I frequently argue that income is a meaningless concept, as it includes capital gains (and losses) in asset values. Indeed the problem is even more basic, as income mixes labor income and all investment income, which is like adding apples and oranges. No, it’s even worse, like adding strawberries and watermelons, and talking about the number of “fruit”.

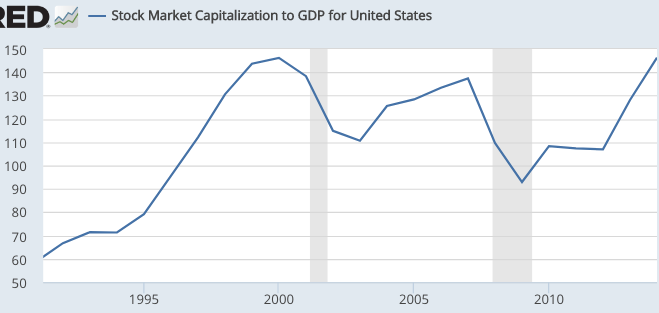

Because income is a meaningless concept, income inequality is also meaningless. But let’s say I’m wrong, and let’s assume that capital income actually measures something interesting. What then? In that case, the income of the top quintile would almost certainly be highly cyclical. Consider the following graph, showing the total stock market capitalization in the US:

Notice that stock market capitalization fell by 23.4% of GDP between 2001 and 2002, and by 44.5% of GDP between 2007 and 2009. What happens when stock market capitalization falls by nearly a quarter?

Let’s consider the top quintile of the population, which owns the vast majority of stocks. Capital losses of 23% of GDP would sharply cut into their income from other sources. The top quintile earns about 55% of total income, or 43% after taxes and transfers. If the income inequality data were accurate, it should show a huge drop in the share of income earned by the top quintile, any time the stock market crashed. But we don’t see that—income shares are pretty stable from year to year.

The problem here is that while income proponents claim to care about capital gains and losses, what they actually measure is realized capital gains and losses, which is meaninglessness on steroids. It takes an already meaningless concept (capital gains) and only counts those amounts that show up on tax returns when people buy and sell stock. Economists agree that there is no functional difference between a realized capital gain and an unrealized gain, indeed realized gains often are not even consumed, rather simply reinvested in another financial asset!

If you really believe that we should be measuring capital gains, and including them in with income, then we ought to include the unrealized gains as well. If we did that, we would observe massive declines in the income of the top 20% in bear markets like 2001-02 and 2007-09. Do you recall Americans basking in the glow of a dramatic improvement in “equality” in 2009? Neither do I. And that’s because its consumption inequality that matters, and consumption inequality did not change dramatically during the Great Recession.

A few points on the data:

1. Foreigners own a portion of the American stock market. However, Americans own lots of foreign stocks as well. Since foreign markets crashed at about the same time, I think these are still ballpark estimates of capital losses for Americans from the bear market in stocks.

2. During 2007-09, the top 20% also saw large capital losses in real estate. Thus the data above understates the total capital losses incurred by the elites in 2007-09. It would not surprise me if total income earned by the top 1%, or perhaps the top 0.1%, actually turned negative during 2008. (It did for me.) That is, their capital losses outweighed labor income plus interest and dividends. But obviously it would be silly to include the top 1% in with homeless people in income inequality data. It’s consumption that matters.

3. Conversely, huge gains also distort the picture. When I file taxes next year I’ll have to report a huge capital gain, as I am selling my house for about a million dollars more than I paid for it. And yet nothing really changed for me this year. I am buying another house of roughly equal value. Nothing has changed in terms of my flow of housing consumption; I occupy the exact same number of square feet as when I bought the house in 1991. It’s all just housing inflation, which in coastal areas has outpaced the CPI.

This is not to say that I am not in some sense “rich”, or deserve to pay lots of taxes. I could choose to live in a cheaper area, and have lots of money left over. By global standards I’m extremely rich, and even by American standards I’m upper middle class. But the income I report on my tax return next April won’t accurately portray my economic circumstances. I’m affluent, but not as affluent as someone who made my combined wage and capital gains income, all in the form of wage income from a single job. There’s a reason that 73% of Americans spend at least part of their life in the top quintile–incomes are volatile.

