Rajat directed me to a post by Miles Kimball, entitled “Pro Gauti Eggertsson”. He discusses Eggertsson’s views on the role of inflation expectations in the recovery from the Great Depression. Like Miles, I’m a big fan of Eggertsson’s work on the role of dollar depreciation, and particularly the expectations channel. Unlike Miles, I strongly disagree with the view that higher inflation expectations from adverse supply shocks can be expansionary, even at the zero bound. Here’s Miles discussing Eggertsson’s work:

In “Was the New Deal Contractionary?” (to which his answer is “No”) Gauti argues that the much derided National Industrial Recovery Act was useful as a way to raise inflationary expectations. And he argues that its explicitly temporary nature was a recognition that ordinarily raising inflation expectations is a bad thing, but under the extraordinary circumstance of the Great Depression when the economy was hard up against the zero lower bound on nominal interest rates, higher inflation expectations could be helpful. Together with “Great Expectations and the End of the Great Depression,” this paper constitutes a major bit of revisionist economic history, countering the generally dim view that many economists have taken of the details of FDR’s policies as anything more than sleight-of-hand confidence-building measures. (Here there is some danger I am projecting onto others my own view before reading Gauti’s papers, but I do not think I was alone in those views.)

In macroeconomics, there are very few propositions that we can be relatively certain are true. One of those is the claim that Paul Volcker’s tight money policy of 1981 triggered a severe recession. Another is that the NIRA slowed the recovery from the Great Depression. In my view this claim is not even debatable. There is a large empirical literature on this, by many researchers, using a variety of techniques. My recent 500-page book on the Great Depression devotes about 25% of its pages to showing that FDR’s 5 wage shocks (the first of which occurred under the NIRA in July 1933) each sharply slowed the recovery in monthly industrial production.

If the empirical evidence is clear, what about the theory? Why aren’t higher inflation expectations expansionary? The simple answer is that looking at inflation expectations is reasoning from a price change. Thus if inflation rises due to a positive AD shock (more NGDP) then both prices and output will rise in the short run. But if NGDP is unchanged, then higher inflation leads to lower output. That’s why supply shocks are contractionary.

The New Keynesian models are simply wrong. The role played by inflation expectations in NK models should be played by NGDP growth expectations. Switching to NGDP allows us to avoid reasoning from a price change, and avoiding mistakes like the claim that adverse supply shocks can be expansionary.

