Alex Tabarrok has an interesting new post on trends in housing prices:

In 2005, I thought housing prices were rising above the fundamentals and I said so. In 2008, as the fall in housing prices was well under way, I wrote a blog post and later a NYTimes op-ed saying that the housing price bubble was not nearly as big as people thought. I wrote:

I think that housing prices went beyond the fundamentals sometime around 2004…but 2004 levels are still well above long run trend.

…Prices will probably drop some more but personally I don’t expect to ever again see index values around 110. Do you? If we don’t see the massive drop back to “normal” levels then the run up in prices should be described as a shift to a new equilibrium…[with some overshooting, rather than as a bubble.]

To put it mildly, not everyone agreed with my argument. I certainly got the timing wrong-I didn’t think the recession would be as long or as deep as it was. Nevertheless, some people are coming round to my point of view. Karl Smith, for example, has a new post Was There Ever a Bubble in Housing Prices? which concludes more or less, as I did nearly ten years earlier, that the answer is no. What happened was greater liquidity which made housing prices gyrate more like stock prices but “the fundamental driver isn’t irrational bubble behavior. It is competition over a scarce resource.”

I have frequently argued that bubbles are a myth, or more precisely the “bubble” concept is generally not a very useful tool for understanding the world. In the comment section to Alex’s post, Alan Goldhammer made this remark:

First of all there were some prescient folks who called the ‘bubble’ very early on including Dean Baker and the Calculated Risk duo of Bill McBride and the late Doris Dungy.

At first glance it would seem that an early prediction is better than a late prediction. But in a 2010 post I argued just the opposite—the earlier predictions were less accurate than later predictions, indeed not accurate at all.

When Dean Baker warned of a housing bubble in 2002 and Robert Shiller warned of “irrational exuberance” in the stock market in 1996, they weren’t merely suggesting that bubble conditions might develop in the future, they were claiming that asset prices were already at excessive levels.

