The Wall Street Journal has a very interesting story on the BOJ, which faces an important policy decision on Wednesday:

Until recently, Bank of Japan Gov. Haruhiko Kuroda managed to keep a fragile majority on the nine-member board in favor of his preferred easing steps. A decision in January to introduce negative rates on certain commercial-bank deposits passed 5-4. Two of the dissenters later left when their terms expired, replaced by supporters of easing.

That should have given Mr. Kuroda a comfortable majority. But the seven supporters of easing now have fractured over where to go next, say people familiar with their thinking.

At least three in this camp favor sticking with the plan, convinced that both huge government bond purchases and negative rates are still effective in forcing private money to flow into riskier assets. This faction thinks curbing those purchases, or even tinkering with the buying formula in a way that markets might perceive as tightening, could send the yen soaring, according to people familiar with its views, which is the opposite of the policy’s intended effect. That could hit corporate profits and the stock market.

Others, while still pro-easing, are no longer confident bond purchases can get the job done. Some including BOJ staff have floated the idea of flexibility in the buying. In place of the current commitment to buy ¥80 trillion of government bonds a year, some in this group have suggested a range, perhaps ¥70 trillion to ¥90 trillion.

The two sides get particularly heated over whether Japan is running out of bonds to buy, according to people familiar with the deliberations. The pro-flexibility faction says the practical limit could come in the next year or two as banks, which often use government bonds as collateral in day-to-day operations, become reluctant to sell more of their holdings to the central bank.

These board members believe the BOJ should begin looking for policy alternatives, according to people familiar with their thinking, such as introducing a target for long-term interest rates and pledging to buy only the amount of bonds needed to guide rates to that target.

The thought is that such a move–which former Fed Chairman Ben Bernanke has endorsed as an option in certain situations–could reassure people that borrowing costs will stay low while giving the BOJ room to reduce purchases if necessary.

Opposing the idea, one easing proponent said “any grade-school student can tell with a little arithmetic” the BOJ can’t buy bonds forever, “but it’s strange to be deciding policy today based on some future limit when…we haven’t reached that limit.”

The seven pro-easing board members nonetheless agree that lowering interest rates further into negative territory should remain as an option.

I find that both sides of the monetary policy debate miss a very important point. In the long run (and even in the medium run), the slower the rate of NGDP growth, the larger the share of NGDP held in the form of base money. This is the “inflation or socialism” trade-off that Nick Rowe and I frequently discuss.

Most of the world sees things very differently. They see a bigger central bank balance sheet as being expansionary (and sometimes it is) and expansionary policies leading to faster NGDP growth. In this view, bond purchases become “ammunition” to be used to propel the economy toward higher NGDP growth. In contrast, I see QE as mostly the effect of low NGDP growth. The central bank accommodates the public’s growing demand for zero interest base money as NGDP growth slows.

Why is NGDP growth so important? Because the long run rate of NGDP growth is positively correlated with the nominal return on owning stocks, bonds and real estate, which are all substitutes for holding base money. In countries with very rapid NGDP growth, people and banks don’t want to hold very much zero interest base money–they have better options.

If anxiety over a large balance sheet causes a central bank to refrain from purchasing assets, this will slow the rate of NGDP growth. In the long run this will lead to more demand for base money, which the central bank must eventually accommodate if it wants to avoid a depression. Thus if the Japanese demand for base money doubles from 20% of GDP to 40% of GDP, the BOJ must either double the base, or see NGDP fall in half. The US tried the latter approach in 1929-33, and it didn’t turn out very well.

This relationship is often hard to see, because in the short run the correlation between QE and NGDP growth may be positive and (more importantly) because what matters is expectations of future policy, not current changes in the base.

