Most economists view the Fed as a sort of firefighter, an institution that pushes back against “shocks” that mysteriously arise in the private sector. Bob Hetzel and Josh Hendrickson have a different view. Here’s Josh:

The predominant difference between this view and the Taylor view presented above can be expressed in terms of whether the Federal Reserve can be seen as an inflation fighter or an inflation creator, as summarized by Hetzel (2008a). The inflation-fighter view suggests that ”inflation shocks are the initializing factor in inflation” and ”explanations of inflation stress FOMC failure to respond aggressively to realized inflation” Hetzel (2008a, 273). The inflation-creator view of monetary policy emphasizes that the central bank influences the price level through the control of a nominal variable. . . .

According to the Taylor view, the change in post-1979 policy was the more steadfast commitment to respond to inflation. The Federal Reserve became an effective inflation fighter.

The alternative view put forth in this paper suggests that the change in policy was not simply a renewed commitment to fighting inflation, but rather an acceptance of the Federal Reserve’s role as inflation creator. The nominal variable that the Federal Reserve sought to control to influence the price level was expected inflation and the means of doing so was a commitment to low, stable rates of nominal income growth.

I agree with Hetzel and Hendrickson. Alex Tabarrok and Saturos directed me to a Kevin Grier post:

After the events of the great recession, it’s just amazing to me that people think the economy is a steak, the Fed is a precision sous-vide machine, and all we have to decide is medium-rare or well-done.

For the millionth or so time, the models implying the Fed can do this, completely and utterly failed during the great recession. There is also evidence that a large part of the good outcomes credited to the Fed during the great moderation were actually due to exogenous forces (i.e. good luck).

Neither the Fed nor the President “runs” the economy. There is no stable, exploitable Phillips Curve / sous vide machine that lets us cook at a certain temperature.

This Fed worship is more religious than scientific. The past 10 years should be enough to convince anyone with an open mind that the Fed’s power over the economy is quite limited and tenuous.

Let’s start with the question of what it means to “control” an entity called “the economy”. What does ‘control’ mean, and what is “the economy?” If the economy means real GDP (and that’s usually what people mean when they say “the economy”) then Kevin might be right. If ‘control’ means move RGDP where it wants, then he is clearly right. He’s also correct that the Phillips Curve is not a useful model for controlling “the economy.” That’s why I oppose Yellen’s suggestion that we might want to run the economy hot for a while to fix labor market problems. Please Fed, just refrain from causing more problems. You’ve done enough damage already

On the other hand, while the Fed cannot control RGDP in the sense of moving it where it wishes, it can destabilize RGDP through unstable monetary policy. Fed policy during the Great Moderation did not stabilize the economy by fixing problems, or pushing RGDP to the right position, rather it reduced instability by refraining from introducing as many monetary shocks.

While the Fed has only very limited ability to influence RGDP, one variable that it absolutely can control is expected growth in NGDP. Although the terms NGDP and RGDP sound similar to the uninitiated, they are actually as different from each other as a poem and a cement truck. One is a way of describing a vast real, physical economy, and the other is a way of describing the value of the medium of account.

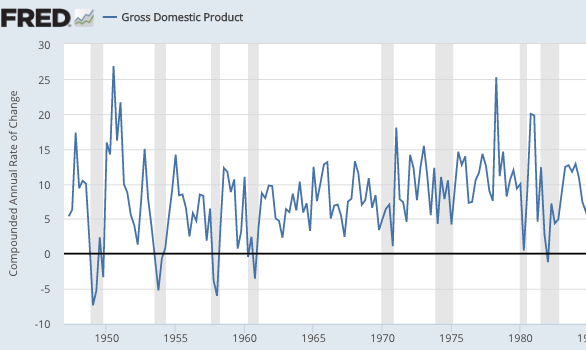

During the Great Moderation, the Fed made the path of expected NGDP much more stable than prior to the Great Moderation. As the following graphs show, this also made the path of actual NGDP much more stable.

Now this greater nominal stability does not, in and of itself, make the path of RGDP more stable. Recall than in 2008 Zimbabwe’s NGDP soared a zillion-fold, even as its RGDP fell into depression. They are very different variables.

