You may recall a famous saying by Herb Stein:

If something can’t go on forever, it won’t.

I don’t quite believe that, although I must admit that Stein has me beat on logic. But I’ve noticed that when people say something can’t go on forever, the day of reckoning never seems to arrive. For instance, inflation hawks tell me the Fed can’t just keep increasing nominal GDP forever (at say 5% per year.) Why not?

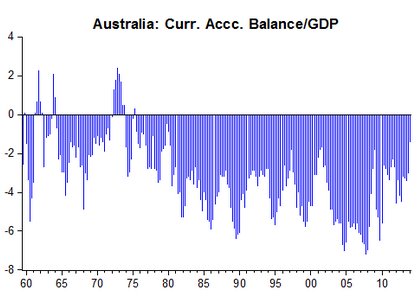

Then there are the countries that are “living beyond their means,” such as Australia and the USA. The US has run current account deficits for many decades. Some claim we benefit because the dollar is the international currency of choice. This is called “exorbitant privilege.” Nonsense. Australia’s been running huge CA deficits for longer than the US. Here is a graph from Marcus Nunes’ excellent post; as you can see Australia typically runs a current account deficit of about 4% of GDP, and has been doing so essentially forever.

Is the Australian day of reckoning about to arrive? Well they probably will have a recession some day, although by keeping NGDP growing at a fairly healthy rate, and coming back to the trend line when they deviated, they’ve avoided the 2001 and 2008-09 recessions. Their last recession was in 1991, even though in theory a commodity-based economy should have more recessions, as the real side of the Aussie economy is much less stable than the US.

Why do people think the Aussies can’t keep running CA deficits forever? Because they were taught that a CA deficit means that you are borrowing money from the rest of the world to support your consumption. “You are living beyond your means.” Not true, consider the following data point from Australia:

In Australia, foreigners bought a record 14 percent of new properties in the first three months of the year, based on a survey of property professionals by National Australia Bank Ltd.

Suppose some Australian workers built a condo on the Gold Coast, and sell it to a Chinese investor. They take the $500,000, and buy 50,000 sneakers made in China by Chinese workers. This shows up as a $500,000 current account deficit for Australia. That’s because they are importing “goods” and exporting “assets.” But this is clearly nonsense. Indeed the word “deficit” does more to confuse than enlighten. All trade is two-sided; there are no international “deficits.”

Here’s what we should be talking about. Is the Australian government living beyond its means? Is it borrowing too much? No, it has one of the lowest national debts of any developed country, 29% of GDP. That’s far less than half the ratio of Germany; a country no one thinks is living beyond its means.

How are Australian corporations doing? I don’t know, look at the stock market. How about households? The point is that countries cannot “live beyond their means.” That’s not to say that certain people, businesses and governments within a country cannot borrow too much—look at Greece. But you don’t know that from international “deficits,” you know that by looking at Greek fiscal policy, or banking policy, which was reckless during the go-go years.

Predictions:

Social Security will go on and on.

The US will keep running budget deficits for decade after decade.

Australia and the US will keep running current account deficits.

Germany will keep running CA surpluses, as will East Asia.

The NYC/LA/SanFran/London/Dubai/Shanghai/HongKong/Singapore/Sydney housing bubbles will never burst. There will be times when they appear to burst, but it will be an illusion. Prices will bounce back.

Peak oil will keep getting delayed.

NGDP will keep going up and up.

The Spurs will still be winning titles when Tim Duncan is 87 years old.

Unfortunately Herb Stein couldn’t go on forever; he was a voice of reason in an often crazy profession.

READER COMMENTS

Chris Hallquist

Aug 2 2014 at 9:22am

One objection: a bubble that never bursts isn’t a bubble. The cities you mention are expensive because demand for them has grown faster than supply. Demand won’t collapse unless the underlying industries that drive those cities collapse, a la Detroit. I do think it’s possible, though, that in the face of increasingly high prices the leaders of those cities will come to their senses and enact policies to increase supply (taller buildings, mostly), thereby stabilizing prices.

