We live in an age where everything official seems to be distrusted. Trump has suggested that the government’s unemployment data is incorrect, and that the actual rate may be as high as 40%. Some economists on the left also question the data. While progressives may not see a conspiracy, they claim that there is much more slack in the economy than suggested by the (U-3) unemployment rate.

I’m skeptical of the rigged claim. The government produces 6 different unemployment rates, some of which include discouraged workers and part-timers who’d prefer to work full time. In addition, the data is produced by non-partisan bureaucrats, and does not seem affected by a change in who’s in the White House.

The biggest problem with conspiracy theories is that they’d have to cover too much ground. It would not be enough to fake one of two data points; you’d have to recreate all of reality in an almost “Matrix-like” fashion. For instance, suppose China wanted to falsely pretend that it’s been a fast growing economy since 2000. It wouldn’t be enough to fake GDP data, they’d also have to pressure Western companies like GM and VW to fake auto sales data; to falsely claim skyrocketing cars sales to the Chinese public. That sort of all encompassing conspiracy is very hard to pull off. And if something like that were being done, it would be odd for the Chinese government leadership to itself question the accuracy of the data—they’d want to loudly insist it was accurate.

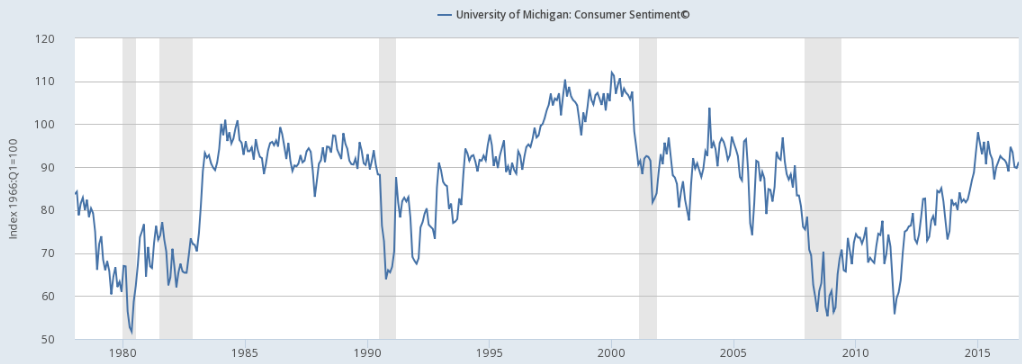

I believe the current unemployment rate of 5% does accurately reflect the state of the US labor market. One piece of evidence for this is that the public currently seems pretty upbeat about the economy. If the data were falsely creating an upbeat picture, you’d expect the Michigan Survey of Consumer Confidence to show a much more pessimistic picture:

In fact, the level of consumer confidence is about the same as in 2005-06, 1995-96, and the late 1980s, which were also periods when unemployment was close to the natural rate.

And yet RGDP growth has been quite slow over the past decade, suggesting we do have a problem. In my view, we are now at a position where we can’t expect demand stimulus to do much more for the economy. Unlike in 2009, when unemployment was 10%, there is no large reserve army of unemployed just waiting to find jobs. That’s not to say there is no slack, it’s quite possible that we could have another year or two of above trend growth, driving unemployment down to 4.5%. But for a major improvement in the economy, we need serious supply-side reforms.

Of course neither of the two major candidates is a supply-sider—just the opposite, so I’m going to stick with my pessimistic view that 1.2% RGDP growth is the new normal. That’s roughly the rate over the past decade, and I expect similar growth over the next decade.

HT: TravisV

PS. I’d like to congratulate Ben Klutsey for winning the Great Communicators Tournament in Washington DC on Wednesday night. Some of you may know that David Beckworth and I both participate in the Mercatus Center’s Program on Monetary Policy. Unfortunately we both live some distance from the headquarters in Arlington, VA. Ben is the program’s manager, and does a lot of the behind the scenes work that readers might not be aware of. I feel lucky to work with someone who is both a very nice guy and a highly talented manager.

Also congratulations to runner-up Charles Blatz, another Mercatus employee.

READER COMMENTS

The Original CC

Oct 29 2016 at 8:34am

Cool post. What do you think is the low-hanging fruit for supply-side reform? (Low-hanging could mean politically palatable for both parties, or that the gov’t is unlikely to mess it up along the way, or that it’s very likely to be very effective, etc.)

Pajser

Oct 29 2016 at 12:01pm

What is real GDP? Is it data from bea.gov? My calculation on the base of that data is that average growth in “GDP in billions of chained 2009 dollars” was 1.43% per year in last ten years. But, it doesn’t seem to be growth per capita, as US population has grown nearly 14% in last ten years, it seems as stagnation to me. Do I read that wrong?

World Bank claims that USA GDP (PPP) per capita in const 2000 Intl.$. progressed barely 6% (per capita) in period 2005-2015. Is it same or similar measure, except maybe for a year which is used for comparison? If it is, difference is significant. And 6% is still very slow, particularly if employment is good.

I tend to believe USA official data, and many other countries official data – mostly because I rarely find evidences that data was falsified in past.

Craig

Oct 29 2016 at 4:44pm

Scott,

Do you think that there should be more stimulus to get inflation expectations up, even if it won’t increase RGDP? 5-year break even is at 1.57.

Elizabeth

Oct 30 2016 at 2:32pm

Great post Scott. I, too, am a big fan of both Ben and Charles. I must point out though that Charles currently works for IHS!

Farid Elwailly

Nov 2 2016 at 4:42pm

Scott,

You’ve made this point a number of times and I tend to believe you since the employment picture is looking better but growth is low.

Does this imply that an NGDP shock that lasts too long has a long term effect on supply factors that cannot be fixed by raising NGDP (and hence inflation) for a while?

Or is your thinking that the supply situation was getting worse even before the NGDP shock? If this is the case, has the shock been keeping us from implementing supply-side reforms?

Maybe we should run inflation high for a while and that will make some of the supply-side reforms more readily desirable. (ex. controlling for rising labor costs by investing in automation.)

Comments are closed.