Here’s one estimate of income (after taxes) and consumption inequality:

I suspect that inequality in real terms would be less than inequality in nominal terms (shown above), as the affluent tend to live in high cost areas. That’s not to deny that there would still be plenty of consumption inequality. There is. And I also suspect that consumption inequality is getting “worse” over time, albeit not at the pace shown in the data—as house prices have risen faster in affluent places like Silicon Valley. (I mean worsening domestically—consumption inequality is actually falling at the global level.)

PS. I always find that some people are confused by the claim that investment income should not be included with wage income. I like to explain this with a thought experiment of two equally well off twin brothers. Assume that both earn identical lifetime wage incomes, and neither inherits money from their parents. Then both are equally well off. If one chose to buy two Hondas and the other chooses to but one BMW, you would not say the guy with two cars is better off. If one chooses to buy a BMW at age 25 and the other saves and buys two BMWs at age 55, you would not say the more patient brother is better off. (Unless you were the US government). Future goods have less value than present goods. Saying that investment income should be included with labor income is essentially saying:

1. The brother who chooses to save is better off, even though that avenue was open to the other brother, who preferred current consumption. After all, the patient brother will have more total “income”.

2. A BMW that you have to wait 30 years to get is equally desirable as a BMW today. Is that what you believe? If not, then stop talking about income inequality.

PS. In previous posts I sometimes get people claiming a contradiction when I say that income is meaningless, but at the same time advocate the targeting of “national income”. In fact, NGDP does not included capital gains. (And there are other differences as well.)

I do think that it might be better to target total labor compensation rather than NGDP. But not because NGDP inaccurately measures investment income, rather because wage stickiness is the key macro problem that monetary policy needs to address.

PPS. Some commenters claim that income matters more than consumption, because it measures political power. Just the opposite. Suppose Jeff Bezos makes $20 billion in capital gains on Amazon stock in 2017. Does anyone seriously believe that Bezos has more political power than a teachers union representing 400,000 teachers, each earning $50,000/year? Suppose he advocated vouchers for all students in California. Could he beat the teachers union? Consumption is a better index of political power, albeit far from perfect.

In aggregate, 400,000 teachers have far more to lose than Bezos (in terms of foregone consumption) which is why they fight harder for their preferred policies.

READER COMMENTS

Chris

Jul 25 2017 at 8:49am

Wouldn’t a consumption based measure neglect wealth stored as savings or investment? There is huge power that comes with having unused wealth. People do not consume more on a linear income / spending curve which is why inequality appears to decrease when you take this view, but stored wealth allows the wealthy to weather financial difficulties, make investment or life mistakes, and reinvest when the market is down in order to reap greater gains. Without access to this stored wealth the middle and lower classes lacks both security and profit potential.

I got your argument, but it still feels like you’re solving issues of income measures by creating issues of consumption measures.

Scott Sumner

Jul 25 2017 at 9:04am

Chris, If you are interested in wealth, then consumption is a far better proxy than income. My consumption in 2017 will tell you far more about my wealth than does my income.

Jeff

Jul 25 2017 at 10:05am

Agreed that taxing consumption rather than income would be better economics. The trouble is that it’s not better politics. But maybe I’m wrong about this and someone can come up with a way to sell it that hasn’t already failed.

So long as we are taxing income, lower taxes on capital gains as opposed to other forms of income can be portrayed as “lower taxes for the rich”. We’ve been thru several cycles of this already. Reagan cuts capital gains, the Democrats decry it as a tax break for the rich, then capital gains tax rates are raised again. Then it starts over again.

A better approach would be to eliminate the double taxation of dividends by abolishing the corporate income tax and taxing interest income, dividends, and realized capital gains as ordinary income. It might be possible to adjust all of these for inflation, i.e., tax real interest, real capital gains, and subtract the inflation rate from the dividend rate before taxing.