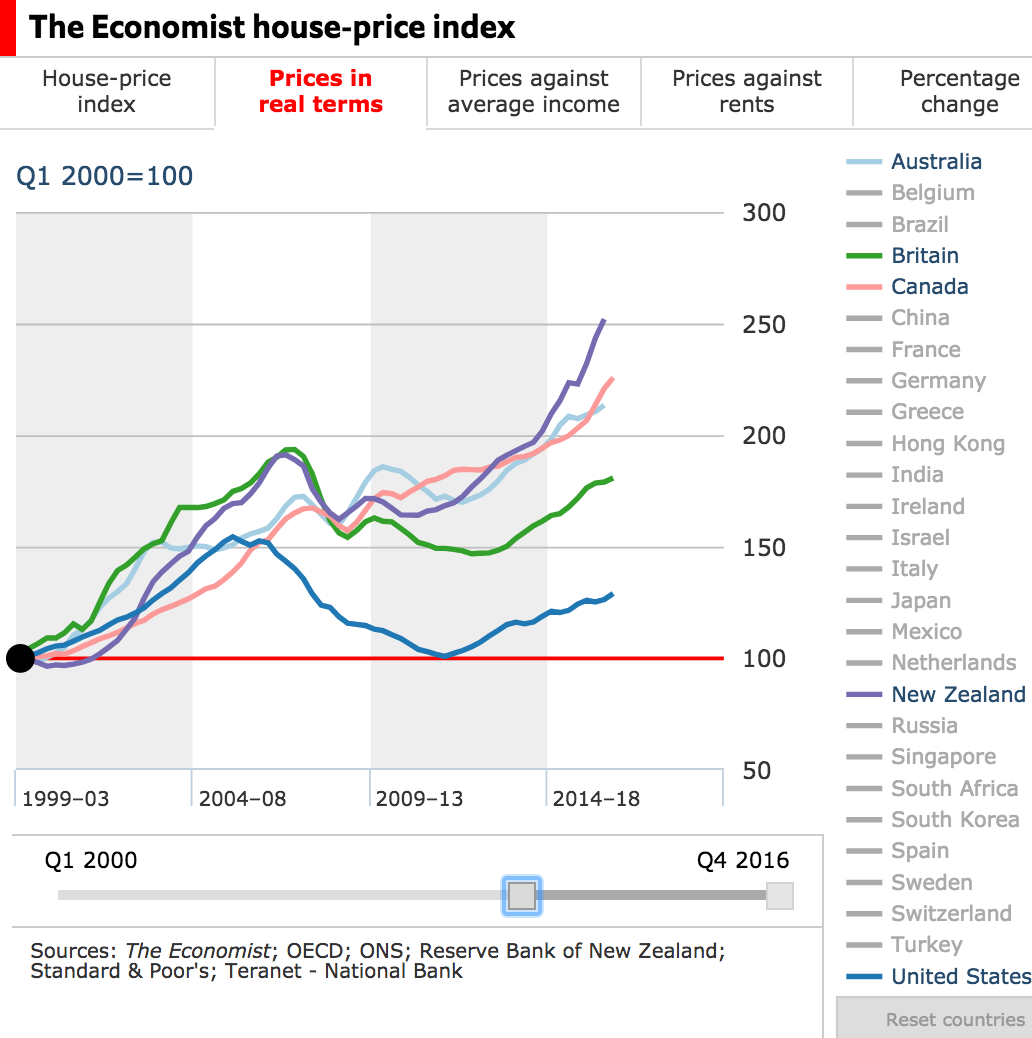

In retrospect, those claims don’t seem particularly prescient. Tabarrok’s post shows that housing prices are now above 2002 levels, even in real terms. And of course stocks are now far above 1996 levels. That doesn’t mean they were necessarily wrong; perhaps housing and stocks are in a new bubble. But it does mean that one cannot simply point to these early predictions as being obviously correct bubble calls, as it is by no means obvious that prices were excessively inflated in those two cases.

I often suggest that bubble claims will be increasingly popular during the 21st century. That’s partly because recent bubbles are widely (and wrongly) viewed as having done great damage to the economy, and also because with the “new normal” of ultra low interest rates, asset values will often seem higher than justified by many of the usual metrics.

READER COMMENTS

Shane L

Aug 9 2017 at 12:34pm

I was definitely one of those who assumed that the housing crisis was caused by a bubble in construction. It has been amazing here in Ireland to watch house price declines flip rapidly and construction once more to soar, especially around Dublin. Rising rents, prices, and homelessness suggest that there is a real lack of accommodation around the city, something I could not have believed in 2009, so I got that wrong.

One thing I did notice in the immediate aftermath of the housing crash was a general deification of any commentator who had been predicting economic calamity. Even at the time it struck me that this was flawed because all kinds of groups were predicting doom, and had been for years or decades. Religious groups, communists and individual contrarians joined the few far-sighted economists in predicting calamity in the 2000s. In fact, I can confidently predict right this moment that there will be another period of economic chaos… eventually.

Without a deadline, predictions are not so meaningful.

anomdebus

Aug 9 2017 at 4:30pm

When is too early to warn of the ‘bubble’ bubble? What is the likelihood of a ‘bubble bubble’ bubble developing?

Alan Goldhammer

Aug 9 2017 at 4:47pm

It may be that a “bubble” is in the eye of the beholder. I could have amplified on my response to Alex’s blogpost by noting that a number of people made a lot of money when the housing bubble burst as noted by Michael Lewis in “The Big Short.” There will be more money made in the coming years with the rebound in real estate prices by those who had the cash to purchase properties that were either in foreclosure or “short sales.” In a number of housing areas, investors or groups purchased housing and that stock is now being rented out. At some point the investors will cash in. Surprisingly, there is actually a lot of rental housing in the Washington DC area and we were not hit all that hard in terms of price drops.

I agree with Scott’s point about asset prices being higher as a result of the “new normal, ultra low interest rates.” One cannot count on reliable returns fixed income accounts (bonds, bank interest, etc.) with rates so low. IMO, this forces anyone planning for retirement to consider equity or real estate investment if they hope to maintain enough capital/income during their non-working years. It forces an intrepid investor to really delve down deep into financial disclosure statements to make sure that the companies are rock solid.

Dean Baker had a very nice comment on lesson’s learned regarding the financial crisis today.

