Market forecasts are often wrong. But they remain the least bad way we have of predicting the future. In the past, we’ve paid a heavy price when the Fed ignored market forecasts. In September 2008, the TIPS markets predicted very low inflation while the Fed predicted very high inflation. The Fed refused to ease money policy and we paid a heavy price when it turned out the markets were correct.

Once again the TIPS markets are predicting the Fed will fall short of its inflation target. Fortunately, this time the macroeconomic consequences of a mistake are likely to be smaller, as the economy has adjusted to 1.5% trend inflation. But it does slightly increase the risk of recession, and long term there may be a price to pay if the Fed loses credibility, or suddenly lurches toward 2% inflation at the top of the business cycle—which is the worst possible time.

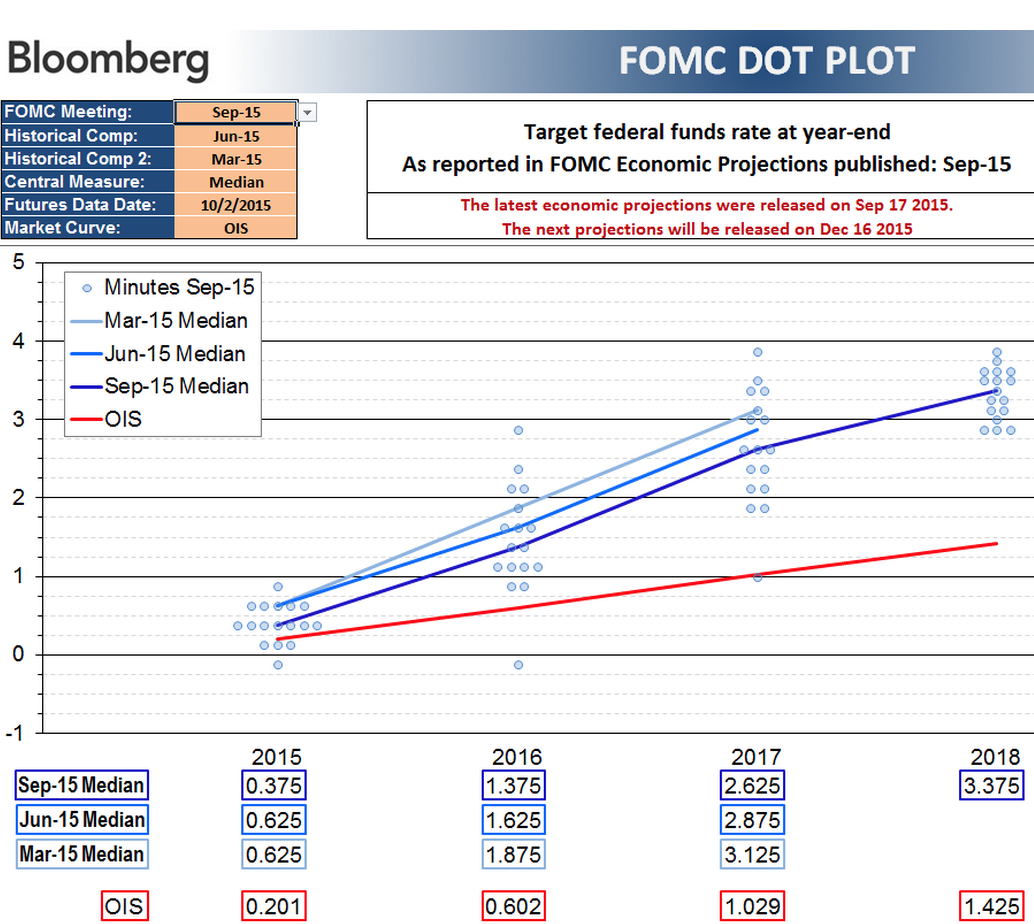

Some argue that TIPS spreads are not a good indicator of inflation expectations, as TIPS are less liquid than conventional T-bonds. However there is a completely unrelated market that is sending us the same signal—fed funds futures. As the following graph shows, the market expects the fed funds rate (red line) to rise at a slower rate than the Fed estimates (blue lines.)

Notice that the market forecast for the end of 2017 is only about 1%—which is equal to the forecast of Minnesota Fed President Kocherlakota, who is viewed as being a bit eccentric by other Fed officials. That’s a warning that anyone who tells the truth about monetary policy is likely to be viewed as a bit crazy. As someone who has claimed for years that a tight money policy in 2008 caused the Great Recession, I sympathize with Mr. Kocherlakota.

As always, interest rates are tricky to interpret, as they are both indicators of policy and (endogenous) indicators of the state of the economy. As long as the Fed has at least some credibility, some intention to keep inflation in the ballpark of 2%, then long run interest rates are endogenous—they reflect the market expectation of the condition of the economy. On the other hand the Fed has some discretion about what to do this December.

If I’m right then I would interpret these market forecasts as follows:

1. The near term forecast (end of 2015) implies the market believes Fed policy will be too tight.

2. The longer term forecast (end of 2017-18) implies the market thinks NGDP will grow by much less than the Fed thinks NGDP will increase. As a result of that slow NGDP growth, the Fed will be forced to keep rates lower than it currently expects in order to prevent inflation from deviating dramatically from the 2% target. (In other words, to keep inflation in the 1% to 2% range, rather than falling into negative territory.)

