Here’s a question I’m confused about. I think I understand that Keynesians believe that fiscal stimulus is expansionary and fiscal austerity is contractionary. But what do they believe is the effect of fiscal stimulus if it’s called supply-side economics? Does that make its effects contractionary?

If not, then precisely what point is Paul Krugman trying to make with this post:

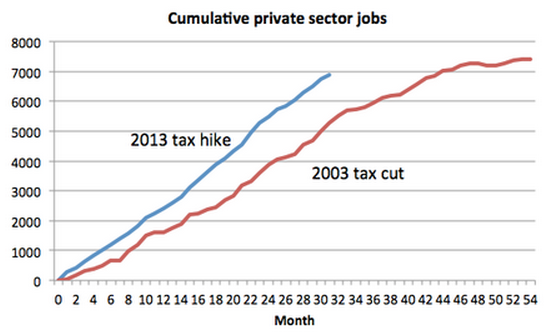

So the big tax cut of 2003 (and big spending increases) was less expansionary than the various types of fiscal austerity adopted in 2013 (big income and payroll taxes increases, plus spending cuts.) I guess I can buy that. But I’m not clear as to what sort of point Krugman is making here. Does this support the Keynesian model? If not, then what’s his point? Perhaps it suggests that Keynesianism and supply side economics are both wrong? Not likely, as Krugman is a Keynesian. Or maybe the point is that when Keynesianism is being evaluated it’s not a fair test, because other things weren’t equal, but when supply-side is being evaluated it is a fair test, because there is no need to hold other things equal when evaluating supply-side economics. Any anecdote will do just fine.

Undoubtedly I’m being unfair to Krugman, and I hope some of his readers will let me know the point of his new post.

PS. Apologies if the post comes off as sarcastic, but I’m actually raising an important point here, about how we evaluate evidence.

READER COMMENTS

baconbacon

Sep 10 2015 at 12:57pm

Its pretty obvious, isn’t it?

Total Krugman blog hits since 2010 have increased every single year.

UE rate since 2010 has decreased every year.

Therefore Krugman blog hits decrease UE.

Partisan attacks on republicans increase blog hits.

Its so simple that even a monetarist could understand it.

TallDave

Sep 10 2015 at 1:01pm

Obviously Krugman is a statist whenever the two diverge. “Anything that increases government revenues or spending is good” is not a Keynesian argument.

TallDave

Sep 10 2015 at 1:10pm

Notably, this is why “austerity” became the dysphemism for plans to achieve solvency — leftists could hardly inveigh against tax hikes on their own, but package them with spending cuts…

Steve Fritzinger

Sep 10 2015 at 1:18pm

From the graph, it looks like Krugman is comparing absolute number of jobs, not jobs per 100,000 people.

There are 30 million more people in the US today than there were in 2003.

I don’t think that graph is saying what Krugman wants it to say.

Justin D

Sep 10 2015 at 1:49pm

My guess is that Krugman would argue the following with respect to the claim that his chart undermines the Keynesian model:

1) Taxes have relatively low fiscal multipliers.

2) The underlying state of the economy matters – the underlying momentum of the labor market in 2013 was stronger than in 2003.

He’s making the point that we shouldn’t expect big economic gains from tax cuts, thus undermining Jeb’s tax plan which assumes that lost revenue will be made up by the beneficial impact on the economy. He can grant that taxes have an effect on job creation but it’s so slight that it is difficult to see empirically.

Regardless of what one thinks about the Keynesian model, I think Krugman’s view on tax cuts presented in his blog post is generally correct: the impact on the economy of modest tax cuts is not going to generate large dynamic effects, and there will be very little offsetting tax revenue from increased economic growth.

Capt. J Parker

Sep 10 2015 at 1:52pm

I think Krugman’s point is supply side effects from tax cuts are never as big as supply siders claim. For sure he believes Jebs tax plan has no hope of boosting real GDP growth to 4%. Krugman linked to this old James Tobin paper a few posts back. Tobin talks about supply side effects starting on Pg 36 and moves in for the kill on page 40 – Tobin:

Tobin goes on to back up this assertion with a simple model in the footnotes.

[Comment edited with commenter’s permission.–Econlib Ed.]

foosion

Sep 10 2015 at 2:04pm

Krugman is arguing against the Republican supply side claims that tax increases are job killers and tax cuts are magic. That’s the main point and he seems to have made it effectively.

Beyond that, when evaluating fiscal programs the details matter, something beyond the scope of the post you link. Things such as fiscal multipliers, what happens on the spending side, who gets the cut or increase (e.g., are they likely to spend or save), etc. are necessary for the analysis.