This is not perfect, but it’s better than what we have now. It gets rid of the bias that favors debt over equity financing, and you can sell it as taxing all income the same. A lot of people currently employed as corporate tax collecters and avoiders would find more productive employment.

Zeke5123

Jul 25 2017 at 11:20am

Jeff:

The difficulty there is that you induce lock-in effect. You could then enact mark-to-market schemes, but (a) good luck and (b) liquidity restraints are a real thing. So, assuming we continue with a realization scheme, I am not sure taxing capital gains as ordinary income is desirable from a capital markets perspective, especially if you think PE is worthwhile.

Further, the lock-in will encourage monetization schemes, which permit a taxpayer to economically exit a position without paying current tax. There are a lot of ways to monetize an equity position without triggering tax now, but it (a) costs more money and (b) adds unneeded complexity to markets. Taxing capital gain as ordinary income would encourage such monetization planning, which is not good for the economy. Now, you could try to stop such monetization schemes, but that requires changing a lot of laws on the book (i.e., it isn’t easy).

So, on balance I disagree with taxing capital gains as ordinary income. I get the theoretic appeal, but too many issues.

mariorossi

Jul 25 2017 at 11:20am

I think the large majority of what we call investment income is simply disguised labor income.

Take Jeff Bezos himself. Are you really arguing that his wealth is mostly investment income? He built a business from nothing. I really don’t see why the money he made from Amazon stock should be labelled as investment income. He built it himself. He got paid in stock. Why would his labour be worth what the stock was worth then (if it even traded) rather than now? Ex-post his labour was worth billions and it should be taxed so.

In general any person that doesn’t work for cash would suffer from the same measurement issue: we don’t know what wage he receives until much later. If we simply ignore this type of payment, we create an unfair advantage for people that can structure their wages this way. And this is likely to advantage wealhty people who have less need to be compensated in cash.

The example you make is entirely deterministic. In reality we live in an uncertain world. Investment income taxes are also a tax on luck. If two people make identical risky investments, it seems unreasonable to me to tax the one that made money the same as the person that lost money. And this effect is likely as big or bigger than the time value effect you complain about. In an uncertain world, a tax on labour would not be equivalent to a tax on consumption due to variable capital gains.

I find this issue (lucky investors are completely untaxed) much more unfair than the example you give above, but I guess it’s a matter of opinion…

Alan Goldhammer

Jul 25 2017 at 11:22am

Interesting column as usual. However, not everyone suffers during financial meltdowns. Certainly those who hedged the right way back in the mid 2000 period made out big time (‘Big Short’ folks). Those who were heavy in cash and then came back in the market in 2009 likewise. Also, capital gains/losses are only important when the item in question (equity, bond, home) is sold. Until it’s sold nothing matters (assuming you have done due diligence and not purchased something that is rotten to begin with).

I’m not up on the real estate tax laws but I believe you can offset some of the realized gains on the sale of your home with the purchase of the new one in OC. Count yourself very fortunate that the sold property was not in CA which has a very high cap gains tax on real estate sales (I know from personal experience!!!).

Regarding consumption, I do think it’s a better metric. I recently had an email exchange with Robert Frank following a NY Times piece he wrote on health care and he sent me an appendix to a paper he wrote on a progressive consumption tax which he supports. It’s an interesting proposal.

A lot of stuff could be improved by totally revamping the tax code (both individual and corporate) but given the total dysfunction going on in DC these days, I’m skeptical that’s going to happen.

R Schadler

Jul 25 2017 at 12:00pm

Equality as a concept makes a great deal of sense in mathematics and physics. It is necessary there.

In human affairs, it seems to make sense, to have meaning, but does not. In economics, three criteria are especially important in assessing general economic well being: income, wealth, and access to economic goods. For the middle class, income is highly relevant; the other two, less so. For the wealthy, wealth dominates; income may be so marginal as to be irrelevant (Steve Jobs and others can be a dollar a year employee). In a place with a robust safety net, or for those who are well liked by wealthy relatives or friends, or children generally, access to economic goods without entering the market to get them is the most salient. (Think: Warren Buffett’s favorite nephew who needs no income, no assets, but might well live the life of a billionaire anyway.)