Kevin Erdmann

Aug 9 2017 at 7:29pm

Alan, if low rates were driving other asset prices, we would have been seeing high levels of investment in things like real estate. Investment is low in spite of very high yields in real estate, and on an enterprise value basis, corporations have very low leverage and pretty normal valuations.

In your link, Baker claims that the housing bubble was not based on fundamentals. He is making the error of looking at national numbers. Looking at individual MSAs, rents have been diverging for 20 years, and those diverging rents basically explain the bubble. Prices were also highly varied among MSAs, highly correlated to rent inflation. I’m afraid it is Baker who has learned the wrong lessons.

Thaomas

Aug 10 2017 at 6:42am

I would not worry about people correctly or incorrectly predicting variance in asset prices if

a) perceptions of a “bubble” did not cause the Fed to take its eye off the ball of keeping the price level growing at a constant percent (2% pa ma be too low, but that’s another story) [I think perceptions that there was as an asset, bubble in 2008 contributed to the Fed’s tardy and tepid response to the financial crisis, especially to the failure to head off widespread mortgage foreclosures] and

b) “correct” predictions did not raise the credibility of the correct predictors’ policy recommendations in other areas. [That gold bugs, inflation hawks, and other financial vermin could claim to have “predicted” the 2008 crisis contributed to their political influence in preventing the Fed from carrying out “everything it takes” policies to maintain price level growth and quickly restore full employment.]

Alan Goldhammer

Aug 10 2017 at 8:21am

Kevin, the real estate side of things is complicated and one doesn’t see uniformity in terms of asset price appreciation. Shopping malls are being battered by on line vendors such as Amazon. Look at what is happening to Sears Holdings. Virtually all the value now is in the real estate portion, some of which has been spun off into Seritage Properties. Even so, the real estate has been marked down several times to accord with PV.

Housing prices have rebounded since the bottom was marked in 2008-9. Office space in growing cities has increased in value but in those cities that have lost jobs there are problems.

Bill McBride over at Calculate Risks regularly charts the Rent/Own ratio for housing. I’ll need to go back and check on that; you are likely correct regarding what you state about the divergence.

Marc Sargen

Aug 10 2017 at 2:09pm

The big difference between overvaluation & a bubble is frenzy & most normal metrics are not really geared to detect frenzy.

I view a bubble frenzy is when people are doing actions that most of the time would look completely ludicrous.

During the Dot.com bubble the were regular reports of average people quitting their job, maxing their credit cards, & becoming day traders. What metric it there to separate what they were doing from other trades?

During the housing crisis spec building was rampant, cranes covered Las Vegas & there were people with limited income buying multiple houses with 100%+ loans expecting to flip them in a few month to get 20% returns. While prices have soared in some areas, I just don’t see a huge number of absurd activity that occurred during the bubble even in Silicone Valley

A friend of mine in China was telling me of a number of associates who are considering getting a divorce so they can get around the property limitations being imposed by the government & buy twice as many. Bubble frenzy?

Kevin Erdmann

Aug 10 2017 at 5:33pm

Marc, you have explicitly pointed to a government restriction. If, during the one child policy families had engaged in regulatory arbitrage in order to have two children, would you have called that a bubble in reproduction? Why treat the cases differently?

Lorenzo from Oz

Aug 12 2017 at 6:30pm

If turning points in asset prices could be reliably predicted, they wouldn’t happen (since no none would buy at the “about to be seriously undercut” price).

The “bubble” folk don’t seem to understand that calling it a “bubble”:

(1) entails not knowing when the turning point will happen;

(2) means prices are reflecting current information, not information that hasn’t become available yet.

The most one can squeeze out is that there may be herd effects in asset prices (i.e. people think prices will rise, act on that shared belief, so prices rise). But as we have no idea when the herd effect will stop happening (see [1]), that doesn’t get us very far. After all, herd effects (possibly “flock effects”, as the mechanisms seem similar to bird flock movements) can operate in either direction.

Identifying what is driving current asset prices movements, and how robust those factors are, is useful, but that is useful without adding in the “bubble” usage.

So, all a “bubble” claim ends up doing is something saying something like “I believe current asset prices are based on thinly grounded expectations which will collapse at some unspecified (indeed, unknown) point in the future”. Doesn’t seem to get us very far–apart from being an awful basis for monetary policy.

Comments are closed.