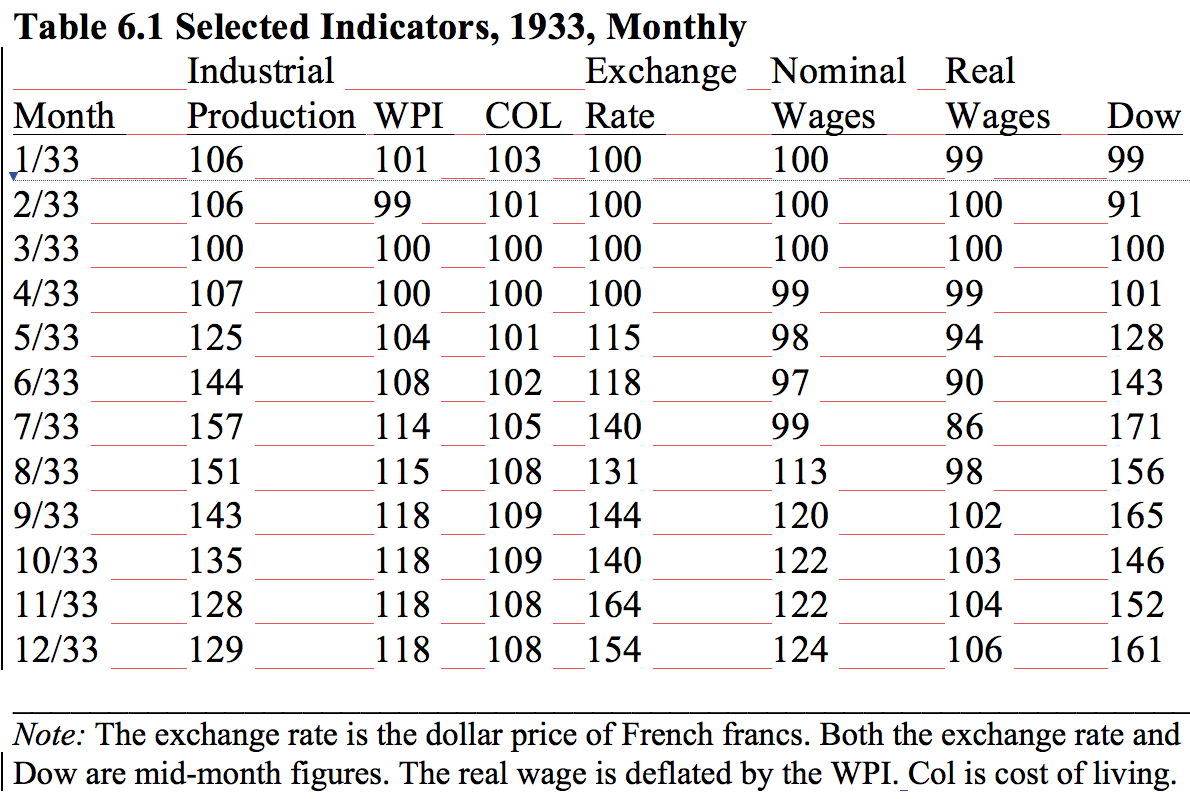

Companies do not care about inflation expectations; they care about total revenue expectations—which are tied in to NGDP growth. If you tell steel companies that they must raise their hourly wage rates by 20% in two months (as FDR did to steel and other manufacturers in July 1933) then the steel companies may expect higher steel prices, but they will also expect lower profits, as steel prices would probably rise by less than wages. They would react by sharply cutting production, which is exactly what manufacturers did after July 1933 (until the NIRA was declared unconstitutional in May 1935, after which industrial output soared.) In contrast, if you tell steel companies that you are going to sharply devalue the dollar, as FDR did in April 1933, then they will expect higher revenue from selling steel. This will make both steel prices and steel output rise rapidly. Indeed industrial production soared 57% between March and July 1933, after which FDR’s NIRA aborted the recovery for 2 years.

It’s about as perfect a set of natural experiments as I’ve ever seen, at least in the field of macroeconomics. The following table shows some data for 1933, in case you are interested.

READER COMMENTS

Brian Donohue

Jul 28 2016 at 12:36pm

Another excellent post.

I do think, as an empirical matter, that higher inflation expectations have gone hand in hand with higher REAL interest rates over the past six years (and, as seen this year, lower inflation expectations and lower REAL rates go hand in hand too), which I think is interesting and not intuitive and not a general rule, but something peculiar to the times in which we currently find ourselves.

Just started The Midas Paradox. Delicious.

Effem

Jul 28 2016 at 12:50pm

I assure you companies care about future profits more so than revenue (if not, i have a few companies to sell you). And the split between real growth and inflation matters immensely for profits.

Scott Sumner

Jul 28 2016 at 12:58pm

Brian, The pattern you see may be partly cyclical. And thanks for reading my book.

Brian Donohue

Jul 28 2016 at 2:41pm

Scott, Yeah, I can’t distinguish cyclical/secular, but I get the sense there is some trend (not the Fed) driving rates lower. My contention is that spasms of QE arrested and temporarily reversed this trend.

Nominal interest rates don’t interest me as much. It’s obvious to me that a looser monetary policy would increase long-term rates by increasing expected inflation. I want to see past this trivial result.

So, I look at TIPS yields instead. Yeah, the data are noisy, but it sure looks to me that QE raised real rates (particularly the most Chuck Norris-like QE3), while tapering/ending QE and increasing rates last December produce lower long-term real rates.

Scott Sumner

Jul 28 2016 at 3:59pm

Effem, Of course they care more about profits than revenue. My point is that revenue is more relevant than inflation when thinking about future profits.

And yes, the split matters. My point is that they’d prefer lower inflation, for any given NGDP growth rate.

Brian, I think that is quite possibly true, but hard to prove definitively.

Lorenzo from Oz

Jul 28 2016 at 7:20pm

Why would people think that economic agents would somehow decompose future transactions into the “real” bit and the “inflation” bit? First, how? given the enormous difficulties in measuring inflation. Second, why? What’s in it for them to carry the information and cognitive burden of doing so?

People estimate income and expenditure, because that’s how you pay your bills (or not), and that juggling is not changed by adding a whole level of complication to the process.

In a monetised economy, money is not an after-thought of “real” transactions. Money is one side of (almost all) transactions. We don’t actually exchange “real” goods, we provide goods and services for money which we use to buy goods and services. Money illusion occurs precisely because money is the basic and pervasive medium of transaction.

One suspects obsessing over interest rates has a role to play here. It is all very well for economists to decompose interest rates into their various components but it is still the (expected) money flows that come first.

Scott Sumner

Jul 29 2016 at 2:57pm

Lorenzo, Good comment.

Lorenzo from Oz

Jul 29 2016 at 10:13pm

Thanks Scott: it’s good to know you’re not missing something crucial 🙂

Aristotle Magganas

Jul 31 2016 at 7:13pm

Scott: A paper coming out of Berkeley recently goes through the evidence on this in the case of France in the Thirties. http://behl.berkeley.edu/files/2013/02/WP2015-08_Cohen-Setton_etal.pdf

Comments are closed.