Last November a lot of pundits were telling us that falling oil prices were good for the economy. I criticized that view:

Rising oil production is likely to lead to faster global growth. Falling oil production is likely to lead to slower global growth. That’s because oil is an important input into the production process.

However falling oil prices have no implications for global growth—it merely redistributes global wealth.

Even in December, these claims were still being made:

WASHINGTON (Reuters) – The recent drop in oil prices should persist, helping to boost global economic activity by up to 0.7 percentage points next year, two senior IMF economists wrote in a blog on Monday.

Today the World Bank scaled back it’s forecast of global growth in 2015, from 3.4% to 3.0%. What might explain the lower forecast?

Consider two hypotheses:

1. Oil prices are falling because of supply improvement such as fracking, and a rebound in Libya after the recent revolution.

2. Oil prices are falling because of a global growth slowdown, perhaps due to tighter monetary policy.

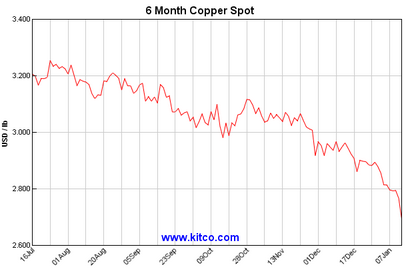

How could we tell which is right? One possibility would be to look at other commodities. Fracking would not be expected to boost the supply of other commodities, but a global slowdown would be expected to reduce demand for other commodities. Here’s copper, sometimes called “Dr. Copper” because it has a PhD in predicting movements in global growth:

Of course that’s not definitive, but other sensitive commodities are also falling in price. Thus I see the “lower demand” argument as being somewhat more plausible than the “greater supply” argument, at least for the past couple of months. But that’s not to say that the supply of oil (and perhaps copper) has not also increased, and indeed I still see little sign of a major economic slowdown. For instance, while equity markets are down today, their absolute levels are still rather high.

READER COMMENTS

Brent Buckner

Jan 14 2015 at 1:03pm

Not necessarily either/or – could be both:

http://econbrowser.com/archives/2015/01/demand-factors-in-the-collapse-of-oil-prices

Richard A.

Jan 14 2015 at 1:43pm

What you need to look at is the change in the quantity of oil being sold to help determine if the price fall is due to a decrease in demand or an increase in supply.

cthorm

Jan 14 2015 at 1:55pm

Scott –

If demand was the culprit, why aren’t we seeing lower equities prices? I believe commodities overall (excl Oil) are seeing a special case situation of falling demand. Commodities really exploded as an “asset class” about a decade ago, and accelerated in 2009. These “inflation protected returns” funds have done awful and they’ve seen huge outflows starting in 2011.

ThomasH

Jan 14 2015 at 2:03pm

The global outlook for 2015 might be less bright than was thought (leading the WB to revise its forecast) [we know that both the Fed and ECB are running too tight monetary policies] AND that lower oil prices leading to an increase in growth (compared to no decrease in those prices) of x%.

That’s the way I interpret statements about “A will have effect B.” It’s like the sequester; it may have reduced growth by 0.x% compared to no sequester [Or may not. I wish someone would have a look at that in a fully specified model] but growth over the period did not slow down because ceteris non paribus.

Don Geddis

Jan 14 2015 at 2:51pm

@ThomasH: No, it’s much worse than that. You’re merely imagining that there are multiple influences, and perhaps the low oil prices are still stimulating growth, but something else (e.g. tight money) is exerting pressure the other way, and even stronger. So the net effect is negative.

But you are still making the same “never reason from a price change” mistake. Namely, lower oil prices by themselves, don’t tell you whether the oil effect on growth is positive or negative. The whole point is: it matters why the price of oil declined. There are both supply and demand reasons that oil could drop in price, but they have opposite implications for future growth.