Daublin

Sep 10 2015 at 2:12pm

I applaud your patience and effort, in this post and in many others, but like some of the other commenters, it’s hard for me to be charitable.

Republican bashing has infected people in all manner of positions these days. It’s taken over Paul Krugman’s thinking and writing, and it’s taken over Neil deGrasse Tyson’s. It’s even taken over actual defense of substantive issues that are supposed to be important to the parties, such as women’s rights in Iraq. The government is 25% female now, which I would have thought to be a huge win for women’s status in the world. It’s being played down by women’s groups, though, because it’s a positive change that was caused by George W. Bush.

I find it depressing at a deep level, and it makes me want to not take part in intellectual discourse on this planet any more.

What I really don’t understand is why it’s so tempting to become troops for the Democrats. I understand why a failed thinker might turn to partison hackery as a way to get some blog hits. But why people like Paul Krugman? If he wanted to, he could make a big impact on the strongest economic thinkers of our times. Instead, he is alienating them, and for what? What is he really going to get out of being a loyal trooper for the Democrats?

Capt. J Parker

Sep 10 2015 at 2:17pm

Justin D, You beat me to the punch on what’s going on in Krugman’s head. But, about your last paragraph: before you dismiss the stimulative effects of tax reform you might want to read this from a guy who went to the same school as Krugman.

[Comment edited with commenter’s permission.–Econlib Ed.]

Andrew

Sep 10 2015 at 2:38pm

Mr. Sumner, you really should read thru the comments attached to Mr. Krugman’s posts if you are confused about what point he is trying to make.

It took me 30 seconds to find this one…

Mr. Krugman’s post has nothing to do with economics, Keynesian or otherwise.

baconbacon

Sep 10 2015 at 2:58pm

@Andrew-

Only that argument doesn’t hold up, specifically

because Krugman doesn’t mention that the situations are different or explore the counterfactual (what growth “would” have been). What Krugman does here is give the LEAST amount of information on the situation- he strips out the changes in total population (which is incredibly easy to adjust for as would be lfpr or working age population) and ignores the base UE rate etc etc etc.

foosion

Sep 10 2015 at 3:33pm

@baconbacon:

The GOP made specific predictions about the results of tax and regulatory policy. They did not condition their predictions on base UE, etc., etc., etc. Those predictions turned out to be wrong.

DD

Sep 10 2015 at 3:34pm

Krugman’s specific chart and post are absolutely terrible, but the overall argument that he implies is fairly sound. Republican forecasters treat tax cuts as stimulatory magic (hence economic growth offsetting decrease in revenues); the evidence for this is extremely, extremely weak (if it even exists). I would guess this is a nod to Jeb Bush’s recent tax proposal.

Like I said: not a great post (to put it mildly), but the implied message is worth discussing.

James Alexander

Sep 10 2015 at 3:35pm

OT

Apparently, if you model a monetary policy shock it has bad outcomes. Genius!

http://blogs.ft.com/gavyndavies/2015/09/10/what-caused-the-equity-crash/

E. Harding

Sep 10 2015 at 4:28pm

“Undoubtedly I’m being unfair to Krugman, and I hope some of his readers will let me know the point of his new post.”

-I don’t see how you’re being unfair here, at all.

adam

Sep 10 2015 at 5:33pm

Andrew,

Krugman was arguing in Dec. 2012 that raising taxes and cutting spending was going to hurt job growth, so while the chart doesn’t support supply-siders predictions about the 2003 tax cuts, it also undermines his own predictions about the 2013 tax hikes.

Scott Sumner

Sep 10 2015 at 6:13pm

Justin, I am not sure if that’s the argument Krugman would make, but I hope you can see that it’s a weak argument. If there are special factors that prevented the Keynesian model from working during this period, like the momentum you mention in the labor market, then that would equally well apply to any inferences about the supply-side model. Either there is a ceteris paribus problem, or there isn’t. You can’t say it’s a problem only when Keynesian model tests seem to fail.

As for taxes having a smaller multiplier, there were also big spending increases around 2003-04, and big spending cuts around 2013-14.

Captain, I certainly don’t think Jeb Bush’s plan would lead to 4% growth, but on the other hand it would have vastly bigger supply-side effects than the 2003 tax cut, which was very poorly designed.

Krugman’s post doesn’t provide a shred of evidence that I should be more skeptical of supply side economics than I am of Keynesian economics. Not a shred. If that graph is to be taken seriously, then both models are bogus. (I don’t take the graph seriously. It doesn’t test anything.)