Ian

Aug 2 2014 at 9:38am

Why does social security have to go in forever. Whyyyyyy? Please make it stop. -24 year old

Greg G

Aug 2 2014 at 9:38am

Nice post Scott. Your original thinking and sense of humor keep me coming back even when I am not sure you are right.

In this case an economy that sustains long term growth can sustain the growth of many other factors. When Hamilton convinced the Congress to take on the debts of the states many predicted that would soon cause the financial ruin of the country. And ever since, many have been predicting that a continuous increase in the nominal national debt will ruin us. That ruin has always been…just around the corner.

Yes, I understand that their argument is that the debt will eventually prevent the very long term growth that makes its increase possible. When will this happen? Just around the corner.

( I think you may be right about the Spurs too.)

Hazel Meade

Aug 2 2014 at 10:17am

[Comment removed for crude language. –Econlib Ed.]

Tom West

Aug 2 2014 at 10:42am

I think a lot of people cannot help but assume that the rules that bind personal finance must in some way eventually bind government and businesses.

That engenders this feeling that when countries do violate the rules of good personal finance, they should eventually be punished for it. After all, that’s how the narrative goes.

Feelings of disgust that the USA and other nations haven’t gotten their comeuppance for their “profligate” ways by people who would be severely affected by that reckoning don’t seem uncommon.

Conformance to the narrative is important.

Scott Sumner

Aug 2 2014 at 11:01am

Chris, Yes, I agree that a bubble that never bursts is not really a bubble. I should have used scare quotes around “bubble,” I was trying to be sarcastic.

Ian, I wish we had a fully funded system with private accounts–but we don’t.

Greg, Yes, but just to be clear I do think some governments borrow too much—Greece and Argentina are obvious examples. The US would probably have done slightly better with smaller deficits, but it’s not really a major game changer for us.

Tom, Good point about personal finance analogies. Try this:

Imagine a family business in Britain passes on from one generation to the next. The total indebtedness of the family is described by this formula:

Year*10 pounds = total debt.

In other words, they owed banks 18,500 UK pounds in 1850, and now owe banks 20140 UK pounds. They do repay old debts when due, but take out new ones to keep their total indebtedness rising at 10 pounds per year. That family:

1. Runs a “budget deficit” of 10 pounds per year.

2. Can keep running that deficit essentially forever, or at least as long as the family dynasty lasts.

mike davis

Aug 2 2014 at 12:22pm

Here is Herb Stein on the current account (from Econlib Encyclopedia).

I miss Herb

Brent

Aug 2 2014 at 12:56pm

Of course, sometimes bad ideas are just so big yhey take a long time to fall. The Roman Empire, British Empire, Soviet Empire, etc. come to mind…

bill

Aug 2 2014 at 1:22pm

Ian,

If Social Security stops, be prepared to spend the money you save in taxes to make payments to your parents to replace the money they were going to get from Social Security. In your individual case, that may be a good thing (or not, I don’t know you), but for the various age cohorts involved, it will be about a wash.

i don’t want destitute old codgers rooting through my garbage cans, so I’m glad we provide a minimal income safety net.

AbsoluteZero

Aug 2 2014 at 2:55pm

Scott, good post and good example in the comment.

Yes, this is another one of those weird things that many people believe. And it’s not just that they use analogies from personal finance. If a person’s assets keep going up, the number gets more positive, they think that’s obviously good. But to them debt is somehow inherently bad, and increasing debt means things are getting worse. What they don’t understand is you can have both, and it can be sustained. If things are getting worse, they believe eventually something catastrophically bad must happen. In essence they confuse “bad” with “not sustainable”. A second, related issue is they often count only one side, they look at only the debt and ignore what the debt was used to buy.

vikingvista

Aug 2 2014 at 4:23pm

Who are these economists and pundits who, after studying the issue, don’t grasp that in the *balance* of payments, a current account deficit is balanced by a capital account surplus? The words “deficit” and “surplus” seem appropriate and not susceptible to accidental misuse by people who are paid to understand these things. I can’t think of better terms.

