I’m seeing two common mistakes by commenters trying to analyze the Brexit vote shock:

1. Assuming that monetary offset applies to real shocks

2. Assuming that a cut in the BOE’s target interest rate represents an easing of policy.

It turns out that these two errors are interrelated. The Bank of England has a dual mandate, which includes 2% inflation in the long run, but macroeconomic stability in the short run. It’s probably easiest to view this as keeping NGDP growth steady in the short run, but gradually nudging it up or down in the long run to keep inflation close to 2%.

To make things simple, let’s define AD as a given level of NGDP. Then the BOE wants stable growth in AD, at roughly 4%/year. Now suppose there is a nominal shock. In that case, the BOE should adjust policy to keep NGDP growth stable. If we use the Equation of Exchange:

MV = PY

You can think of that as the central bank adjusting M to offset changes in V. If you prefer a Keynesian approach, you can define the Wicksellian equilibrium interest rate as the rate that keeps NGDP growth at about 4%. If the Wicksellian rate falls (as it did after Brexit) the BOE will cut the policy rate, to keep growth in NGDP stable.

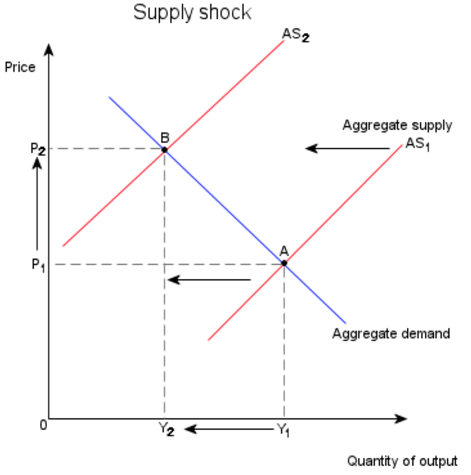

But monetary offset does not apply to real shocks:

When the AS curve shifts left, the BOE will keep monetary policy stable by keeping the AD curve stable (more precisely the growth rate is kept stable.) So real shocks will reduce RGDP, even if monetary policy is fully offsetting shocks that might impact AD. Monetary offset is a useful concept, but can only do so much.

I think people tend to overrate the importance of central banks in setting interest rates. The BOE is constrained by its macro targets. Thus 90% of the time when it adjusts interest rates it’s not a true policy change, it’s just the central bank reflecting a change in the Wicksellian rate caused by some sort of shock. It looks like the central bank is what’s causing rates to change, but that’s a cognitive illusion.

As an analogy, a bus driver will adjust the steering wheel on a twisty road. Superficially it looks like the bus is moving around at the whims of the driver. But a deeper explanation is that the path of the bus reflects the shape of the road, and the driver simply adjusts the steering to keep the bus centered on the road. A true change in “bus driver policy” would be a change in steering that drove the bus off the road.

Central banks mostly adjust rates passively to accommodate changes in the economic road ahead. Occasionally they do something wild and crazy, like not adjust the interest rate to changes in the Wicksellian equilibrium rate. How do we know when that happens? The economy goes off the road. NGDP goes wildly up or down. The last good example was in 2008, when rates were cut too slowly. Another example is the 1970s, when rates were raised too slowly.

When big mistakes are made, the problem is almost always “rates adjusted too slowly.”

READER COMMENTS

James Alexander

Feb 5 2017 at 4:14pm

Scott Sumner law #1

The stance of monetary policy is shown by expectations for NGDP growth.

NGDP growth expectations in the U.K. remained stable post the vote and, in fact, NGDP growth has accelerated since the vote. RGDP has remained steady despite initial fears for RGDP.

Why?,Because NGDP growth has risen. Domestic demand has been stimulated to offset those RGDP fears.

Are those fears real, Real, nominal, or just debatable? Does it matter?

Matthew Moore

Feb 5 2017 at 4:27pm

Only tangentially related…

@Scott: what real outcomes (not institutional) would convince you that Brexit was actually the better option?

James Alexander

Feb 5 2017 at 4:46pm

Or. Simply. The devaluation shifts the AD curve to the right.

Scott Sumner

Feb 5 2017 at 8:35pm

James, Too soon to say NGDP growth has accelerated since the Brexit vote. We need more data. I don’t think it has accelerated.

Basically I don’t think the Brexit vote affected AS or AD, at least I see no firm evidence of such an effect.

Matthew, A very good trade deal with the EU plus continued high rates of immigration into the UK.

Alternatively, if RGDP growth after 2019 kept up at the same pace, that would suggest it was probably a good move.

Matthew Moore

Feb 6 2017 at 9:00am

Thanks for the clear answer.

James Alexander

Feb 6 2017 at 9:47am

Scott

Facts are facts. You may not like ’em, but …

http://ngdp-advisers.com/2017/01/26/uk-nominal-gdp-growth-jumps-even-post-brexit-vote-thought/

bill

Feb 6 2017 at 10:07am

@”rates adjusted too slowly”

You mean that when Lehman failed, the bus drivers should have turned the steering wheel more than zero degrees?

[Sarcasm] 😉

TMC

Feb 6 2017 at 11:16am

High rates of immigration is what Brexit is trying to avoid. This has been a net negative to the UK. At least now they can continue to allow in high quality immigrants, but filter the lower quality. It’s not the wild west anymore, when you could allow immigrants to sink or swim. Maybe the question should have been “..would convince you that Brexit was actually the better option for the UK?”

Scott Sumner

Feb 6 2017 at 2:47pm

James, The 4th quarter NGDP data is not even out, and Fred shows NGDP growth slowing in Q3. So no, “facts” are not facts. Facts require interpretation.

https://fred.stlouisfed.org/series/UKNGDP

Bill, Well put.

TMC, I believe immigration is a good thing for the UK.

James Alexander

Feb 6 2017 at 4:50pm

1. I think your data link needs refreshing. 2016Q3 accelerated to YoY 4.0% from 3.1% in 2016Q2.

(Perhaps you are looking, American-style, at 4x the QoQ rate, which did indeed decelerate.)

2. NGVA has proven an excellent proxy for NGDP, it is NGDP less taxes, and has the huge advantage that it comes out with the first estimate of RGDP. It continued the recovery in YoY nominal growth post-Brexit.

Scott Sumner

Feb 7 2017 at 9:24am

James, When you do at an event study, the last thing you want to use is YoY data, 3/4ths of which comes before the event!

You use actual quarterly change, which is what I did. Let’s wait until we have 12 months of actual NGDP data, not guesses based on other data. Then make a judgment.

And BTW, NGVA is not an excellent proxy for NGDP, I’ve seen both data series.

So far, NGDP growth has not accelerated.

ChrisA

Feb 7 2017 at 12:53pm

Scott, guilty as charged. But I think the mistake you are making is that the BOE is actually holding to their inflation target. I think they are communicating, via their interest rate reduction, a willingness to tolerate higher inflation than otherwise. So the market is assuming accelerating NGDP growth. Of course any CB indicating a willingness to have higher NGDP growth than previously should expect a depreciating currency.

Rajat

Feb 9 2017 at 4:59pm

Scott, I know you wanted to keep things simple, but (as you’ve said before) to make the diagram work, doesn’t AD need to be a rectangular hyperbola (1/NDP)?

Lorenzo from Oz

Feb 9 2017 at 5:32pm

Not sure “immigration is good for the UK” can be quite so baldly stated. The combination of immigration and land rationing is not doing good things for a lot of Brits.

http://www.businessinsider.com/inequality-class-britain-property-ownership-workers-income-poorer-2017-2?IR=T

Comments are closed.