Foosion, You said:

“Krugman is arguing against the Republican supply side claims that tax increases are job killers and tax cuts are magic. That’s the main point and he seems to have made it effectively.”

I’d respond:

Krugman is arguing against the Democratic Keynesian claims that austerity is a job killer and fiscal stimulus is magic. That’s the main point and he seems to have made it effectively.

See how terms like “magic” suddenly have a different connotation when they are being used against you?

Andrew, Is Krugman focusing “specifically” on the prediction that he himself made in early 2013? That austerity would slow the economy?

Everyone, I think a lot of you are missing the point. This post is not about supply side economics, or about whether his graph is a good test of supply side economics. It’s about whether Krugman uses a different procedure to test his own Keynesian theories than he uses to test supply side economics. I really expected someone to be able to defend Krugman on that score. I’m surprised that no one is even offering a defense of him on that point.

I would add that I’m surprised that people think supply siders are somehow more simplistic than Keynesians in their predictions. That Keynesians were not making grand claims that if we do “austerity” horrible things will happen, without taking into account all the complicating factors that people here (rightly) think are important and necessary to take into account. Like monetary offset.

Supply side economics has lots of sophisticated researchers doing careful work, (like Martin Feldstein), and lots of pundits shooting their mouth off in the press. Keynesian economics, on the other hand, has lots of sophisticated researchers doing careful research, and lots of pundits shooting their mouth off in the press. So what’s the difference?

bill

Sep 10 2015 at 6:59pm

I love this post. I would like to comment on this:

—

Foosion, You said: “Krugman is arguing against the Republican supply side claims that tax increases are job killers and tax cuts are magic. That’s the main point and he seems to have made it effectively.”

I’d respond: Krugman is arguing against the Democratic Keynesian claims that austerity is a job killer and fiscal stimulus is magic. That’s the main point and he seems to have made it effectively.

—

I think Krugman would agree with Foosion. And so would I. I know Krugman would disagree with second statement. I think he was in such a rush to make the point as Foosion interpreted it, that PK completely overlooked the obvious connection to this second statement. Yet the second statement is glaringly true too.

bill

Sep 10 2015 at 7:21pm

Regarding multipliers, I recall that Keynesians universally saw the two point Social Security tax increase as particularly deadly because it was two points on the first $115,000 of wages or so. Of course, they were wrong. The deficit fell five hundred billion dollars (say that with a Dr. Evil voice) and NGDP kept right on growing. And since we were at the ZLB, this is all totally inexplicable [sarcasm]

andy weintraub

Sep 10 2015 at 8:42pm

I remember Milton Friedman saying that the best real measure of taxes is government expenditures, as opposed to tax revenue.

Perhaps the austerity of 2013 produced a reduction in the rate of growth of government expenditures while the tax rate reductions of 2003 were actually associated with an increase in government expenditures.

meets

Sep 10 2015 at 9:12pm

He’s knocking down a strawman.

Nothing more.

Many of his posts have the quality of an angry commenter than of a professional economist.

Jose Romeu Robazzi

Sep 10 2015 at 11:26pm

I think that Krugman is so eager to go against Republicans in every single subject that he does not even care anymore about consistency with his own previous economic views. He is probably just trying to get a data evidence that increasing taxes don’t destroy jobs, because some Republican said otherwise …

ThomasH

Sep 10 2015 at 11:47pm

Not quite. If the economy is already at full employment and monetary authorities are trying to reign in the economy fiscal policy cannot be expansionary. That’s when Keynesians call for contractionary fiscal policies reducing investments in activities whose future benefits when discounted at the borrowing rate are less than zero in order to reduce deficits

And “austerity” (negative departures from the NPV rule) during recessions is thought to be contractionary because they assume that monetary authorities will not provide more stimulus to offset the fiscal drag. (If it could do more, why wasn’t it doing so already?) The latter assumption may of course be incorrect in some cases, though it has been a pretty good assumption in the US and Europe since 2008.

Greg G

Sep 11 2015 at 7:41am

I had the same reaction as Thomas. Where did Keynes say that fiscal stimulus at full employment was expansionary? I read him as saying it is merely inflationary and a bad idea.

No doubt it will be hard to get people to agree on what “full employment” means but I think it’s clear that whether or not Keynes saw deficits as expansionary was entirely dependent on where you where in the business cycle.

Mark Cancellieri

Sep 11 2015 at 9:52am

[Comment removed. Please consult our comment policies and check your email for explanation.–Econlib Ed.]

J Mann

Sep 11 2015 at 10:20am

Krugman’s post seems dishonest. Isn’t he on record that 2013 performance should have been disasterous, but for the fortuitous intervention of “other stuff?”