And yet under some conditions NGDP can impact RGDP, at least in the short run. This is especially like to occur if nominal hourly wages are sticky. Thus one side effect of making NGDP more stable is that one also makes RGDP more stable. In 2008, the Fed took its eye off stabilizing NGDP and focused on (high) inflation. This led to a big fall in NGDP, and the Great Recession resulted. In his recent memoir, Ben Bernanke admits that Fed policy was too tight in September 2008, and indeed the same could be said for the entire second half of the year—probably the first half as well.

Some people question whether the Fed really “did anything” to create the Great Moderation. It depends what you mean by “did anything”. Most economists don’t know how to identify monetary policy changes, and hence in their empirical work they struggle to find evidence of the Fed having much effect on the economy. If they defined monetary policy in terms of expected changes in NGDP, then the role of the Fed would be much clearer. If at the same time the government created a deep and highly active NGDP futures market, then monetary shocks would be even easier to identify. But you go to war with the generals you have, not the generals you wished you had. And we don’t have a highly active NGDP futures market.

I like to use the arsonist metaphor to force people to think about central banks in a different way. But perhaps the Fed is neither an arsonist nor a firefighter. Maybe the Fed is like a ship captain, which can do his or her job well, or poorly. If so, then the ship is not “the economy”, it’s the value of money.

The value of money can be defined in many different ways; I prefer 1/NGDP.

PS. The Great Moderation may be clearer if we look at the entire period of NGDP growth, on one graph:

READER COMMENTS

Benjamin Cole

Oct 20 2016 at 10:03pm

Great post.

Kevin Grier’s post is dispiriting, and appears to be another right-wing statement that the Fed should do nothing, that the Fed has been accommodative, and tight money is best.

Actually, the Fed, and other major central banks, have been practicing tight money since about 1982, which is why secular trends in interest rates and inflation are down, and now we have reached deflation in much of the developed world.

This is persistently tight money! What other explanation holds water?

The central banks, however, have ossified into their inflation-fighting mindsets, and now cower in fear of 2% inflation.

The central banks need to become much more pro-growth.

Besides which, the Fed is always “doing something.”

The manager who leaves a pitcher on the mound who is getting bombed is not “doing nothing.” If your neighbor’s house burns down, and you watch but do not call the fire department, you are not “doing nothing.”

It is sad to see nearly the entire American right-wing devolve into the School of Monetary Suffocation.

Four times in his career Milton Friedman bashed central banks for being too loose: The Great Depression, 1957-8 in U.S.; in Japan in the 1990s; and in again in 1992 the U.S. Fed.

Today no right-wing economist is allowed to say the Fed is too tight. It is not PC.

Left-wing economists are worse, but for other reasons.

Khodge

Oct 21 2016 at 12:27am

Yes. So obvious and yet so hard to dislodge from mainstream thought

bill

Oct 21 2016 at 10:07am

Here’s some text from:

https://en.wikipedia.org/wiki/Firefighter_arson

Firefighter arson is a persistent phenomenon involving a small minority of firefighters who are also active arsonists. Some of the offenders seem to be motivated by boredom, or by the prospect of receiving attention for responding to the fires they have set.

See also hero syndrome.

I see elements of this in the Fed today. Not content with 1.5% inflation and 5% unemployment, it’s time to add “financial stability” to the mandate even while NGDP growth is now below 3%.

Regarding Grier’s post. I’ve had steaks cooked just like I ordered them and others that were ruined by the cook.

@Ben Cole. Did you reverse loose and tight in the last couple sentences in your comment? Thx.

Thaomas

Oct 21 2016 at 12:28pm

I’d say that 2008-present, the Fed has taken it’s eye off the ball of maintaining consistent price level growth (and expectation thereof) in favor of keeping a ceiling on the ST inflation rate. I suspect this had a lot to do with the fall in RGDP after the financial crisis and the excruciatingly slow recovery.

Benjamin Cole

Oct 21 2016 at 11:56pm

Bill: You are correct sir!

Comments are closed.