It was the best of times; it was the second best of times. It’s natural to want to compare Hong Kong and Singapore. They are among the very richest non-oil producers in the world, at least among economies having more than 5 million people. They are both quite small, and mostly ethnic Chinese. They score #1 (Hong Kong) and #2 (Singapore) on both of the major economic freedom indices. Neither is completely laissez-faire, but then no country in the entire world is even close to being laissez-faire. For instance, in Hong Kong the government dominates the all important real estate industry.

But there is one difference that’s worth thinking about—monetary policy. Hong Kong has had a currency board since 1983, and Singapore has a monetary regime that uses exchange rates (rather than interest rates or the money supply) as the monetary instrument. The Singapore approach could be viewed as somewhat market monetarist, as we oppose using the interest rate because of the zero bound problem.

If Singapore does have a more effective monetary regime than Hong Kong, then I’d expect less cyclical instability due to demand shocks, and hence less of a “Phillips Curve” type relationship. I already knew that Hong Kong exhibited a highly significant Phillips curve, because it meets all three conditions necessary for the Phillips curve model to work:

1. Stable inflation expectations and an unstable actual inflation rate.

2. Demand shocks more important than supply shocks.

3. A stable natural rate of unemployment.

The first and second point reflect the fact that pegging the Hong Kong dollar to the US dollar meant stable expectations after 1985, because America had low and stable inflation expectations. However, Hong Kong had more unstable actual inflation than the US, because it was hit by major shocks, such as the East Asian crisis of 1997-98. And unlike Western European countries, it has a stable natural rate of unemployment, because the government is not heavily involved in regulating the labor markets.

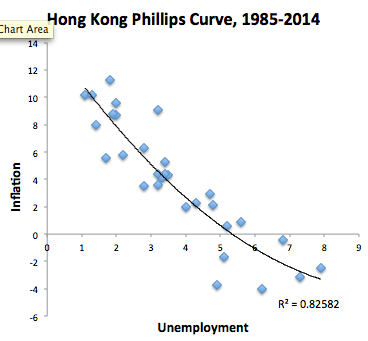

Here is the (very impressive) Hong Kong Phillips curve:

Notice the R2 of 0.826. They don’t make Phillips curves like that anymore! (I believe the US would show almost no correlation over that period.) But a good Phillips curve is a bad monetary policy. The central bank is creating procyclical inflation, and hence making the business cycle worse. A central bank with a dual mandate would create countercyclical inflation. Most don’t achieve that, but some come close.

Also note that inflation is extremely volatile. I’ll give Hong Kong credit for flexible labor markets. If the US or Europe had that sort of inflation instability, our unemployment rate would be far more unstable, with horrific levels of unemployment during years of 4% deflation. But can’t we do even better? Yes, we can.

Here’s Singapore’s (unimpressive) Phillips curve:

The R2 is now only 0.227. Also notice that Singapore avoids the extreme levels of inflation and deflation experienced by Hong Kong, although it was subject to the same sort of shocks. For instance, Singapore could devalue in 1997-98, and thus avoid the worst of the East Asia crisis. As a result, Singapore also had less unemployment rate instability than Hong Kong.

Conclusion: Singapore has a very good monetary regime. The use of exchange rates as a policy instrument avoids the zero bound problem, and hence fiscal stimulus is not needed. (I’m not sure if it was used.) By adjusting the exchange rate to minimize demand shocks, Singapore has much less cyclical instability than Hong Kong. The Hong Kong government argues that the dollar peg provides security for investors, helping Hong Kong maintain its position as a financial center. But Singapore is also a very successful financial center. Hong Kong should adopt Singapore’s monetary regime.

PS. Think of Hong Kong as like a superbly conditioned athlete that lives in a flimsy house. During storms he is bombarded with branches, tossed by the wind. He survives, but only due to the fact that he’s in much better shape than his friend Argentina, who was severely injured by the hurricane of 1998-2001. Singapore’s also in excellent shape, but not quite as good as Hong Kong. But Singapore lives in a much sturdier house, and received only modest damage in the storm.

After 2002, Argentina crawled into a much safer house, but then adopted some really bad habits, and his health eventually deteriorated as he lay on the sofa all day eating high cholesterol steaks.

PS. Travel today—replies to comments may be delayed.

READER COMMENTS

Zooko

Apr 17 2016 at 9:15am

I read the whole thing with interest but with limited comprehension. Isn’t pegging to the USD just the extremum of “using exchange rates as a policy instrument”?

I have only one comment: eating high-cholesterol steaks is good for your health.

(You might enjoy this excellent recent article on the probable coming upheaval in food politics: http://www.theguardian.com/society/2016/apr/07/the-sugar-conspiracy-robert-lustig-john-yudkin .)

Daniel

Apr 17 2016 at 9:35am

This lacks the contextual understanding that Singapore is like .75 a normal country and Hong Kong is .25 a normal country.

Their macroeconomic policies reflect this. The situation of investment in Singapore is radically different than that of Hong Kong. Hong Kong knows what their priorities are, and knows what they are doing. Ditto to Singapore – they’re just different.

Scott Sumner

Apr 17 2016 at 11:12am

Daniel, Without any specifics, I can’t comment.

I will say that if you look around the world over the past decade, it’s a pretty good bet that central bankers do not “know what they are doing”.

