good, and public choice theory is evil.

Mike Konczal

Jan 3 2014 at 9:30pm

– Scott: “[Konczal’s] graph appears to be an attempt to make 2013 look bad.”

Just so it’s clear, that graph is the marker David Becksworth put on the table, austerity-vs-NGDP-wise, at the end of 2012, and one I’ve been watching since:

http://macromarketmusings.blogspot.com/2012/12/paul-krugman-will-not-like-these-figures.html

TallDave

Jan 3 2014 at 10:36pm

Agreed, this is absurd. However, Scott is basically something equally asburd; “The state can create prosperity at will if the planners are just willing to print enough money.”

NGDPLT seeks an NGDP path that is optimized, not maximized. Market monetarism has times and places for monetary policy that is both tighter and looser than today’s.

Mike Konczal

Jan 3 2014 at 11:04pm

Also, correct me if I’m wrong Scott, but isn’t my graph, the one you are criticizing, the *same exact* graph you submitted as your Most Important Graph for 2013, except I updated it with the actual 2013 data?

http://www.theatlantic.com/business/archive/2013/12/the-most-important-economic-stories-of-2013-in-44-graphs/282193/

JohnB

Jan 4 2014 at 1:02am

Tall Dave,

NGDPLT does not seek an NGDP path that is optimized or maximized. Rather, Sumner selected 5% NGDP growth per year because that was roughly the average from 1985-2007. There’s no a priori optimal number for NGDP growth.

W. Peden

Jan 4 2014 at 10:04am

JohnB,

That’s true, although there are empirical arguments for one NGDP number over another, e.g. someone very concerned about sticky wages would want a number greater than the trend rate of output, in order to produce an inflationary price-trend; if you thought that the distortions discussed in Milton Friedman’s “The Optimal Quantity of Money” were very very important, you’d want to have a very deflationary trend; whereas George Selgin has arguments in “Less Than Zero” for a mildly deflationary number.

However, it is true that, from a market monetarist point of view, the key problem is with instabilities in the path of NGDP, rather than any particular path. An extremely erratic and unpredictable path, fluctuating from depressions to 1970s-style inflations, would be much worse than a very steady -5% contractionary trend or a 15% inflationary trend.

Tom

Jan 4 2014 at 11:15am

@ Dustin Irwin

The numbers you posted disagree. From Q3 2011- Q1 2012 it increased from 1.0 to 1.3 to 1.4.

Nathan Smith

Jan 4 2014 at 11:52am

“I like the AS/AD model, although I’d prefer the AD curve be drawn as a hyperbola.”

Fascinating.

But should we be supposing there is something at the macroeconomic level corresponding to try sticking price-taking in microeconomics? That is, do consumers observe the level of prices, or the rate of price growth, and then decide how much to consume? But if AD is a hyperbola, then there will be two spending levels, or rates of real spending growth, that correspond to a given rate of price growth.

Without “price level taking” in any sense, how is AD defined?

Scott Sumner

Jan 4 2014 at 12:35pm

Mike, You are clearly suggesting that the data points shown on the graph for 2013 reflect NGDP growth during 2013. But they don’t, they largely reflect NGDP during 2012, when austerity had not yet started.

If David used them to show long run trends that’s fine, but they don’t tell us anything about the before and after effects of austerity. That point is not even debatable.

Nathan, I don’t follow your comment. You can think of the curve as price level takers, although I prefer a different approach. I prefer to view NGDP (AD) as being determined by monetary policy, and then the split between P and Y being determined by SRAS, i.e. the degree of price stickiness, etc.

marmico

Jan 4 2014 at 12:49pm

[Comment removed pending confirmation of email address. Email the webmaster@econlib.org to request restoring this comment. This is your final notice. We have tried to reach you previously and you have not responded. A valid email address is required to post comments on EconLog and EconTalk.–Econlib Ed.]

TallDave

Jan 4 2014 at 1:17pm

JohnB,

The assertion is only that some optimal NGDP path exists.

By definition nominal gross domestic product level targeting is an attempt to achieve some particular NGDP path.

Roger McKinney

Jan 4 2014 at 1:41pm

This seems one sided. If the opposite happens, market monetarists insist it is proof that monetary policy is too tight, not that ngdp targeting failed.

If job growth and real gdp increases are proof that ngdp targeting working, then the opposite should be proof that it has failed.

And it is very likely that the economy improved in spite of monetary policy, not because of it. After all, more is happening in the economy than just monetary and fiscal policy. Micro factors are far more powerful. Seems to me that macro economists take credit for things the micro economy is doing.

That’s more worthy of politicians than economists. Politicians take credit for every good thing that happened during their administration whether they played any role in it or not.

Nathan Smith

Jan 4 2014 at 2:00pm

“Nathan, I don’t follow your comment. You can think of the curve as price level takers, although I prefer a diffof oach. I prefer to view NGDP (AD) as being determined by monetary policy, and then the split between P and Y being determined by SRAS, i.e. the degree of price stickiness, etc.”