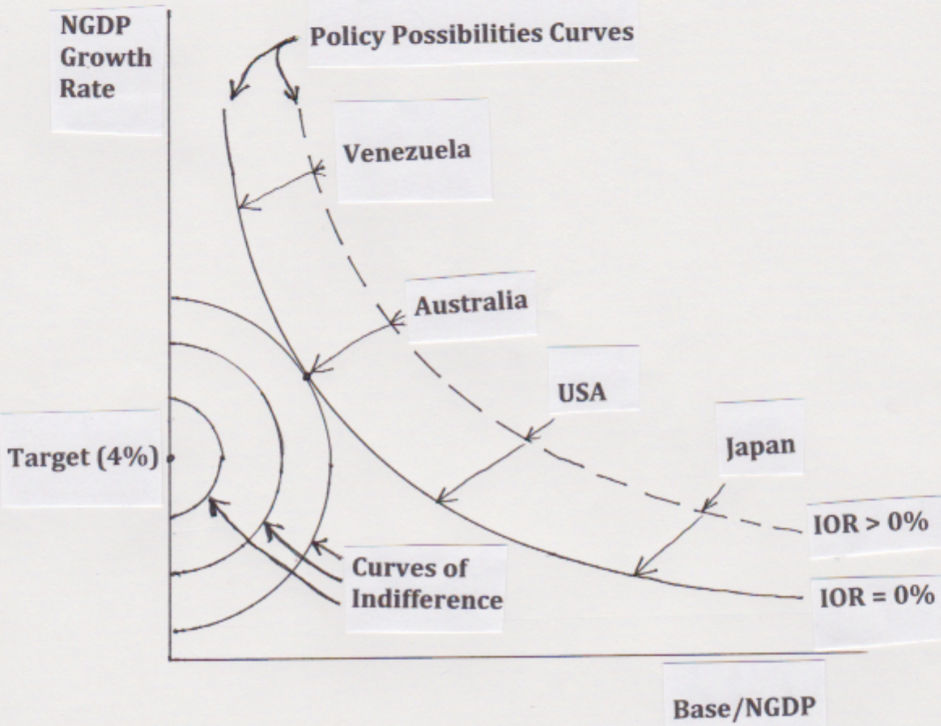

I’ve developed a graph that allows readers to visualize this point. The two convex lines are PPFs—policy possibility frontiers. I’ll focus on the one assuming no interest on reserves (IOR=0%). That line shows all the possible combinations of NGDP growth and base/NGDP ratios, in the long run. If NGDP growth is extremely high (almost always due to high inflation), people won’t want to hold much base money—say 2% of GDP. That might be a country like Venezuela. At a somewhat lower NGDP growth rate, base demand will be higher. Australia’s base has been about 4% of GDP in recent decades. The US has still lower NGDP growth, and a base of over 20% of GNP. And Japan’s NGDP growth rate has averaged about zero in the past 22 years, and its base to NGDP ratio is roughly 80% of NGDP.

So the two lines that slope down and to the right show the tradeoff between inflation and socialism. If you want lower NGDP growth (i.e. lower inflation), then the public will demand more base money as a share of GDP, and the central bank will end up owning a bigger share of the economy. That’s not a problem if all they own is government bonds, but the BOJ has also purchased equities.

Put aside your own view on big central bank balance sheets. Let’s take the central bank anxiety as a given. Suppose the target NGDP growth rate is 4%, which is assumed to best trade off the costs of low NGDP growth (an inefficient labor market) and higher NGDP growth (inefficient excess taxation of capital income.)

Central banks then have “policy indifference curves” which are sets of points that are equally desirable to policymakers. I’ve drawn three of them, rippling out from the (assumed) optimal 4% NGDP growth point. (I assumed a zero balance sheet is optimal, which is unrealistic, but changing that to 5% of GDP would not change anything important—you’d have circles instead of semicircles for indifference curves.)

As you go further out from the 4% optimal point, policy becomes less desirable. In this exercise, Australia reached the highest policy indifference curve, while the other three had either too much NGDP growth (Venezuela) or too big a balance sheet (the US and Japan.)

With the exception of a few market monetarists, almost no one understands these trade-offs. Over the past 7 1/2 years I’ve devoted far more time to trying to convince people that this is the right way to look at the world, than I have to defending NGDP targeting.

People at the Bank of Japan and the Swiss National Bank think they can have a smaller balance sheet if they adopt a tighter monetary policy, but in the long run just the opposite is true. On the other hand, it’s hard to blame them, because in this case the truth is far stranger than the fiction. Here’s the truth:

If the BOJ want’s to avoid a socialist outcome, where it owns much of the Japanese economy, then it should announce the following policy on Wednesday:

“We plan to start buying massive quantities of a wide variety of assets, and will continue doing so at a rapidly accelerating rate, until NGDP growth expectations rise to 4%”

That’s what the Bank of Japan should do Wednesday if it wants a smaller balance sheet. No wonder only a few lonely market monetarists see the world this way, it’s about as counterintuitive as you can get.

