Over the years I’ve argued that economists are horribly confused about the concept of “income.” They use income for tax incidence discussions and also economic inequality, whereas on theoretical grounds consumption is clearly the appropriate variable. And yet until a few minutes ago I never realized just how confused we were (which I guess means I was equally confused).

I did a post over at MoneyIllusion on real wages, and commenter Foosion directed me to a Paul Krugman post on the topic. Krugman tries to show that real wages have done poorly, but is only able to do so by deflating the wage series by the CPI. I used the PCE, which is preferred by most experts, and found a significant rise in real wages since the 1990s. But it was this comment by Krugman that left me scratching my head:

My second chart shows real GDP per household — nominal GDP, deflated by the consumer price index, divided by the total number of households; and compares it with median household income, both expressed as indexes with 1979=100. We’ve had substantial income growth since then, but very little for the median household, because so much of it has gone to the top.

Now it’s a free country, and Krugman can define “real GDP” any way he likes. But the term ‘real GDP’ has a pretty well accepted meaning among economists, and it’s definitely not NGDP/CPI. Instead, real GDP is NGDP divided by the price index of the goods that make up NGDP, i.e. the GDP deflator.

At this point I realized that I was being too hard on Krugman. After all, GDP is just another term for gross national income. And economists have been using the CPI to deflate income data of all sorts for decades. But the fact that we’ve been doing it doesn’t make it any less insane. Let’s look at some basic definitions (sorry David).

GDP = C + I = C + S = GDI

So in a simple model with no trade or government, national income has two parts, consumer goods and investment goods. Obviously if we want to calculate the real value of consumption, we ought to use the price level of consumer goods (the CPI or the PCE). And if we want to calculate real income/output, we’d deflate using the price level of all goods, consumer and investment. And yet how often do you see economists calculate real income by using the CPI or the PCE? Indeed I made this mistake in my MoneyIllusion post, using the PCE. The correct deflator is the GDP deflator. (Yes, it gets more complicated with government and trade, but that doesn’t excuse this fundamental error.)

Perhaps economists are interested in the purchasing power of income under the assumption that all income was consumed. But in that case GDP would equal C, and investment would be zero. So the two price indices would be identical. As long as GDP does not equal C, it makes no sense to deflate income with the CPI or the PCE.

If you are still reluctant to give up on the notion that the “cost of living” should be measured in terms of consumption price indices, I think I know why you are confused. Yes, in a sense the CPI or PCE is the deflator that is appropriate for living standards comparisons, but that means our bigger mistake is that we are using income as a measure of economic wellbeing, whereas all our economic models tell us that consumption is the appropriate variable.

Unless I’m mistaken this is embarrassing. First the economics profession ignores the implications of their models by using income where consumption is appropriate. That’s already pretty bad. Then to make matters worse we don’t deflate income with the appropriate price index, the one for all of income, not just consumption. Instead we deflate income (i.e. C+I) with a consumption price index. We use the wrong indicator of well being, and then pick the price index that would be appropriate if we’d chosen the right indicator of well-being!

Does this matter? Not before 1970. But since then it matters a lot. Commenter E. Harding sent me a graph showing that since 1970 the CPI has risen far faster than the PCE, and even the PCE has risen more than the GDP deflator. This mistake explains much of the phony claim that “real income” has stagnated since the 1970s. (Although many articles also make other mistakes, ignoring fringe benefits like health insurance, or government transfers.)

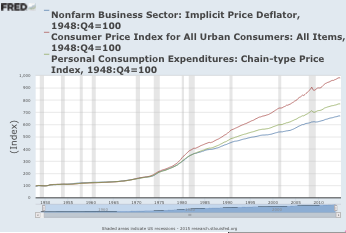

PS. Unfortunately I had to shrink this graph to fit the 400 pixel max at Econlog. The fast rising red line is the CPI, the green is the PCE and the blue is the GDP deflator.

Update: I misinterpreted the graph sent to me by E. Harding. The blue line was the price index for the business sector. In this new graph the GDP deflator is added, and is very slightly above the PCE. So the problem is less worrisome than I assumed.

READER COMMENTS

Zack

Mar 5 2015 at 12:01am

Wow, great post. I never even thought about this but it seems so obvious. Have economists really been looking at this the wrong way this whole time or is Prof. Sumner missing something? I’m really looking forward to hearing the replies to this one.

Kenneth Duda

Mar 5 2015 at 1:43am

Scott, this is totally amazing. Sometimes I think you’re the only economist on the planet who can think clearly about aggregates. Krugman is so damn smart yet you are totally right, deflating GDP by anything other than the GDP deflator is just divide-apples-by-oranges nonsense.