Maybe we would need to be drawing on blackboards to understand each other. This remark seems like a description of Cowen’s presentation in the textbook. But Cowen draws AD as a straight line. If NGDP is determined by monetary policy and split between P and Y, how can AD be a hyperbola?

magilson

Jan 4 2014 at 2:17pm

Scott,

The medicine you prescribe appears to have worked better than the medicine prescribed by the *whatever*-Keynesians. But could you address the statement by one of the practitioners that no one really understands why?

I hope you will respond to this. Victory is meaningless if one doesn’t understand the why. I suspect he over-stepped his purview and should have said “I” instead of “We”.

Brian

Jan 4 2014 at 3:54pm

Mike Konczal,

As Scott has pointed out, the graph you provide doesn’t attribute NGDP to the correct time scale since it shows year-over-year growth. The 4Q 2012 point shows the growth for all of 2012 and that’s only 3.8%. Even worse, the year before austerity (which began in spring 2013) had YOY growth of only 3.0% That’s the pre-austerity baseline that matters. But with post-austerity growth at 4.0%, it seems clear that growth has accelerated, not declined, since the sequester began. Granted, the final analysis can’t be done until 1Q 2014 ends, but Keynsianism is not doing well. Not dead, perhaps, but on its deathbed with the end in sight. In any case, you’ve certainly lost both the argument and the war.

Steve

Jan 4 2014 at 9:25pm

Keynes wrote a lot. A specific element of Keynes is claimed to be dead, sure, as all real positivist science should be a measurement and re measurement. (See Kuhn and Polanyi)

Mr. Sumner, its great to read your comments and observations. Paradigms breaking is a tough business. I salute you.

Side note, why don’t you pull the antiKeynes circlejerk stuff? The guy lived and wrote constantly for 30 years… his entire body of work is not dead due to this non random and hardly unbiased review.

dajeeps

Jan 4 2014 at 11:17pm

@ Roger McKinney:

Mr. Sumner is talking about monetary offset of changes in fiscal policy in this post, not NGDP level targeting. NGDP level targeting hasn’t been tried.

[broken link fixed. Please check your links before submitting comments.–Econlib Ed.]

Mark A. Sadowski

Jan 5 2014 at 10:23am

Tom,

“The numbers you posted disagree. From Q3 2011- Q1 2012 it increased from 1.0 to 1.3 to 1.4.”

That’s two increases, not three.

Dustin Irwin

Jan 5 2014 at 1:55pm

Thanks, Mark ^

I posted a similar response that didn’t appear…

[Dustin, all your comments have been posted. Some were temporarily trapped by the spam filter but they are all posted now. If something didn’t appear you may not have hit the Submit button for it.–Econlib Ed.]

Dustin Irwin

Jan 5 2014 at 2:09pm

Brian. “but Keynsianism is not doing well. Not dead, perhaps, but on its deathbed with the end in sight. In any case, you’ve certainly lost both the argument and the war.”

2013 only shows that there is more to invigorating the economy than fiscal policy alone. If that ‘more’ is entirely MM, then what of Keynesianism in a world lacking a courageous, willing, and dutiful CB (ahem, Europe…).

Brian

Jan 5 2014 at 9:40pm

“2013 only shows that there is more to invigorating the economy than fiscal policy alone.”

Dustin Irwin,

No, I think it shows that neither fiscal nor monetary stimulus/austerity has much effect.

Let’s be clear: ~4% growth this year over a 3.8% growth base in a slowly recovering economy is basically a null result. There’s no evidence of any effect. That either means that two large effects–austerity of the sequester/shutdown and the stimulus of QE3–cancelled each other exactly, or it means that neither one has much effect. Exact cancellation would be fortuitous and is therefore unlikely. Based on the evidence, then, the only supportable conclusion is that neither stimulus nor austerity has much effect.

This conclusion is supported by the trends of the last 5 years. Most years we have had both fiscal and monetary stimuli (these supposedly large effects have been working together), but recovery has been painfully slow and there’s no evidence that the recovery has been any faster than it would have been without stimulus. Since the effect is unobservable whether fiscal and monetary work together or oppositely, I have to conclude they are both small, if not negligible.

All this stimulus appears to be little more than a lot of bluster to show that we’re doing SOMETHING, but without significant effect.

Dustin Irwin

Jan 5 2014 at 11:56pm

Brian,

I’m not sure what you’ve stated is inconsistent with what I’ve said. Any model that predicted lower deficits = lower growth is flawed (objective statement). Something is driving our growth, however unimpressive it is (subjective statement). It could be MM, it could be non-policy related as you claim, could be both or even other (it is unclear to me!); this is a secondary debate. Gathering the facts first, though, is crucial to informing such a debate – and an obvious fact is that ZLB growth isn’t always dictated by fiscal policy, and it seems you agree.

Pete Harvard

Jan 12 2014 at 3:38pm

Scott (or anyone),

I don’t get the distinction between real and nominal GDP that you make. How can nominal GDP only reflect AD, but real GDP can also be influenced by AS? Why isn’t nominal GDP affected by AS, while real GDP is?

Thanks!

Comments are closed.