As I said at the opening, markets are sometimes wrong. But if I were a betting man I’d bet on the markets, not the Fed. This is one more reason why we need policy guided by NGDP futures markets, not a committee of 12.

READER COMMENTS

James

Oct 3 2015 at 4:03pm

“This is one more reason why we need policy guided by NGDP futures markets, not a committee of 12.”

What we have now is policy guided by the overnight lending market with a committee picking the target price in that market. Exactly how much better would it be to have the committee focus on the NGP market?

I’m asking for point estimates and a method to reproduce your results. Absent that, there is no reason to believe NGDP targeting would make enough of a difference to care about.

ThomasH

Oct 3 2015 at 5:23pm

The problem was in trying to predict inflation rather than keeping it on track. Yes, the Fed could have reduced rates sooner and started QE sooner, but the larger problems were in not letting the market know that QE (or what ever it took) would be used in any amount necessary to keep inflation on track or to return the price level to its target trend. If the Fed acted consistent with it’s own target, its failure to predict inflation would not be so serious.

Scott Sumner

Oct 3 2015 at 8:49pm

James, This paper explains my NGDP futures proposal:

http://mercatus.org/publication/market-driven-nominal-gdp-targeting-regime

Thomas, Good point. In fact both problems were important—the failure to predict, and the failure to target the forecast, that is, the failure to set policy at a level expected to produce on target results.

James

Oct 3 2015 at 10:30pm

Scott,

I began my question with “Exactly how much…” and then told you I was asking for point estimates, not an explanation. I think anyone could read my comment and see that I was asking for numbers. You gave none.

Since I didn’t find it in the paper you referred me to, perhaps you can clarify here: Under your proposal, would the target be set by a committee of economists? In case it’s not clear, I am asking for a “yes” or a “no.”

ThomasH

Oct 4 2015 at 6:01am

I am more focused on the long, ongoing error of insufficient stimulus 2009-2015 produced by the failure to target the “target,” than the failure to predict. Prediction in the current political economy — pressure for tightening and none for “inflation” — will, I think give prediction a downward bias. There will always be plenty of predictions of higher inflation and this gives the Fed cover to ruminate about tightening when the PL is still below trend.

Also I think there is an interesting division in outlooks on future inflation fighting if and when THAT becomes necessary. One side thinks the Fed can and will easily raise interest rates (I’m sticking to the current way of thinking about “policy”), while the other thinks the Fed will be reluctant to tighten either out of fear of a sharp recessions or because it is beholden to financial interests that do not like big, unanticipated changes in interest rates. The first leads to less concern (no concern when the price level is below target) with inflation when it is below target. The second leads to an inflation rate ceiling constraint.

Still another three strands of opposition to allowing catch-up inflation (that constrains PL targeting and would constrain NGDP targeting) are 1) instrument inertia (reluctance to use anything but changes in ST interest rates) 2) central bank balance sheet concerns and 3) asset bubble/financial instability fears. These have to be addressed even if they are just rationalizations of financial interests self-interested or mistaken desire for higher interest rates.

Nathan W

Oct 4 2015 at 7:21am

“or suddenly lurches toward 2% inflation at the top of the business cycle—which is the worst possible time”

Why is 2% inflation worst at the top of the business cycle? I’m guessing something about price signals and relation to hiring and investment, but I’m really not sure.

James – “would the target be set by a committee of economists” – no, he said a futures market NOT a committee of 12 (last line)

James Hanley

Oct 4 2015 at 9:58am

Can the debate about the best indicator be settled by an analysis of historical data?

Scott Sumner

Oct 4 2015 at 3:55pm

James, Yes.

Thomas, I don’t believe that balance sheet constraints would limit NGDPLT. Indeed level targeting would allow the Fed to hit its target with a far smaller balance sheet. So that’s actually an argument in favor of NGDPLT. The same is true of low interest rates. Under NGDPLT, interest rates would be higher than today.

Nathan, Procyclical inflation violates the Fed’s dual mandate, and makes unemployment more volatile. The Fed’s dual mandate calls for countercyclical inflation, low inflation during booms and higher inflation during recessions.

Lots of people get confused on this point. To see why, start with a single mandate, 2% inflation. Now add an employment mandate. You’d want to be a bit more expansionary when unemployment is high, and vice versa. That pushes inflation in a countercyclical direction.

James Hanley, There’s not a long enough time series for TIPS spreads to really resolve the issue.

ThomasH

Oct 5 2015 at 7:32am

Scott,

I was trying to consider an intermediate state of a ngdp targeting but not the commitment to using purchases and sales of the ngdp futures contract as an instrument and in situations in which achieving the target requires that realized inflation be above the recent historic rates.

Another way of looking at things is what would the Fed have done 2007-2015 — what would it have bought and sold — if it had adopted a 4% ngdp target in Sept 2007? And would there have been political opposition to doing so?

James Hanley

Oct 5 2015 at 7:34am

Thank you, Scott.

Scott Sumner

Oct 5 2015 at 2:55pm

Thomas, With a 4% NGDP target, level targeting, the Fed could have done far less QE, and achieved better results (faster NGDP growth.) The policy would have been more effective and more popular.

Comments are closed.