Benoit Essiambre

Apr 17 2016 at 12:48pm

Excellent. I’m no economist but it seems to me that this post could be the basis for a blueprint for central bankers.

If they go long periods without making the Philips curve strait or sloping a bit upwards like a dual mandate implies, they should face serious questions.

ThaomasH

Apr 17 2016 at 2:05pm

I certainly agree that Singapore has a better monetary policy than Hong Kong, but seems like Hong Kong’s mistake is to limit itself to using only ST interest rates as a policy, like the US Fed. Whereas Singapore uses a wider array of instruments (including purchases and sales of foreign exchange denominate assets?) to target something like NGDP. It seems to me the analysis would be clearer if it dealt separately with what outcome is targeted, and what instruments are used (including any limits on the use of those instruments)

Scott Sumner

Apr 17 2016 at 10:49pm

Zooko, The peg prevents the central bank from trying to stabilize demand.

I’ll defer to your expertise on diet.

Benoit, I agree.

Thaomas, You could regard the dollar peg as HK’s instrument. Once they adopt that peg, nothing else really matters (in terms of monetary policy.)

HL

Apr 17 2016 at 11:50pm

Another brilliant post!

I guess the PBOC was trying to achieve something similar to Singapore’s (basket, band, and crawl) to mitigate trilemma, but it seems much trickier to pull that off with the capital account liberalization in progress. I still don’t know if BBC is workable for any large open economy, but at least for small city states I strongly agree that Singapore’s framework is better than Hong Kong’s.

david

Apr 18 2016 at 5:19am

Singapore engages in direct countercyclical engineering of the wage rate via tweaking the employer’s contribution rate to the national ISA fund. This swamps any impact on the nominal wage bill from monetary policy.

Pacemaker

Apr 18 2016 at 11:23am

david, I recall the Singapore government saying that they are no longer as keen at using CPF contribution rates as countercyclical policy due to the impact on retirement savings.

Scott, the policy david mentioned is equivalent to changing the employer-side payroll tax, which I recall is your least abhorred form of fiscal policy. The most recent use of that policy was during the Asian Financial Crisis. In more recent times, the government seems to have used direct income transfers. They have sometimes cited countercyclical reasons for those income transfers though I suspect the reasons are more populist.

Scott Sumner

Apr 18 2016 at 11:57am

Thanks HL. Yes, size is an issue. China faces resistance from other countries that is not a problem for a small nation like Singapore.

David, Yes, that’s the sort of clever idea you’d expect from Singapore.

Pacemaker, Thanks for that info.

mbka

Apr 18 2016 at 11:43pm

Pacemaker, Scott,

David used the more appropriate wording here. The Singapore government didn’t change the payroll tax, because there is no such equivalent tax in Singapore. What the government did, and as recently as after the 2008 crisis, was to temporarily reduce employers’ mandatory retirement savings account contributions. Since this is part of an employee’s earned income (paid out to the individual savings account), this effectively constitutes a pay cut. And this pay cut helps employers. At the same time, it is not visible in present consumption by employees because it only affects what would have gone into savings. But a pay cut it is.

BTW – yes, these mandatory savings contributions would be counted as a tax in the US (Social Security) but they aren’t counted as a tax in Singapore (because they’re savings into identifiable retirement accounts). If these contributions were counted as taxes, Singapore would look pretty high tax (30% by savings contributions alone, plus applicable income taxes on the rest of the salary or income). Corollary, that’s why I laugh at the international tax comparisons people do. Retirement savings are counted as “tax” when funneled through the global government budget (Social security in the US, Europe) but is counted as “savings” when funneled through a government run IRA (example Singapore). When in fact either contributions are automatic and mandatory.

mbka

Apr 18 2016 at 11:53pm

Scott,

I am also scratching my head at this

” For instance, in Hong Kong the government dominates the all important real estate industry.”

You’re sure you don’t mean Singapore? Here, about 85% of the population lives in government built housing estates.

Scott Sumner

Apr 19 2016 at 10:20am

mbka, I knew that Singapore also dominates real estate, but I mentioned Hong Kong because they are the most “free market” country in the world.

Thanks for your information on payroll contributions. I agree that the term “tax” is rather poorly defined, but what makes a US Social Security contribution a “tax” is that the money goes to someone else. I’d consider the Singapore plan to be forced saving, not taxes. More analogous to the Obamacare plan, which forces people to buy health insurance. But I can see how some might consider that a tax as well.

Taxes are most useful as a “wedge” concept, so countries with bigger tax wedges are countries with bigger gaps between what you produce and what you are paid for that production. Let’s suppose Singaporeans value retirement savings at 80 cents on the dollar, that would make the tax wedge about 6% of income (.80X30%)

TheManFromFairwinds

Apr 19 2016 at 3:50pm

“After 2002, Argentina crawled into a much safer house, but then adopted some really bad habits, and his health eventually deteriorated as he lay on the sofa all day eating high cholesterol steaks.”

But now, specifically in December 10th 2015, we looked in the mirror, went “this is me?” and decided to hit the gym. After 4 months of losing deficit fat, settling old lawsuits, and ending currency controls we have attracted far more looks from investment banks. Now this week we are about to issue 15bn in debt at 1% lower rates than expected for the 10 year notes.

Comments are closed.