There’s an unfortunate tendency for economists to align themselves into “supply-side” and “demand-side” camps. Many conservatives in Europe denied that the ECB’s tight money policy caused a double-dip recession, leading to a dramatic rise in unemployment between 2008 and 2013. Indeed conservative Eurozone policymakers caused that recession.

On the other hand, many demand-siders go too far, ignoring the fact that the relative performance of individual countries within the Eurozone reflects supply-side factors. Greece and Spain would have been better off never having joined the Eurozone. But given that they did so, they should have tried to make the best of it by adopting labor market reforms to make their economies more flexible, and austere fiscal policies with budget surpluses. Greece and Spain both had very poor labor market policies, and Greece had almost unbelievably reckless fiscal policies.

The Financial Times reports that Spain has recently been growing rapidly, after adopting some unpopular economic reforms:

For some, not least the Spanish government and Europe’s political establishment, this is a moment of relief and vindication. In their view, the recovery of the eurozone’s fourth-largest economy shows that the unpopular policies pushed through at the height of the crisis worked. Despite causing initial pain, Spain’s decision to reform the labour market, overhaul the banking system and cut the deficit paved the way for a return to growth. It is a message Madrid would like to resonate beyond Spain’s borders: countries can reform their way out of an economic crisis, even while being locked into the single currency.

There is, however, another view. Critics, mainly from the left but also from parts of academia, argue that the country’s recovery is not just incomplete but that the price of austerity and reform was too high. The unemployment rate may have fallen sharply, but at 18.6 per cent it remains far above the pre-crisis level and almost double the eurozone average. Ms Oltra is one of many who bemoans the creation of a new class of “working poor” in Spain. Inequality has increased dramatically and public finances continue to bear the scars of the crisis: Spanish government debt is 100 per cent of GDP, up from 40 per cent before the crisis.

Here it is important to avoid “mood affiliation”. My views are much closer to the first paragraph than the second, even though the people making that argument are to a large extent the same people who caused the Eurozone crisis, which imposed so much misery on the Greek and Spanish public. But on this particular issue they are correct, supply-side reforms are the key, once you’ve ruled out leaving the Eurozone.

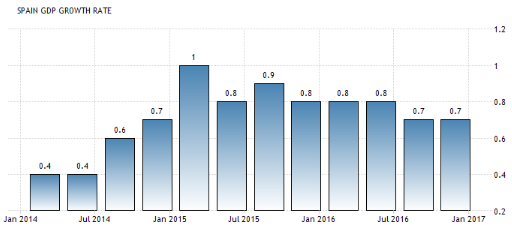

Let’s start with a comparison of growth rates. Here are the quarterly growth rates in recent years in Spain. (If you are an American, it helps to multiply by 4 to annualize the rates.)

Compare that the Greece, which is just treading water:

But what about Spain’s 18.6% unemployment rate? There’s no denying the fact that unemployment remains a huge problem in Spain. But it’s also important to note two other facts. First, just a few years ago it was over 26%. Second, Spain has a very high natural rate of unemployment. Since 1980, their unemployment rate has fluctuated between about 10% during booms and 20% to 25% during recessions—even garden-variety recessions that are much milder than the Great Recession.

Thus an 18.6% unemployment rate in Spain is not nearly as horrific as the same rate would be in the US or Japan.

Finally, the creation of a “new class of working poor” should be viewed as a policy success. To see why, just look at the huge class of poor in Greece, who are not working at all.

PS. In my view the ECB should adopt more expansionary monetary policy as well. This post is looking at options from the perspective of individual Eurozone members.

READER COMMENTS

Thaomas

Apr 9 2017 at 4:41pm

I think this either or fallacy is also the case among “demand sliders.” Neo-Keynesians neglected beating up on the Fed for failing to maintain NGDP growth (or even price level growth while Market Monetarists neglect beating up on the Federal Government for failing to increase spending on projects with positive NPVs.

Meets

Apr 9 2017 at 5:20pm

The Paleo Keynesians are not gonna be happy

Biopolitical

Apr 9 2017 at 6:16pm

The labor reforms in Spain were slight and are probably having only a small role in the recovery of employment. Employment is going up just like it did after other past recessions, regardless of labor reforms. Given how awful Spanish labor laws still are, unemployment will remain one of the highest in the world.

To look tough before their voters when they were negotiating the Spain’s bailout, European politicians required Spain to pass labor reforms. Unfortunately, cosmetic reforms were good enough for that goal.

bill

Apr 9 2017 at 7:40pm

@Thaomas,

I agree with your premise – that the gov’t should undertake positive NPV projects. However, many pieces I’ve seen written by Keynesians seem to ignore repayment of principal (I’m not accusing you of this; I’m just noting it). They imply that if the interest rate is zero, then almost everything makes sense. But if a capital project costs $100 and has an expected life of 25 years, it has to provide an annual benefit of $4 to be a breakeven if it’s financed with zero interest costs. Then in real life, things get more complicated, like is the expected life 20 years vs 30 years, or if the benefits are fuzzier to measure, etc. Add to that, much infrastructure will just facilitate the burning of more carbon based fuels.

Scott Sumner

Apr 9 2017 at 9:00pm

Thaomas, You said:

“Market Monetarists neglect beating up on the Federal Government for failing to increase spending on projects with positive NPVs.”

That’s an odd comment. I don’t think MMs are opposed to projects with a positive NPV, but I also don’t have any expertise in determining exactly which projects those are. So why would I “beat up” on an issue that’s not in my area of expertise?

Biopolitical, Any thoughts on why Spain is recovering much faster than Greece?

Thaomas

Apr 9 2017 at 10:27pm

Scott,

I do not think MM’s should identify which projects pass the NPV test or which one pass when there is unemployent of factors of production (MC is less than P) of inputs and the real interest rate has declined during a recession (and while a central bank has not yet restored NGDP to its target path). But there ought to be more such projects than when there is full employment (MC=P) and interest rates are “normal.” And deficit finance investment in such projects ought to be part of the MM prescription just as is restoration of NGDP to target level is.

Scott Sumner

Apr 10 2017 at 3:57pm

Thoamas, You said:

“But there ought to be more such projects than when there is full employment (MC=P) and interest rates are “normal.””

That’s reasoning from a price change. It depends why rates are low. Maybe they are low because there aren’t many good investment projects out there.

Karl

Apr 11 2017 at 6:37pm

Economists forgetting how to optimize.

Thaomas

Apr 12 2017 at 10:20am

Scott,

Sorry, I thought the context made it clear that I was referring made the comment in the context of a fall in inter to a recession and the central bank has reduced interest rates.

However, governments should definitely “reason from a price (including shadow price) change” about whether and when to undertake investments — anything with near term costs and longer term benefits. If prices (or marginal costs in the case of sticky prices) of some of the inputs to an investment project – labor, capital, real estate, agricultural land, whatever — have declined relative to the benefits — certainly likely unless one thinks the recession will last forever — that should mean that governments would increase investment.

The lager point is that governments should be using the NPV rule recession or no recession and NOT reduce investment because the deficit increases during a recession. Doing so will, to those whose main interest is reducing the size of the state, look like and be denounced as “Keynesian” “fiscal stimulus.” Austerity would be “reasoning from a deficit change” and I can’t think of any mode in which that is the correct decision rule.

Comments are closed.