PS. My dream is that someday this graph appears in Mishkin’s money textbook. In that case I’ll die a happy man.

READER COMMENTS

Matthew Moore

Sep 18 2016 at 6:19pm

Since you are looking for feedback on the graph, I’m going to make a suggestion that I think is probably not an improvement, but has a small possibility of being helpful:

Invert both axes. Then your ICs and your PPFs have the standard shape. Call the axes ‘slower NGDP growth’ and ‘lower base/GDP’. Since you have a policy bliss point, there’s no monotonicity of preference on either axis, so there’s no loss of clarity there. Then any economist sees it immediately, and you don’t impose any excess cognitive cost, which can be a major barrier to people accepting a new idea.

Joe Calhoun

Sep 18 2016 at 8:26pm

I offer this, tongue planted less than firmly in cheek: if a smaller balance sheet is associated with higher NGDP growth, shouldn’t the BOJ, ECB and Fed be selling assets? If the 10 year Treasury yield is a decent proxy for NGDP growth why do we need an NGDP futures market? Why not just target the 10 year yield?

Pretty chart….

Joe Calhoun

Sep 18 2016 at 8:40pm

As a followup to my previous comment: If the goal of the central banks is to get investors to sell their Treasuries and go do something more productive with their capital, what better way than for the Fed to announce after their next meeting that they have decided to take whatever actions are necessary to raise the yield of the 10 year Treasury to, say, 3%?

Lorenzo from Oz

Sep 18 2016 at 9:12pm

Once explained, the graph is clear. Though labelling the otherwise mysterious lines radiating out from the optimal policy point would likely be helpful.

Joe Leider

Sep 18 2016 at 11:13pm

Isn’t NGDP growth rate your independent variable, because that’s what central banks control? That means it should be the X axis. The y axis should be the dependent variable, base/NGDP, because base/NGDP ‘results from’ the NGDP growth rate.

What you’re really trying to convince people is that NGDP growth is the independent variable. So flip those axes or else you’re saying the exact opposite, no?

Gary Anderson

Sep 19 2016 at 1:37am

Isn’t asset inflation a tax if wages don’t rise? I would like market monetarists to prove that isn’t the case. It is a legitimate question from a non economist, especially when it appears that $147 oil helped slow down the economy in 2007.

I realize it was not the Fed that grew the price of oil, according to the Saudis it was the investment banks (according to Wikileaks.)

Jose Romeu Robazzi

Sep 19 2016 at 9:22am

Since what the central bank really controls is the base money quantity, it looks ok to put base money on the x-axis.

People really should be convinced of why higher asset prices are a symptom of tight money. A lot of people dismiss monetary policy because they say bonds and money are interchangeable, they are the same thing. But this argument is self defeating: if bonds and base money are interchangeable, then high demand for bonds means also high demand for base money, which in turn means monetary policy is tight.

Prof. Sumner, what you should continue to press on is that real investments are not undertaken just because financing is cheap. First, the entrepreneur must believe nominal demand for his/her products will be strong. If they believe that they will turn money reserves into real assets and employment. Also, if that is true, a 1% point higher or lower financing cost will be a detail on a spreadsheet, nothing else…

Rob Thorpe

Sep 19 2016 at 10:36am

I don’t see how this makes sense. Throughout the 19th century there was no long-run inflation in the US or UK. Surely by this logic the balance sheets of the Central Banks should have been massive?

Scott Sumner

Sep 19 2016 at 11:02am

Matthew, Thanks, but what would the origin represent in that case?

Joe Calhoun, No they should not sell assets, as the short term effect is different from the longer term effect. And long term bond yields are not closely enough correlated with NGDP growth to serve as a useful target.

You said:

“If the goal of the central banks is to get investors to sell their Treasuries and go do something more productive with their capital,”

That is not the goal. The goal is to stabilize NGDP growth.

Thanks Lorenzo.

Joe Leider, Good point, but economics has a long tradition of mixing these up. Think about the demand curve.

Rob, Good point, but the curves have shifted over time due to the massive expansion in safe assets with very low yields. In the 19th century, the alternatives to money offered positive rates of return.

In addition, at that time gold and silver were the media of account, not cash.

