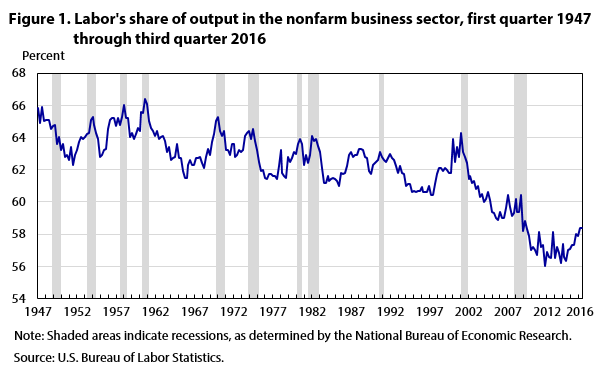

One of the most striking and troubling patterns in the US economy in recent decades is the “declining labor share: that is, the pattern that the share of the value of output (in the nonfarm business sector) that goes to workers in the form of compensation, which includes benefits as well as wage and salary compensation, has been dropping. The labor share was typically in the range of 63-65% from the 1950s into the early 1970s. By the 1980s and 1990s, it was more often falling in the range of 61-63%. In the early 2000s, it fell below 60%, and since the end of the Great Recession in 2009 it has typically been between 56-58%.

This is the opening paragraph of Timothy Taylor’s excellent post “The Declining US Labor Share, Explicated,” Conversable Economist, February 27, 2017.

Timothy goes on to summarize a Bureau of Labor Statistics article by Michael D. Giandrea and Shawn A. Sprague in the February 2017 issue of the Monthly Labor Review.

Here’s the section of Timothy’s post that I found most interesting:

The underlying assumptions about “proprietor income” are biasing the labor share calculations.

The calculation of labor share involve adding compensation received by employees to “proprietor income,” which is the labor income received by those who run their own business. However, proprietor income is conceptually tough to measure, because someone who owns their own business can receive both “labor income,” as if the person was an employee of their own business, and “capital income,” as the owner of the business. In the real world, these two types of payments are jumbled together. To address this issue, the Bureau of Labor Statistics has assumed that the hourly labor compensation of proprietors is the same as that of employees. However, if the labor income of proprietors is actually rising over time, then this assumption means that the labor share is understated. One study finds that about one-third of the observed decline in labor share is due to this assumption that the hourly labor compensation of proprietors is the same as that of employees, rather than using an alternative method that tries to estimate the capital income of proprietors directly. (bold and italics in original)

READER COMMENTS

Andrew_FL

Feb 27 2017 at 9:34pm

Huh, almost every recession has been preceded by or concurrent with a spike in the labor share. Interesting.

Nikolas

Feb 28 2017 at 2:49am

Is this bias time variant?

Tim Worstall

Feb 28 2017 at 6:07am

I’ve always been puzzled by the American calculations of the labour share. Because to my mind it’s done the wrong way. Part of it is as above. Allocating that mixed income across the labour and capital shares. The UK stats (and thus all EU ones, all must report the same way) list four portions. Capital share, labour, mixed income and taxes on consumption and subsidies to production as the fourth.

When broken out this way it’s possible to see, for the UK figures, what has been happening. Yes, a decline in the labour share over the decades. But not a rise in the capital share. Rather, mixed income has risen a bit as there are more self employed people. But what has really made the difference is that taxes upon consumption have risen. VAT in fact which has more than doubled since inception in the mid 1970s. It’s more than a few percentage points of GDP as well.

My intuition (and most certainly not one I’ve the chops to be able to prove) is that if we reported the US figures the same way then we’d see something similar. Sales tax rates have certainly risen in some places over those decades for example. The move from C to S corporations will have made a difference to the mixed income numbers. It wouldn’t surprise me at all to find we get the same as the British result although I don’t insist that we would. Which is a fall in the labour share but not a rise in the capital, the fall being explained by the other two parts instead.

And I’d be fascinated to see the results of someone managing to find the numbers to test that.

David R. Henderson

Feb 28 2017 at 8:25am

@Nikolas,

Is the bias time variant?

Yes. See my earlier post on this.

Thaomas

Feb 28 2017 at 11:49am

It’s an interesting problem but I do not think it is very important for designing a first best solution: higher taxes on high incomes (or better still, high consumption) and lower taxes on low incomes (e.g. eliminating the wage tax “financing” Social Security and Medicare) and using the money for redistribution in kind — low premium health insurance, subsidized day care and child services — and wage subsidies like a much higher Earned Income Tax Credit. Only if these are blocked do we have to worry about whether it is technology or trade or demand shifts in order to design minimum cost second/third/fourth best policies.

Comments are closed.