If he’s adjusted these graphs to correct for “other stuff,” he should spell that out.

Seriously, the Krugman/DeLong response is typically to sigh a lot and point out some unstated assumptions that any reader is expected to understand if they want to read Krugman’s writing at any level deeper that “Republicans bad!”. In this case, I would bet Krugman would say that since he believes that multiplier is always lower for tax changes than for fiscal changes, he doesn’t consider tax austerity to be comparable to fiscal austerity, not tax stimulus to be comparable to fiscal stimulus.

I think the “other stuff” might still give him s problem, though. If “other stuff” lifted the economy and prevented the cataclysm Krugman was predicting, then how is 2013 a good comparison for anything?

Hazel Meade

Sep 11 2015 at 10:25am

I have a suggestion.

Instead of the Fed raising interest rates, maybe the government should cut spending.

TallDave

Sep 11 2015 at 10:49am

ThomasH/Greg — As has been pointed out before, NPV is a measure of cash flows. Government spending virtually never has (or even intends) positive NPV. And changes in real borrowing costs don’t have much effect on the value proposition of a new road or bridge or welfare program, and to the extent it does matter, the best value proposition is going to be spend money within revenues, where borrowing costs are zero.

The classic statist/Keynesian dodge is on display again here — Krugman certainly did not argue the economy was doing so well in 2001-3 that the tax cuts were unnecessary, he argued (and still does) that tax cuts are ineffective. Again, that’s statism, not a Keynesian argument.

Rich

Sep 11 2015 at 10:53am

I don’t think the two eras are comparable at all. To me, the Great Recession was due to extremely oversold assets that never recovered at a normal pace due to excess regulation and the imposition of excess labor costs, much in the form of the ACA. Employment lagged in the market place until 2012. Companies held cash until this time and did not hire workers because business risk was too high. Once the costs of the new era settled business was able to plan modest expansion. To me, the first term of the Obama administration restricted employment from taking place at a normal rate. Now that employment is returning to normal, some deferred hiring is taking place within the normal hiring we are seeing. Of course, economists often overuse regression techniques to associate illogical independent and dependent variables. I would not associate the tax hike of 2013 with the current hiring rate and then compare it to 2003 without adjusting for context.

Scott Sumner

Sep 11 2015 at 11:07am

Andy, That’s exactly what happened.

Thomas and Greg, I agree about the full employment qualifier, which of course weakens Krugman’s claim, as we were closer to full employment in 2003 than 2013.

Mark, I don’t like to see ad hominem attacks–stick to the issues.

Justin D

Sep 11 2015 at 2:53pm

Capt. J Parker,

I understand some studies have found large effects for tax cuts, but I just can’t accept it. Take the Romer paper. It doesn’t seem likely at all that a $1 tax cut raises GDP anything like $3. The experience of the US in particular doesn’t seem to square with such a strong relationship.

For example, in the 5 years to 2002Q4, GDP grew 2.95%/yr. In the 5 years to 2007Q4, GDP grew 2.95%/yr, despite the fact that the first 5 years contained a recession/weak recovery and the second had a more favorable tax environment. GDP growth in the 5 years to 1996Q4 was 3.56%/yr, despite the Bush and Clinton tax hikes.

I can believe that tax cuts of the type which typically occur in the US changes real GDP growth marginally: perhaps +0.3%/yr or something like that – but not anything substantially more.

Scott,

I can see that’s a weak argument, I agree it is difficult for Krugman to appeal to that chart to show how tax policy doesn’t have large macroeconomic effects without also undermining the Keynesian model given the overall fiscal situation in each case. I do think he’d rely heavily on the fact that not all else is equal. He doesn’t really have anything else available as far as I can tell.

Capt. J Parker

Sep 11 2015 at 6:50pm

Justin,

I think we both believe there are no magic bullets to achieving more real growth. But, right now we have 2% real growth on average since the recovery. 2.3% real growth would be a big improvement.

John B

Sep 11 2015 at 9:33pm

It’s ridiculous to me that Mises’s lessons about economic methodology are so underappreciated. Everywhere you look in economics you see examples like the one Scott highlighted but no seems to draw the correct and logical conclusion that economic theory cannot be be either derived or supported by empirical data because of the high causation density. Good economic theories derive from sound reasoning. It doesn’t make any more sense to try prove supply and demand through observation than to prove the Pythagorean theorem by conducting “natural experiments” measuring right triangles. Despite this we know that both are true because they are logical. Furthermore, they are both useful and not merely tautologies. Just to make another point, no one in economics has ever been convinced by a graph like this but nearly everyone arrived at their current views on economics because they bought into a chain of reasoning.

