A commenter named Captain Parker recently left this comment:

Ok, so, inflation is a monetary phenomenon and Burns should take the blame. This I believe. Yay Milton Friedman.

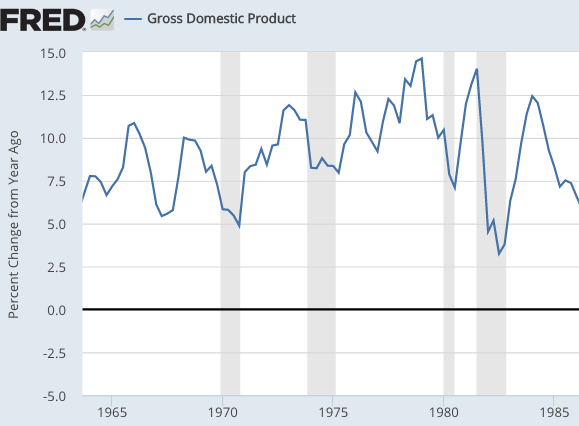

But if you look at ’72 through ’76 you would conclude Burns was doing a pretty good job of creating a nice stable growth path for NGDP (exactly like a market monetarist would want) yet real GDP began falling in mid ’73 and by ’74 we were in recession. So, a casual observer would say NGDP path targeting doesn’t work that time. I raised this issue once before and Dr. Sumner was kind enough to reply that wage and price controls were the problem. But, those controls were gone by early ’74 and in any event what would have been the clue in ’73 -’74 that the nice stable path of NGDP wasn’t doing it’s job? It can’t be the jump in inflation because MMs have been arguing for higher inflation targets if that’s what it takes to keep NGDP on the desired path. And it can’t be the ‘stance’ of monetary policy as measured by interest rates. If MMs try to claim you can judge the stance of monetary policy based on interest rates they will get both barrels from Bob Murphy.

Comments:

1. Let me know when Bob Murphy finds an actual contradiction in my blogging.

2. It’s not quite true that NGDP growth was stable during 1972-76:

NGDP growth did slow in 1974. But out of respect for our nation’s military, I’ll concede to the Captain that the NGDP growth rate during this period (a bit over 8%) was high enough so that we really should not have had a severe recession in 1974. In this case, we do need to look beyond NGDP.

The musical chairs model suggests that it’s the interaction of NGDP and wages that determines the business cycle. Normally, wage growth falls during recessions. Indeed it almost always falls, or at worst is relatively stable. But not in 1974—for some strange reason wage growth shot up during 1974, despite rising unemployment. Why? What’s wrong with the model?

Those who have read my book on the Great Depression (The Midas Paradox) know that I argued that five autonomous wage shocks slowed the recovery during the New Deal. In 1974, there was no explicit government program to boost wages, as there had been during the Depression. But there was a removal of the wage controls that Nixon had imposed in 1971.

Although these were called “wage and price controls”, they were actually all about holding down wage growth. The price controls were the price they had to pay to get Big Labor to go along. Then the Fed juiced NGDP growth, and the combination of fast NGDP growth and slow wage growth created a boom, and Nixon’s 49 state landslide victory in 1972.

But there was a price to be paid for this recklessness. The removal of the wage controls led to fast wage increases. At the same time the Fed was trying to slow inflation, which had shot up from a combination of fast NGDP growth, removal of price controls, and a major oil shock after the 1973 Arab-Israeli War. A perfect storm of bad policy and bad luck came together to produce a modest slowdown in NGDP growth and a sudden rise in wage growth—a toxic combination for the economy.

I do think NGDP by itself is a pretty good model of the business cycle. But it’s not perfect. Recessions can also be caused by real shocks, especially policies that distort the labor market. The slow recovery after July 1933 was one example, and the steep 1974 recession was another.

READER COMMENTS

Andrew_FL

Dec 7 2016 at 1:52am

Lifting a price ceiling should not cause quantity exchanged to go down

AntiSchiff

Dec 7 2016 at 8:48am

Andrew_FL,

A wage shock involving spiking real wages should cause unemployment, ceteris paribus, which mean a slowdown or outright contraction in output.

Scott Sumner

Dec 7 2016 at 9:16am

Andrew, It depends on the nature of the labor market. if lots of workers are paid more than their reservation wage (and they were back in 1974), it may well cause a drop in employment, especially when combined with a slowdown in NGDP growth.