-Ken

Kenneth Duda

Menlo Park, CA

MGreen

Mar 5 2015 at 5:13am

So that’s absolutely right. Krugman of course makes another error by using median household. Since 1970, the characteristics of the median household has shifted radically — smaller, more minority, more female and less employed.

In 1970, the median household was a white, married couple with 2.2 kids and 1.3 incomes. Today it’s a single working mother.

E. Harding

Mar 5 2015 at 5:35am

No, blue is not GDP deflator, it’s the Nonfarm Business Sector deflator, which is used to deflate Nonfarm Business Sector output. If you add in the GDP deflator, over the long run, it looks very similar to the PCE index, and actually rises slightly above it:

http://research.stlouisfed.org/fred2/graph/?g=130I

foosion

Mar 5 2015 at 6:09am

MGreen – what’s your data source? Census data do not appear to support your statements. https://www.census.gov/hhes/families/data/households.html

Scott Sumner

Mar 5 2015 at 9:31am

Zack, I can’t speak for others, but it didn’t occur to me until recently. However check the update, it appears the PCE is pretty close to the GDP deflator. The CPI is still wrong, however.

Thanks Ken.

Thanks E. Harding, I added an update.

MGreen, Interesting, but I’m not quite sure what the term “median household” means, when there are many types of households, and no obvious ordinal ranking.

Foosion, Now that married households are in the minority, it’s certainly accurate to say that the median household is now an unmarried household (but maybe not single working mother.) It looks to me like household size has fallen from about 3.2 to 2.5, or slightly above that, which seems like a non-trivial decline. Obviously any data like real GDP would look better on a per person basis than a per household basis. Perhaps 25% better, in terms of growth since 1970?

W. Peden

Mar 5 2015 at 9:46am

Great post. I’ve long preferred GDP deflator-based real income and wage data, but on the grounds of methodological problems with constructing CPI indexes. Your post makes clear that, even if CPI indexes were unproblematic, calculating using the GDP deflator would be preferable.

AS

Mar 5 2015 at 9:58am

Income is a better measure of the household’s opportunity set and assuming the household is optimizing within their budget set, income (and wealth) will be a better proxy for that household’s lifetime utility than their current-period consumption. Households with high patience will have lower current-period consumption but higher lifetime utility.

Zeke

Mar 5 2015 at 10:33am

Krugman is dishonest. He surely is aware of the literature explaining why comparing households between two periods is an apples/oranges comparison. Yet he does it anyhow because it gets to the political point he wants. Very poor form.

I enjoyed your broader point Scott. Interesting to think about.

Scott Sumner

Mar 5 2015 at 12:02pm

Thanks W. Peden and Zeke.

AS, You said:

“Income is a better measure of the household’s opportunity set and assuming the household is optimizing within their budget set, income (and wealth) will be a better proxy for that household’s lifetime utility than their current-period consumption.”

I strongly disagree. First of all, wealth is the present value of future consumption (for you and those you give money to.) So wealth is more closely related to consumption than is income. Income does not measure a household’s opportunity set, as it combines wage and capital income, which is adding apples and oranges.

You are right that a patient person will have a higher lifetime consumption, and lifetime income, than a less patient person with the same lifetime wage income. But they do have the same opportunity set, and the same present value of lifetime consumption.

Andrew_FL

Mar 5 2015 at 12:53pm

The prices you want to use depend upon the things you want to buy. There really isn’t a single objectively correct price index with which to define the “true” “real” income, because different people want different things.

That being said, if your conclusion depends critically on a particular choice of price index, your conclusion can’t be true (ie objectively true). It depends upon a subjective choice.

Max

Mar 5 2015 at 1:55pm

Well, I have a question after reading about the GDP deflator on wiki. While I agree that Income is the important metric, I think that the GDP deflator might lack something.

“The GDP deflator (implicit price deflator for GDP) is a measure of the level of prices of all new, domestically produced, final goods and services in an economy.”

Are we really only consuming domestically produced goods? Wouldn’t that miss price levels of foreign imported final goods, which could be even more expensive or more inflationary in price?

Did I misunderstood the concept?

AS

Mar 5 2015 at 2:33pm

@Scott Sumner, I think we agree on the same. I was only claiming that current income may be better than current consumption for estimating lifetime utility because differences in savings rates will distort the useful of consumption data. Taking it a step further, by including wealth, I think the ideal measure would be Current Wealth + PV Future Income = PV Wealth. Data on future income doesn’t exist (obviously), but could be estimated from current income and age. So we only need 3 data points for each household: current wealth, current income, and age. That could yield a better measure than current income or current consumption alone.