So the problem is not, as you supposed, that “something else” might also be going on. The problem is that it is already an error to conclude (without looking deeper) that lower prices on their own are a signal of higher growth. (E.g. compare with Richard A’s comment above, who gets it.)

Daublin

Jan 14 2015 at 3:37pm

The level of production seems relevant.

If prices go down, and production is still high, then it suggests that we are getting more efficient at producing oil.

Scott Sumner

Jan 14 2015 at 4:09pm

Everyone, I should have been clearer that in all probability multiple factors are involved. So I agree with many comments, including the need for quantity of oil data.

I guess I was speculating on the basis of a few data points (such as falling commodity prices in many sectors, and downgraded global growth forecasts.) Those point to lower demand, but I certainly agree that larger supply of oil (fracking, etc.) is part of the story.

What I objected to was people jumping to the conclusion that lower prices were good for growth, without carefully considering the reasons for the price decline.

Regarding equities, there is some evidence that the slowdown is mostly outside the US, which would help explain our markets. I suppose Eurozone and Japanese markets have been helped by expectations of monetary stimulus.

Pemakin

Jan 14 2015 at 6:43pm

Scott’s right that demand is a big issue here as other commodities and other variables suggest demand declines. However, the unique features of supply in the oil market really matter as there is an active cartel that has managed supply over the last 50 years. What has clearly happened is that growing non-OPEC capacity (largely North American) and a small decline in demand have undermined the delicate balance in the cartel has maintained. Think of it as really two supply curves, one managed by the cartel in the short run to expected demand and one that would exist without the cartel. We have shifted toward the latter.

The supply curve is likely to tighten (move to the left) as the cartel works out its differences. Remember the price elasticities and non-renewable nature of oil create enormous incentives for both responsible and irresponsible players to arrive at active or tacit agreement.

E. Harding

Jan 14 2015 at 8:01pm

The low oil prices are mostly due to stronger U.S. production.

http://www.advisorperspectives.com/commentaries/fpi_011415.php

Ray Lopez

Jan 15 2015 at 2:15am

A good mnemonic is ‘never reason from a price change’ but to be fair most of the time supply changes slowly, while demand is very fickle, so indeed most of the time it’s a correct inference to say a lower price is due to lack of demand, rather than increased supply.

ChrisA

Jan 15 2015 at 6:08am

I am with Scott. I think the reduction in oil prices is due to a slowdown in the rate of growth expected in the world. And I think other commodities are also falling for the same reason. And the reason is that China is now increasingly being seen as a “mature” economy. Its workforce is actually falling since 2012, there is still growth there, but it is normal growth not the hyper-catch up from communism growth. Markets are about expectations, not just about day to day supply demand. And the markets are seeing a slowdown in world growth due to China. A small change in view in growth rates is huge, when you compound it across many years. I said this at the same time as oil prices were rising (actually on Hamilton’s blog) when the peak oil theorists were rampant in the mid 2000’s. I pointed out that most other commodities were all reaching new highs. But was it really credible that we reached, say, peak Orange Juice at the same time as peak oil? It was not a popular view at the time, but I see Hamilton now is amazed that oil is back down to $50/bbl.

vikingvista

Jan 15 2015 at 12:04pm

Ray,

Wouldn’t you then expect the pundits to be pessimistic about falling oil prices?

Garrett

Jan 15 2015 at 9:36pm

I find it difficult to reason from the level of equity prices given the multitude of factors involved in valuation. To a first order you have three factors (D/[r-g], classic DDM), but to a second and third order you also have margins, payout/reinvestment ratios, the equity risk premium, and risk-free rates.

pszo

Jan 16 2015 at 4:58pm

Since June 19, when crude prices started heading south, oil is down 60% and industrial metals (S&P index) just 11%. So either a) oil supply is very inelastic compared to miners’ price sensitivity or b) price performance reflects specifics of the oil market (such as supply factors). In 2008, for example, both oil and metals moved down more or less in parallel, which indicates that since then something has changed in the oil market.

Comments are closed.