Measuring wealth and income seem plausible, at least to some extent. Measuring access far less so, which may be a big part of why economists tend to downplay it.

But since all three are relevant, any notion of determining on a mass scale the level of “inequality” much less equality, seems completely foolish.

Rajat

Jul 25 2017 at 5:08pm

One thing that often occurs to me about the ‘two brothers’ example: if we didn’t tax capital gains – or returns on saving more generally – would savings increase such that the return on savings fell to at least partly offset the absence of the former tax?

John Hall

Jul 25 2017 at 5:48pm

This might be a bit of a ramble…(mainly about the PS)

The PS says: “I do think that it might be better to target total labor compensation rather than NGDP. But not because NGDP inaccurately measures investment income, rather because wage stickiness is the key macro problem that monetary policy needs to address.”

That last part “wage stickiness is the key macro problem that monetary policy needs to address” seems important, but I’m not sure I would phrase it that way. The problem with wage stickiness is that stickier prices take longer to adjust to shocks (resulting in sustained unemployment, etc.).

The key problem that monetary policy needs to address is monetary disequilibrium. Price stickiness is what makes monetary disequilibrium worse.

So, for instance, if we have a banking crisis that causes a huge negative shock to aggregate demand, then I view that as a pretty important thing for monetary policy to address. And wage stickiness only makes it more important to offset the impact of the demand shock.

Circling back around to the earlier part “I do think that it might be better to target total labor compensation rather than NGDP.” Of course, the U.S., at least, has nominal labor compensation data. In log levels, they have a correlation of 99.99%, so I’m not sure one adds to much value over the other (though log changes have a smaller correlation of 79% and while they seem cointegrated, it is not as strong as I would have though).

I kind of went on and on writing from here, but I’ve deleted it because I wasn’t sure I was really getting anywhere. The key point was that I feel like you keep wanting to get more and more narrow with PW (or PLC) instead of PY. PT was what was in the original equation of exchange. Hard to measure, I know. But the BEA reports Gross output. Why prefer PW to nominal gross output? I’d rather go wide than go narrow. What really matters is aggregate demand right? Not aggregate demand from things that have sticky prices?

Scott Sumner

Jul 25 2017 at 11:39pm

Jeff, You said:

“and you can sell it as taxing all income the same”

I’m trying to convince people not to think this way.

Mario, I think you misunderstood my argument. I argued that Bezos consumed far less than he earned in “income”. Do you disagree?

If investment income is disguised wage income, then it should be taxed as wage income. I have no problem with that argument.

But almost none of my investment income is disguised wage income, and hence it should not be taxed.

Alan, It’s very difficult to offset a gain with a purchase somewhere else–and we would not be able to do so.

Rajat, Probably.

John, I’ve addressed the gross output argument elsewhere–it double counts intermediate goods. I’m not a fan of targeting it.

Thaomas

Jul 26 2017 at 6:47am

To tax capital gains “properly,” on the same basis as other capital income we would need to 1) index the gains and 2) average the gain over the holding period so that it is taxes at the average of the person’s marginal tax rates, not all of the indexed gain in one year.

Now I agree that it would be better still to tax consumption progressively rather than income. Frugal Mr Buffet really should pay less tax than prodigal Lord Fauntleroy who receives the same income.

In political dynamics, I would hope that if we made income taxation more progressive after eliminating business income taxes and wage taxes for financing the health insurance, disability and pensions and converting all deductions to partial tax credits, that the frugal would allay with the Neoliberals to shift from an “income base to a consumption base. But politics is not my comparative advantage.