It is hard to believe that such people are not deliberately misusing the terms, trying to trick passersby into projecting their distaste for government debt into support for protectionist or cronyist legislation.

For such people, I don’t think education is the solution, since I believe they already understand. Education is only a solution for mopping up the damage they’ve done to the minds of others. For them, the best solution is probably shame.

Jody

Aug 2 2014 at 4:50pm

I think the real issue is many use the statement to misdirect from flaws in a claim of unsustainability.

Eelco Hoogendoorn

Aug 2 2014 at 5:09pm

This post seems confused to me. Especially the notion that personal and national finance are fundamentally different. The only fundamental difference is that a monetary sovereign may choose to deflate away any debt denominated in the currency it issues. That’s an important difference, but inflating away your own debt isn’t a free lunch either, of course.

Yes, debt isn’t really that big a deal if your income/GDP rises faster than said debt. If it doesn’t, and you cant (see Greece) / don’t want to inflate it away, you are in trouble. Sure, deficit spending is not bad per-se; sometimes its better to save; but if you can identify genuine investments whos borrowing costs will pay for themselves, all the better of course.

Bu saying that running a deficit is per definition a-ok because all trade (including in government bonds) benefits both sides, is nonsense. Government can (and will) stay irrational longer than you can stay solvent/alive. For instance, selling off hard assets in order to buy bread and games may increase utility in an advance-auction-of-stolen-goods sort of way, but assets are limited, whereas the demand for bread and games is a bottomless pit.

Every 4-year term government who knows what is politically good for itself will manage to convince itself that now is the time to ‘invest in the future’. You know, now that they get to decide what that means. As a consequence, democratic nations tend to operate closer to the brink of default, than to a level of debt that is optimal in any sense.

Shane L

Aug 2 2014 at 6:10pm

“Is the Australian government living beyond its means? Is it borrowing too much? No, it has one of the lowest national debts of any developed country, 29% of GDP.”

Just a word of caution: Ireland’s debt to GDP was 24.8% in 2007; by 2014 it was nearly 124%.

http://www.tradingeconomics.com/ireland/government-debt-to-gdp

These things can change very quickly if private debt and public promises based on assumptions of continuing growth are confronted by a sharp reversal.

Rajat

Aug 2 2014 at 6:11pm

Thanks, Scott, this is great post. In the 1980s, Australian policy makers were terrified of the high CAD and tightened fiscal and monetary policy on numerous occasions to reduce it to ‘sustainable’ levels. Then John Pitchford came along with the ‘consenting adults’ argument to say that as long as the CAD was mainly due to private decions, it shouldn’t matter and policy could focus on other things. Unfortunately, our high school econ students are still taught about the importance of ‘external balance’ and almost everyone believes in the Australian housing ‘bubble’. Fortunately, the government has so far shied away from macroprudential policies, but if house prices keep increasing, as they will probably do if the RBA seeks to tackle an expected fall in our terms of trade with low rates, the government may feel compelled to ‘do something’ like the RBNZ has. But is far, so good.

Anand

Aug 2 2014 at 10:08pm

“Greg G writes:

Nice post Scott. Your original thinking and sense of humor keep me coming back even when I am not sure you are right. ”

+1

Floccina

Aug 2 2014 at 10:12pm

Right but interest on the debt cannot grow faster than NGDP forever. Eventually the bond market will notice.

Lorenzo from Oz

Aug 3 2014 at 12:14am

If one imports capital to build assets to generate income then one can just keep importing capital. As Australia has essentially been doing continuously for 200 years. (I can remember working that out in the 1980s and then being puzzled why others couldn’t.)

One concern is everything ends up foreign owned. But if the asset base keeps expanding, that does not happen.

Shane L: hopefully, no Australian government would be so stupid as to guarantee past and future bank lending in the middle of a global financial crisis as the Irish government did. And we really seriously believe in a floating exchange rate.