ThomasH

Sep 11 2015 at 9:56pm

@Tall Dave:

When doing an economic analysis of an investment one should consider both cash and non-cash costs and cash and non-cash benefits. I fail to see why you think the government borrowing rate is not relevant to the relative value of costs and benefits at different times.

Nor do I understand your (very common) presumption that Keynesian analysis it “statist.” If government invests in activities that have positive NPVs the economy expands by more than the borrowing so government becomes a smaller part of GDP.

I will grant that I am remiss in always talking only about financing activities that that will have future benefits as if they are always government investments. In principle, the same logic applies to private activities financed by subsidies or tax cuts. Tax cuts such as reducing the wage tax or a higher EITC could have the same effect of creating future benefits greater than the discounted presents costs as well chosen public investments. Since the Bush tax cuts were not of that nature (transferred income to high income people and were permanent, not temporary), it’s not surprising that a Keynesian would not be very enthusiastic about them.

Keynesian prescriptions are statest only relative to “austerity,” the idea that expenditures should be reduced (paying no attention to their NPV) during a recession. And one suspects that people who hold that opinion probably think that expenditures should be reduced (paying no attention to their NPV) during full employment, too.

Scott Sumner

Sep 12 2015 at 9:50am

Captain, Under most circumstances neither supply side nor demand side effects of tax changes (or spending changes) will have a dramatic impact on GDP.

There are exceptions. WWII spending had big demand side effects on GDP, and Deng’s policy of allowing farmers to keep a share of their output (which was essentially a tax cut) had massive supply-side effects on GDP in China.

It’s a myth propagated by the left that most supply side economists predicted that tax cuts would boost revenue. That was only expected in extreme cases.

John, Unfortunately neither approach is adequate–you need both.

TallDave

Sep 12 2015 at 11:40pm

ThomasH —

Consumption is utility, and not an input to NPV. When you buy and eat a hamburger, the NPV of the purchase is zero, even if you’re really hungry or borrowing costs are low. Government spending is generally consumption, not investment, and the borrowing rate is a small component given that most expenditures have zero borrowing cost.

Again, Keynesian-ism and statism are different things, and “Keynesians” like Krugman are clearly statists whenever the two diverge. You even managed to repeat his anti-Keynesian fallacy of equating only expenditures with the stance of fiscal policy.

David R. Henderson

Sep 13 2015 at 12:24am

@TallDave,

When you buy and eat a hamburger, the NPV of the purchase is zero, even if you’re really hungry or borrowing costs are low.

The NPV of the purchase is positive or you wouldn’t buy it. Once you’ve eaten it, of course, it’s zero.

hamilton

Sep 13 2015 at 9:00am

The point of the post is that the supply side claim that increasing the tax rate will lead to a collapse in employment, while cutting taxes will lead to measurable job growth, in general, is wrong.

These two data points can’t be used to say anything about small impacts in either direction. But, remember when Milton Friedman predicted the Clinton tax hike would lead to a recession? Showing that this didn’t happen is possible with essentially one observation.

For Keynesians, the Bush tax cuts shouldn’t necessarily have been expansionary — see Scott Sumner’s post. The Fed moves last. Keynes prescription was to run surpluses when the economy is doing well, not structural budget deficits…

That leaves 2013. I don’t see this as strong evidence against Keynesian economics, as it is one data point. Other things aren’t equal so there isn’t a good natural experiment. And the theoretical impact of raising taxes on the rich, who aren’t exactly hand-to-mouth consumers, is that you should have a small multiplier. Thus, call the expected hit — 1% of GDP? How do you know what would have happened absent the tax increase?

TallDave

Sep 14 2015 at 3:34am

David R. Henderson — NPV takes into account expected future states so the NPV of a hamburger purchase must be zero, unless you expected to sell it instead of eating it (consuming its value).

Investment has NPV, consumption does not.

TallDave

Sep 14 2015 at 4:07am

Better example: the NPV of a personal vehicle purchase is its discounted future trade-in value, or zero if you never expect to sell it. (Well, plus any discounted future cash flows you expect from Ubering and Lyfting.)

Utility =/= value. You cannot include the utility of being able to drive the vehicle in your NPV calculation (though of course you do consider it in the purchase decision, because you want to maximize utility when you trade value for utility).

Bob Murphy

Sep 19 2015 at 2:28am

Not sure if you’re still checking this post, Scott, but this was great. A few of us took a whack at this Krugman post but you pointed out the problem with it better than anyone I’ve seen yet.

Comments are closed.