Jeff

Mar 5 2015 at 2:46pm

This is a really important point, and very often not made, even in academic papers. I wrote a short paper (appeared in Economics Letters, 2012), applying different measures of inflation (CPI, PCE, and GDP deflator) to equity prices. Each measure of inflation affects the results of the model is quite meaningful ways. So for those of you writing papers, please identify precisely which measure(s) of inflation you are using!

Mark Bahner

Mar 5 2015 at 6:24pm

D-oh! I should read all comments before typing my own. I was about to post the very same idea: “I’d bet the size of households has declined significantly since the 1970s.”

But one additional thing is that every generation leaves the next generation more wealth than the original generation had. So even if income doesn’t go up, wealth is probably increasing.

Jose Romeu Robazzi

Mar 5 2015 at 7:21pm

Mr Sumner, all, great post, the focus on consumption does seem to be apropriate. But maybe we have to take a step back, even with PCE, when baskets change, we are not certain about the current basket is a perfect substitution to earlier baskets. There is no way to tell if the consumer is not “losing” something, when inflation based on the current basket (PCE) seems low. That is why I like NGDP rate targeting, preferrably with a low target, so as to make inflation zero. When prices area stable, change in content may still accur, but the damage potential is lower …

Andrew_FL

Mar 6 2015 at 1:12am

@Jose Romeu Robazzi-“so as to make inflation zero. When prices area stable, change in content may still accur, but the damage potential is lower”

But which price index do you want (long run) stable? That’s (one of) the fundamental problems with the zero inflation view.

I lean more toward’s the “Productivity Norm” which is a form of NGDP targeting but by the GDP deflator would probably be long run “deflationary.”

AS

Mar 6 2015 at 8:14am

Each generation also leaves behind something even more important than wealth: better technology. That’s very difficult to measure and not really reflected in any price index. How do you compare an iPhone from 2015 with a supercomputer from 1950? Or a vaccine that didn’t exist in 1940?

Mark V Anderson

Mar 6 2015 at 9:03pm

But I would like to understand why these various measures of inflation vary so much over a long period of time. I thought that most measures come together over the long term — thus wholesale prices or business service prices may go up or down at different times from the CPI, but ultimately they would become baked into retail prices.

What am I missing here? How can non-retail prices rise so much less than retail over the long term?

Todd

Mar 7 2015 at 1:57am

One thing I find common to posts on median income is they rarely take into account the fact that the median income nationallly will buy you a completely different lifestyle in, say, Mississippi, than it will in San Francisco.

Headline CPI, PCE and GDP deflators similarly do not account for differences at the regional level that quite literally render the macroview irrelevant.

Jose Romeu Robazzi

Mar 7 2015 at 3:25pm

Andrew_FL

I meant I don’t care about the various inflation indexes because I do think they can’t account for imperfect substitution and small changes in content. What I meant is that given that I don’t trust them, but I do like the NGDP targeting idea, maybe the target should be low, let´s say, instead of 6% NGDP (2% “inflation” + 4% RGPD), I would favor 4% NGDP (0% “inflation” + 4% RGDP).

Greg B

Mar 8 2015 at 9:23am

I have a problem with this post Scott.

The problem is the GDP deflator. It is a derived variable that is Nominal GDP divided by Real GDP and then multiplied by 100.

Problem is how does one derive Real GDP? That cannot be done using the GDP deflator since the deflator hasn’t been derived yet so it is in fact a basket of goods from some agreed upon base year, which is essentially CPI or something like it.

I think you are being a little disingenuous to present the GDP deflator as some “correct” metric. The GDP deflator has the same problems of CPI or any measure of inflation…. and of course I find the whole notion of inflation to be a monetarist fiction really.

There is no such thing as “Real” price. Just like there is no such thing as “natural” rate of interest.

Joe Cushing

Mar 8 2015 at 10:50am

There is a series of articles over at Cafe Hayek called “Cataloging Our Progress.” DON BOUDREAUX, looks directly at the ability to purchase consumer goods with a given number of hours of work. He does this by taking Sears catalogs from decades past and using wage data to calculate the number of hours a person would need to work to purchase a list of items in that time. Then he finds prices on often vastly improved items today and calculates the number of hours a person would have to work today to buy the item. Below is a link to a search of the blog that has several of these articles listed, along with some others that might just be noise, or maybe they mention the cataloging articles.

http://cafehayek.com/?s=cataloging+our+progress+

Comments are closed.