Also, Australia has about the same level of total debt to GDP as other OECD countries, it is just that private debt is a much higher proportion of it.

bill40

Aug 3 2014 at 3:07am

One small quibble if I may. The property market crashed in Tokyo and hasn’t recovered in over two decades.

Ralph Musgrave

Aug 3 2014 at 6:10am

Congratulations to Scott for his discovery that deficits don’t matter (as long as they don’t cause excess inflation). That’s what MMTers have been saying for years.

Vangel

Aug 3 2014 at 10:29am

Social Security will go on and on.

No it won’t. SS has kept going because as long as the Ponzi scheme had more funds coming in than had to be paid out there was never any problem that could not be papered over.

The US will keep running budget deficits for decade after decade.

Only if the deficits are financed by their central banks AND if investors remain unconcerned.

Australia and the US will keep running current account deficits.

As with SS this never ran into the reality problem. As long as the US could live off its accumulated capital and there were few alternatives to the USD borrowing to consume was not a big issue for investors looking for a return over a short period of time. But if we look around we find that lenders are not falling over themselves buying long dated USTs and countries are working to get around the USD when conducting international trade. Americans, and economic analysts, may be in the same position as a turkey a few weeks before Thanksgiving. Their whole lives things have been good and relatively worry free. There will be only one event when that will not be true but once that event comes they will not have the time to reassess their view of the world.

The NYC/LA/SanFran/London/Dubai/Shanghai/HongKong/Singapore/Sydney housing bubbles will never burst. There will be times when they appear to burst, but it will be an illusion. Prices will bounce back.

I used to live in a city where real estate prices peaked during the Tang Dynasty. On one of my vacations I visited a city in which real estate prices peaked 5,000 years ago and many in which house prices reached their highs more than 2000 years ago. I am sure that the inhabitants of these cities, some of which are still around today, felt the same way.

Peak oil will keep getting delayed.

Yet conventional oil production peaked around 2005 and shale producers rely on lender financing to keep going and are still cash flow positive even a decade after they began operations. Economists may also try to figure out the difference between resources and proven reserves. When reserve increases go up because the SEC changed the rules you might want to look at the data once again by applying the same rules for the entire series length.

Hopaulius

Aug 3 2014 at 12:22pm

CO2 will continue to accumulate in the atmosphere, but the Arctic will continue to freeze, Antarctica will remain frozen, and I will continue to play at the same beaches in the same locations where I played as a child.

Scott Sumner

Aug 3 2014 at 3:38pm

Eelco, You said:

“This post seems confused to me. Especially the notion that personal and national finance are fundamentally different. The only fundamental difference is that a monetary sovereign may choose to deflate away any debt denominated in the currency it issues. That’s an important difference, but inflating away your own debt isn’t a free lunch either, of course.

Yes, debt isn’t really that big a deal if your income/GDP rises faster than said debt. If it doesn’t, and you cant (see Greece) / don’t want to inflate it away, you are in trouble.”

That’s my view as well–so what confuses you?

Shane, That’s true, but their debt problems were not caused by an excessive public debt in 2007, but rather the Irish government’s decision to give enormous quantities of taxpayer money to foreign investors.

Rajat, I’d like to see them pop the housing bubble with zoning law reforms.

Ralph, You keep misrepresenting what I say. Where did I say budget deficits don’t matter?

Vangel, I notice you don’t mention which cities.

Hopaulius, No, the Earth really will get warmer.

Scott Gustafson

Aug 3 2014 at 3:39pm

We will always have about 20 years worth of “proven” reserves of whatever mineral you want. Spending money proving up reserves to be produced more than 20 years in the future makes no economic sense at any reasonable discount rate. At less than 20 years, it starts to make a lot of economic sense.

Dan King

Aug 3 2014 at 6:23pm

Something that can’t go on forever, won’t…

You only dispute the premise. CA deficits can go on forever, and therefore Mr. Stein’s logic does not apply.

Comments are closed.