Matthew Waters

Sep 19 2016 at 5:23pm

“We plan to start buying massive quantities of a wide variety of assets, and will continue doing so at a rapidly accelerating rate, until NGDP growth expectations rise to 4%”

So, buying corporate bonds and equities do need to be on the table for expectations to work? Broadly, there are three possibilities for creating NGDP growth at the zero-bound without expectations. The “zero-bound” means moderately negative IOR.

1. Fiscal stimulus.

2. Central Bank purchasing risky assets, which may include NGDP futures.

3. Restrictions on printing and holding of physical cash.

The tradeoff isn’t between “socialism and inflation” as much as “nuttiness and inflation.” Whether with leaving the gold standard or eliminating cash, the actions required at the zero-bound are nutty by conventional standards.

#3 is the most palatable. What about a policy where, if the Fed has negative IOR, any withdrawals from a Fed branch are charged interest up front? Let’s say the Fed sets rates at -1% IOR. If the bank wants to exchange $1 mil. in their account for $1 mil. in bank notes, the Fed “charges” interest up front on the $1 mil. in reserves for 10 years. So an account withdrawal of $1 mil. gets $900,000 in cash.

The dynamics between banks and their depositors would change a lot. There could be speculation on cash itself versus the deposit equivalent. But with Macroeconomics and NGDP, that’s neither here nor there. It’s clear how NGDP targets would be hit without fiscal stimulus or risky asset purchases. It would be more clear to the lay public, as much as they wouldn’t like it, than things like NGDP futures.

Matthew Moore

Sep 19 2016 at 7:07pm

Origin still zero, it’s just the in the top right (or middle right, if you extend the axis to include negative rates of NGDP growth’s which might be useful for analysing policy errors)

Gary Anderson

Sep 19 2016 at 7:28pm

The goal of central bankers is for people to buy government treasuries, not sell them. And they have done a bang up job, assisting the creation of structured finance that has created massive demand for treasuries and bond yields declining in good and bad times.

Market monetarists, who are likely right about yields rising creating more banking activity and more activity in the real economy (Jamie Dimon said that was true),underestimate the power of demand for long bonds that now exists.

Dimon said there exists a shortage of long bonds. Tantrums come and go yet yields go down. You either spend fiscally to get more bonds for Wall Street, or you slow the economy so much that the debt is created without trying.Either way, I fear Wall Street gets what it wants without the US government or its citizens getting anything in return except for a bridge or two and more debt.

Also, the Fed stopped purchasing long bonds, stopped QE, and what happened? Yields went down. And for that, Market Monetarists, who I agree with on most things, have NO ANSWER.

One more point. If people see their dollar eroding, they would possibly buy house, but they go down too. If they see their dollar eroding because of asset inflation, they know it is a tax and may save more. And they know the other shoe could drop, a financial crisis that robs them of their equity in their house.

Enya said what will make things change. Only time. Millennials won’t forget. They hate bankers. And for good reason. They saw what they did to their parents.

joe

Sep 19 2016 at 9:27pm

looks like a recast of MV=PY

Scott Sumner

Sep 20 2016 at 9:14am

Matthew, You said:

#3 is the most palatable.”

i strongly disagree, In any case that option would not be politically acceptable. A far better solution is a NGDP growth rate high enough to avoid the zero bound problem. Second choice would be a bigger balance sheet.

Alex Schibuola

Sep 21 2016 at 12:39pm

“If anxiety over a large balance sheet causes a central bank to refrain from purchasing assets, this will slow the rate of NGDP growth. In the long run this will lead to more demand for base money, which the central bank must eventually accommodate if it wants to avoid a depression.”

This paragraph struck me as the winner.

Is it safe to say the following:

1) central banks have lost their credibility.

2) central bankers are using the wrong models-despite systematic errors on their part (e.g., not hitting their inflation target). Therefore, policy makers are less rational than markets. Just one more argument in favor of using NGDP futures market to conduct OMO rather than the FOMC.

3) one might argue expectations of low NGDP growth should have adjusted by now as Japan is now 27 years into no NGDP growth, while the US, the UK, and Euro area are now 8 years into weak GDP growth. Can it be presumed that the issue reverts back to points 1 and 2? I.e., markets recognize that if they act today (hire people/invest in capital) in expectation of better growth, they know the central bank will pull the rug right out from under their feet. Therefore, they just hold base money and wait for central bankers to read your blog?

It’s a shame central bankers learn with long and variable lags. Keynes was wrong. We’re all dead in the short-run.

Comments are closed.