As I write this post, Australia just announced 1.1% RGDP in the fourth quarter, and 2.4% over the past 12 months, both higher than expected. Thus once again the “Lucky Country” dodged a recession (GDP had fallen 0.5% in the third quarter.)

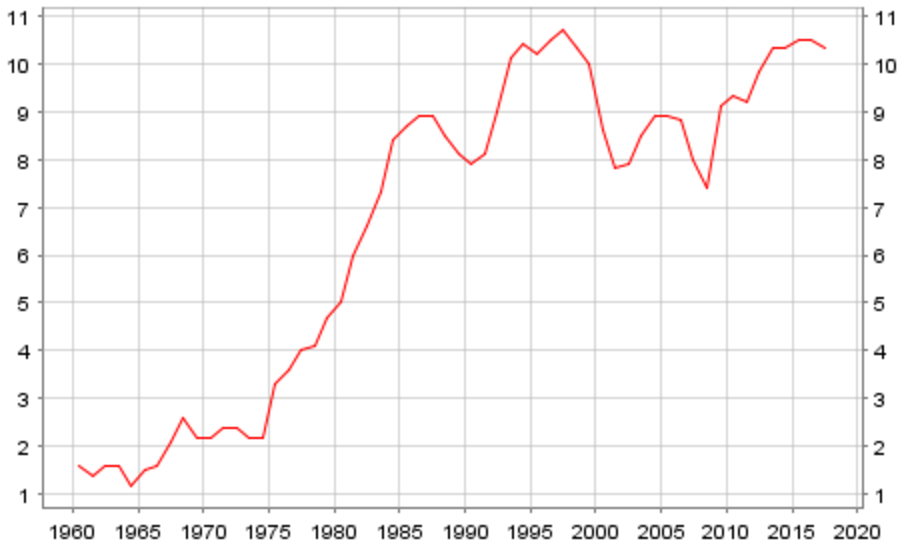

It seems pretty likely than in two more quarters Australia will beat the record for the world’s longest expansion, currently held by the Netherlands (103 quarters, or almost 26 years.) When I saw the list of the longest economic expansions, I was struck by number four on the list, France, from 1975-92, a total of 68 quarters. Younger readers might not understand why I was surprised by this expansion. Take a look at the French unemployment rate since 1960:

How can this be? It looks to me like French unemployment was about 3.5% at the end of the 1975 recession, and then rose at about 0.5% per year, up to 9% in 1986. How can rising unemployment occur during a record expansion?

Here’s the French RGDP growth rate:

Here’s what I think happened. Between 1960 and 1986, France became considerably more socialist, particularly in terms of taxes, benefits and labor market regulations. As a result, the French natural rate of unemployment rose from about 2% to about 9%, where it has remained (more or less) ever since.

A rise in the natural rate of unemployment is not (necessarily) a recession. A recession is probably best thought of as a period when the actual rate of unemployment rises sharply above the natural rate.

Although Australia has had an impressive expansion, it does still have an unemployment rate of 5.7%, considerably higher than the US rate, and almost double the 3.1% rate in Japan. Unlike Australia, Japan has so-called “recessions” quite frequently. That’s because Japan’s working age population is falling at more than 1% per year. So their trend RGDP growth rate is barely above zero. Statistically insignificant fluctuations in Japanese RGDP can create 2 consecutive quarters of falling RGDP.

I encourage people to keep the following things in mind:

1. Unemployment fluctuates with the business cycle, and also with changes in the natural rate of unemployment. The natural rate of unemployment tends to be higher in more regulated labor markets, such as southern Europe, and tends to be lower in less regulated areas, such as Hong Kong. In order to ascertain whether rising unemployment is due to a (demand-side) recession, look to see if there is a slowdown in hourly nominal wage growth. If not, then the natural rate of unemployment may be rising. In addition, look to see if unemployment starts falling once the recession ends. If not, then the natural rate of unemployment has risen.

2. Don’t pay too much attention to “technical recessions”, with two consecutive quarters of falling RGDP. In a slow growth world, these may become more frequent. But in cases like Japan where the negative growth is not accompanied by rising unemployment, it’s not a true business cycle.