In one sense, the shift to consumption taxation would be easy; just make asset accumulation deductible from “income.” In another it would reproduce much of the complexity of income taxation. Presumably we still want to encourage folks to forgo personal consumption for donations to charity. We probably do NOT want to encourage consumption of house ownership services, but it’s likely we would have to reproduce this artifact as well. We might not want to tax uninsured health care consumption like other consumption and there may be other kind of uninsured “forced” consumption that would need to receive special treatment. But policing the favored/unfavored consumption line would probably be easier than the wage/non-wage income line, so overall the system ought to be a bit simpler.

As for NGDP vs wage bill targeting, isn’t there some stickiness in non-wage prices too? I’d still like to see the monetary policy target (inflation rate/price level/NGDP/wage bill) and the level of the target derived from a model in which price stickiness and non-monetary policy shocks are the parameters.

mariorossi

Jul 26 2017 at 9:38am

I think it’s pretty much impossible to tell if Jeff Bezos consumed more or less than the income he received.

But I think in the current tax system, it’s very possible he consumed significantly more if we include his heirs in the consumption calculation.

Any assets he leaves to his heirs would be stepped up the value at his death. They could then sell the shares and consume the proceeds without paying a penny (okay not quite, but largely with a bit of tax planning). You can argue that’s a benefit to the heirs and not to him, but I think that it should be counted (at least I see no obvious reason why to exclude it).

And each generation could do exactly the same: work in exchange for (initially worhtless) equity in some business, fund your consumption from assets passed from a previous generation and pass your now valuable equity to the following generation. Zero tax, great consumption…

I am not even going to go into the idea that buying the Washington Post (or any other loss making asset that gives personal prestige/benefits) is really consumption anyway…

I agree it makes no sense to treat realized and unrealized capital income differently: I reach the opposite conclusion, unrealized profits/losses should be taxed annually. But I agree that we should allow tax-free retirement vehicles (up to some reasonable value). There is no point for a middle class person to be subject to such taxes. Such vehicles would also allieviate the unfairness in the high taxation of high variable income.

I am pretty confident Jeff Bezos and Mark Zuckerberg will consume a much large fraction of the value they create than I will. Even charity is a form of consumption in many ways. I don’t get to decide how about half the value I create gets consumed… They’ll do much better…

Conscience of a Citizen

Jul 26 2017 at 12:26pm

Consider twin brothers who from age 18 earn equal wages. Both work for five years, saving all their wages apart from bare subsistence. Then one brother spends all his savings to get a Ph.D. in Economics and the other spends all his savings to get a parking lot downtown.

Subsequently Doctor brother takes a job with the Federal Reserve that pays double his previous wages while Mister brother leases out parking spaces and collects profits which equal double his previous wages, so both brothers take home the same cash income.

Doctor brother’s wages are return on his “human” capital. Mister brother’s profits are return on his “investment” capital.

Question: why should we tax Doctor brother’s wages but not Mister brother’s profits?

Now, after conceding that rents, dividends, interest, etc. should be taxed along with wages, you might still argue that “pure” capital gains– i.e., selling something for more than you paid for it– should go untaxed.

One problem is that when you try to convert that abstract notion into actual tax policy, you have to deal with people evading taxes by tricks like making their firms buy back stock rather than issue dividends. Both are ways to distribute business income but one goes partly untaxed under current law.

Worse, even supposedly “pure” capital gains actually represent some combination of retained earnings, cleverness (choosing ex-ante to buy stock in one firm or another, or to buy land in Dallas versus Detroit), rent-seeking, monetary inflation, and luck. Luck can be positive or negative so it should wash out. Monetary inflation ought theoretically to be indexed out (though there are practical difficulties). However, retained earnings should be taxed the same as wages since they are simply rents/dividends/interest/etc. which we have already discussed, rent-seeking ditto, and cleverness is arguably return on human capital, which is to say, no different than wages and therefore equally liable to be taxed.

In the end, after adjusting for monetary inflation and offsetting gains and losses, we have strong theoretical grounds for taxing the rest of so-called capital gains along with other forms of income.