Capt. J Parker

Dec 7 2016 at 5:29pm

When you differentiate a time series you amplify a lot of noise. I think I can often see more by plotting things on a log scale where series with a constant rate of compounded grow appear as straight lines whose slope is proportional to the growth rate. Here is a plot of NGDP, RDGP and average hourly wages on a log scale. (with some scale factor tweaking so the lines are easy to compare.)

Looking at this graph:

1) NGDP growth looks pretty linear with a steady NGDP annual growth rate of 10%. I do admit that it looks like the growth rate softened just a bit during the ’74 recession.

2) Average hourly wage does bump up about half way through the ’74 recession. But,

3) RGDP stopped moving with NGDP well before the bump in wages so, the ’74 wage shock doesn’t look like the cause of the 74 recession. It might have prolonged the recession but it’s not what kicked off.

Whether the cause of the ’74 recessions was labor price shock or an oil price shock or a negative supply shock caused but price controls the question that interests me is: could the recession have been prevented and what would the intervention need to have looked like. Should Burns actually have been doing more monetary stimulus to counter the slight softening in NGDP growth? Or, is this an Austrian lesson about once you have too big a (pick your favorite: supply shock, inflation rate, government thumb on the market pricing scale) there is nothing you can do to prevent a spike in unemployment?

Jim Glass

Dec 8 2016 at 11:04am

Not a word about the oil price shock, as the price of oil more than tripled though 1973 into 1974, with the accompanying stock market 45% plunge?

I’ve often heard the oil price shocks cited as the cause of the rise of inflation during the 1973-81 period — which is easy to refute by noting the simultaneous steady inflation in Germany and falling inflation in Japan, corresponding with different monetary policies.

But a sudden tripling of oil prices is a significant shock to the real economy, and the expected effect on the real economy would seem to have been reflected as it happened in the stock market.

(I lived through all that, and in fact was taking economics at NYU-Stern with professors from across the street at the NY Fed, and *they* certainly thought the oil price shock was a serious hit to the real economy.)

It’s a big thing to ignore, and would seem to worth at least a word — if only to debunk the notion.

Jim Glass

Dec 8 2016 at 11:30am

I’ll add that the 1974 recession was global, so it hardly seems likely to have been caused by domestic US policies. The effect of a tripling of oil prices, otoh…

It’s a funny thing to me. In 2008 everyone was screaming about the price of oil going up over $100 heading to $200, in the press there were daily damnations of “speculators” and hoarders driving up the price, oil companies manipulating up the price, Congressional and govt investigations of same, doomsday alarms of peak oil having arrived … check the headlines from back then, the banking system was a much more minor issue and deemed under control. (Google Krugman’s columns from 2008, and you’ll find one after another on oil prices, not much on banks.)

Now, a mere eight years later, the Banking Crisis is universally deemed the cause of the recession, and oil as a trigger is completely forgotten by everyone (who hasn’t read the Fed’s minutes of the day).

And the Banking Crisis was caused by the home price explosion, which was caused by the Greenspan Fed’s irresponsibly easy money policy and/or the US govt’s regulators, etc, even though it was a global phenomenon that could hardly have been caused by US domestic policy…

But I digress.

Mark Cancellieri

Dec 8 2016 at 1:00pm

Jim Glass,

Perhaps the rise in oil prices *was* caused by domestic US policies.

Black Gold: The End of Bretton Woods and the Oil-Price Shocks of the 1970s

However, I’m always willing to listen to counterarguments.

Jim Glass

Dec 8 2016 at 7:31pm

“Not a word about oil…?”

Re-reading I see that the words “oil shock” do appear once in the penultimate paragraph.

My bad for saying otherwise. Negligent reading on my part. Apologies.

But given the big difference in weight given to the other domestic policy factors throughout the post versus the nine short words given to oil at the end, I’ll stick with the substance of my comment.

I have a hard time seeing how the end of wage & price controls, surely a beneficial economic event overall, would drive the stock market down 45%.

Capt. J Parker

Dec 9 2016 at 11:58am

Here’s oil price and Real GDP on the same graph. Real GDP was softening before the ’73 oil price shock so I doesn’t appear that oil shocks were the cause of the 74 recession. Might have prolonged and deepened it but, not what kicked it off IMHO.

Comments are closed.