3. Learn from Australia. Right now, monetary policy in Australia is probably too tight. They are undershooting their targets. They are coasting on their past successes. Fortunately, their past successes gave them enough flexibility so that a mild undershoot didn’t lead to recession in 2016.

4. Countries will occasionally abandon policies that were wildly successful. The current head of Australia’s central bank is one example:

You might think a central bank looking at inflation significantly below its target, a relatively weak jobs market, and a policy interest rate well above zero would be keen on loosening up. In the case of Australia, however, you would be wrong.

A recent speech by Philip Lowe, who runs the Reserve Bank of Australia, explains why: monetary policy has to be focused on long-term economic stability, even if that means acting against what conventional indicators might suggest. The inflation target is more what you’d call guidelines than actual rules. If the choice were between a) having consumer prices rise a little more slowly than target and unemployment at the upper end of its range or b) encouraging a debt-fuelled boom with excessively low interest rates, the RBA would go with option A.

Germany’s Social Democratic Party introduced a major set of labor market reforms in 2004, which turned out to be one of the most successful reform packages in modern history. It was almost a mirror image of France in the 1975-86 period, as the Germany natural rate of unemployment plunged much lower. And now the new leader of the SDP wants to reverse these reforms. Sad!

READER COMMENTS

Daniel Hill

Mar 1 2017 at 5:44pm

The case of Japan is just one example of why talking about changes in GDP (or RGDP) rather than changes in GDP per capita is meaningless. If the fall in Japanese GDP is smaller than the fall in the population, GDP per capita is actually growing.

Scott Sumner

Mar 1 2017 at 6:26pm

Daniel, Good point.

Andrew_FL

Mar 1 2017 at 9:08pm

Average of annualized MoM growth rates of FRED series AHETPI 1. In the 12 months immediately preceding a recession (labeled by year of the starting month) and 2. During the duration of the recession itself

1970: 1. 6.1% 2. 5.7%

1973: 1. 6.3% 2. 7.6%

1980: 1. 7.1% 2. 9.1%

1981: 1. 8.8% 2. 5.3%

1990: 1. 4.1% 2. 2.8%

2001: 1. 4.2% 2. 3.1%

2007: 1. 3.8% 2. 3.3%

Next I first take FRED series M0861BUSM324NNBR, M0861CUSM336NNBR, & M0861DUSM346NNBR. I take YoY growth rates for the three, average them, and then use these to extend M0861DUSM346NNBR backwards.

Now, as above:

1913: 1. 7.1% 2. 4.9%

1918: 1. 33.2% 2. 12.9%

1920: 1. 23.5% 2. -1.0%

1923: 1. 9.2% 2. 3.9%

1926: 1. 2.6% 2. 0.3%

1929: 1. 1.8% 2. -6.1%

1937: 1. 8.96% 2. 2.93%

1945: 1. 4.4% 2. 1.3%

1948: 1. 7.2% 2. 2.8%

Unfortunately I can’t find a comparable broad wage series spanning 1949-1964.

At any rate it appears that what you say is usually, though not always true.

Kevin Erdmann

Mar 1 2017 at 10:07pm

The “debt-fueled boom” he refers to is urban housing. I’m not sure how all the central bankers know that it is “debt-fueled”, since any rise in home prices is bound to include rising debt levels. In places where real home prices have doubled or more, like in Closed Access America and in Australia, interest rates can explain about 20% of it, and urban politics explains the rest. (Actually, the rates that central banks control explain roughly 0% of it.) So, we kill our economies to avoid a non-existent “debt-fueled boom”.

This is what I mean by my analogy of a forest fire, Scott. Urban planners are running through the forest with flamethrowers, and central bankers arrive on the scene, and promise that we should be able to get this fire under control once we kill off all the oxygen-supplying plankton.

The research is unimpeachable. Plankton creates oxygen and oxygen causes fires. The connection is quite clear. And, to give them their due, given that it is the central bank’s job to control prices via oxygen levels, we could hardly expect any less.

Brett

Mar 1 2017 at 11:51pm

The Mitterand government in France back-tracked on a lot of the socialist reforms and widespread nationalizations they implemented in the early 1980s within a year or so (and more – they did massive restructuring and layoffs at the nationalized firms before re-privatizing them). That might have been enough to save France from going negative on GDP growth.