John Hall

Jul 26 2017 at 3:29pm

I found the link (econlog too, not money illusion). I’m quite positive I’ve read that before. Just must have forgotten!

http://www.econlib.org/archives/2016/01/ngdp_or_ngo.html

I got the annual BEA series and did some cointegration analysis and found it to be cointegrated with nominal GDP. I wouldn’t expect that much difference between using one or the other. The mean log change is roughly similar for both. However, the standard deviation of the quarterly log changes is a bit higher for gross output than NGDP.

Scott Sumner

Jul 28 2017 at 10:32am

I don’t have much time today. Most of the issues raised in the comments above could be addressed by making 401k plans more expansive. No contribution limits and no mandatory withdrawals.

Education is already heavily subsidized, so I’m not worried about overtaxing returns on human capital.

Conscience of a Citizen

Jul 31 2017 at 5:26pm

You wrote almost the same words back in 2015 and they were no more enlightening then.

Why do you suggest “education” is the only component of human capital?

No one else thinks that. There are all sorts of human-capital endowments which are not “subsidized education:” physical strength, intelligence, or most importantly “connections” or access to nepotistic or crony favoritism. Consider Chelsea Clinton!

What about work experience, self-study, and professional (not college/grad-school) training? Those are not subsidized (actually, they are taxed).

If subsidies to “education” mean human capital should be taxed, then why should returns on stock in the massively-subsidized firm Tesla Motors go untaxed?

Conscience of a Citizen

Jul 31 2017 at 11:15pm

I apologize. I should have remembered my manners, to thank you for conceding my main point, before berating you about secondary issues.

You agree that taxing returns to human capital* is the same as taxing returns to investment capital, and now you want to quibble over the proper tax rate. Cool!

Reminds me of the story about the philosopher and the socialite at the dinner party, but hey, the point of that story is that for all of us it sometimes it takes a moment to see a principle hiding under a variety of examples.

Welcome to the club, Prof. Sumner.

*The education component, at least– or if you believe even partly in the signaling model, the purchased badge as well.

Conscience of a Citizen

Aug 1 2017 at 12:19am

Don’t think I fail to admire the subtle way you pointed up the value of graduate education in Economics, either.

If we ought to tax Doctor Brother’s wages (in my hypothetical example above) because his graduate education was subsidized (presumably we tax him to recoup some of the subsidy), that must mean his degree is worth more than he paid for it out of pocket, and is therefore worth more (somehow) than Mister Brother’s not-to-be-taxed parking-lot investment. Well, certainly a Ph.D. in Economics is very valuable, though somewhat illiquid.

However, the (market) NPV of Dr. Brother’s Ph.D. is the same as that of Mr. Brother’s parking lot (ex-hypothesis). So where did the subsidy go? Not into Dr. Brother’s pocket! In fact, it obviously went where most such subsidies go: into the pockets of the graduate school and its staff.

In the real world, nearly every economist who looks into the subject comes away convinced that American government subsidies to higher education nearly all benefit schools/staff, not students (who all choose how much to spend out-of-pocket based on their best estimates, however flawed, of how much education will increase their earnings, in comparison to other possible investments).* If you wished to recover subsidies by taxing their recipients, you would tax schools and their staffs.

(You might argue that taxing graduates amounts to indirectly taxing their employers, who get at least some of the benefit of the education subsidy. But that is a difficult tax-incidence question and also neglects the huge share taken by educators before employers get their bite. I don’t think you can redeem the first-order problem with second-order handwaving.)

*I neglect the portion of “education” consumed strictly for entertainment, as I’m sure you will agree is proper. Since most students (or their parents) pay most “education” costs with after-tax dollars, the consumption component of education is well-taxed already, and all along we have been discussing taxes on future income attributable to education, which must perforce be taxes on human capital gained through education, if any.

Pat

Aug 8 2017 at 12:44pm

“I frequently argue that income is a meaningless concept, as it includes capital gains (and losses) in asset values.”

I don’t understand why the inclusion of cap gains/losses makes income meaningless.

Comments are closed.