Rajat

Mar 2 2017 at 7:50am

Scott, you’ve said that the Fed basically does what the consensus of macroeconomists think it should do. In Australia, we don’t have a community of proper (PhD-trained) macroeconomic commentators. Nevertheless, I think the same principle applies – most macro commentators think the RBA is being sensible by not lowering interest rates further. They all have in their heads that higher house prices imply greater risk of a financial crisis. Hence, many support Lowe’s stance. Talk about sad…

Luis Pedro Coelho

Mar 2 2017 at 8:02am

A difference in the German case when compared to the Australian one is that in Germany, the labor market reforms were never very popular and have perhaps only gotten more so now that there is less urgency. Mr Schultz is a politician and politicians get elected by saying popular things. Bashing Hartz IV is popular.

In the Australian case, it seems it’s technocrats who are backing away from a working system when they should know better. I do not know a lot about Australian politics, but I doubt this is being talked about all over the media. I would be surprised if Mr Lowe is a darling of the right like Mr Schultz has become a darling of the European left.

Bill Woolsey

Mar 2 2017 at 8:14am

I don’t think low interest rates, too much debt, speculative boom, is a good way for central bankers to think about things, but we should also keep in mind that one reason why inflation targeting is a bad idea is that consumer prices in general and the implicit rental portion of them is not a good proxy for monetary disequilibrium (or disturbance.) What is happening to housing prices should be taken into account, along with all the other capital goods. Of course, some measure of spending on output, like NGDP, is the way to go, rather than any measure of inflation.

Plucky

Mar 2 2017 at 10:24am

an odd/random q I’ve had- what evidence is there for (or against) recognizable business cycles before the industrial revolution? On the time-scales we’re used to, it’s basically a world of flat population and infintisimal productivity growth.

dd0000

Mar 2 2017 at 12:42pm

The data on France is a bit misleading. Unemployment is so high because the incentives to register as unemployed are much higher.

Per OECD metrics, labor force participation for 25-52 year old’s is actually *higher* in France than in the US (though lower for 15-24 year old’s and MUCH lower for 65+ where the French basically don’t work at all).

dd0000

Mar 2 2017 at 1:31pm

Also – if the OECD data is correct – the Netherlands and Spain (!) have seen two of the greatest economic performances in history, raising their 25-54 yo labor force participation rates from ~60% in the 70’s to ~87% in 2015.

I’m not really sure what to make of that.

https://data.oecd.org/emp/labour-force-participation-rate.htm

Scott Sumner

Mar 2 2017 at 2:23pm

Thanks Andrew, that may be worth a post. The two exceptions are widely viewed as “supply-side” recessions.

Kevin, When central bankers blame factors such as too much debt for macro disequilibrium, they are usually diverting attention from monetary policy mistakes.

Brett, Good point.

Rajat, I agree. Fortunately the RBA’s 2% to 3% inflation target gives them a bit more room. Mistakes are not as consequential as in Europe.

Bill, I agree. Note that NGDP growth in Australia has also slowed recently.

Plucky, I don’t know. I’d guess agriculture was a big factor back then.

dd0000, Interesting.

dd0000

Mar 2 2017 at 4:02pm

Scott – looking at the OECD data again, Spain’s employment rate for 25-54 year old’s is actually *lower* than its labor participation rate (as is the case in a few other countries per the data) – I don’t understand how this is possible.

Thaomas

Mar 2 2017 at 4:57pm

@ Kevin Erdmann,

But central banks are not charged with controlling inflation with interest rates (if I understand your metaphor); they are charged with controlling the price level trend and the employment level with any and all the instruments they can lay their hands on.

Kevin Erdmann

Mar 2 2017 at 6:34pm

Thaomas, they seem to think it’s the interest rate. In any case, it seems clear to me that part of what characterizes the current era is that Anglosphere countries have developed an urban housing supply problem and that this has shaded central banks to more hawkish positions, because they are constantly bombarded with complaints that they are inciting bubbles.

Lorenzo from Oz

Mar 3 2017 at 5:55pm

What Kevin Erdmann said, again.

Comments are closed.