For most of the past decade, I’ve been arguing that people have underestimated the role of falling nominal GDP in the financial crisis of 2008, and that falling NGDP was almost completely to blame for the Great Recession itself. Now it looks like I might have been one of those people who underestimated the role of falling NGDP. Ben Southwood sent me a very interesting NBER paper by Stefania Albanesi, Giacomo De Giorgi, and Jaromir Nosal, which argues that the financial crisis was not caused by a surge in subprime lending. Here’s the abstract:

A broadly accepted view contends that the 2007-09 financial crisis in the U.S. was caused by an expansion in the supply of credit to subprime borrowers during the 2001- 2006 credit boom, leading to the spike in defaults and foreclosures that sparked the crisis. We use a large administrative panel of credit file data to examine the evolution of household debt and defaults between 1999 and 2013. Our findings suggest an alternative narrative that challenges the large role of subprime credit in the crisis. We show that credit growth between 2001 and 2007 was concentrated in the prime segment, and debt to high risk borrowers was virtually constant for all debt categories during this period. The rise in mortgage defaults during the crisis was concentrated in the middle of the credit score distribution, and mostly attributable to real estate investors. We argue that previous analyses confounded life cycle debt demand of borrowers who were young at the start of the boom with an expansion in credit supply over that period.

I had previously bought into the conventional wisdom on subprime loans. And here’s how their study differed from previous work in this area:

Mian and Sufi (2009) and Mian and Sufi (2016) identify subprime individuals based on their credit score in 1996 and 1997, respectively. We show that, since low credit score individuals at any time are disproportionally young, this approach confounds an expansion of the supply of credit with the life cycle demand for credit of borrowers who were young at the start of the boom. To avoid this pitfall, our approach is based on ranking individuals by a recent lagged credit score, following industry practices. This prevents joint endogeneity of credit scores with borrowing and delinquency behavior but ensures that the ranking best reflects the borrower’s likely ability to repay debt at the time of borrowing. Our analysis shows that income growth and debt growth are positively related during the credit boom for individual borrowers.

This finding is especially important for the work of Kevin Erdmann. It’s looking more and more like Kevin got the housing crisis right before anyone else. I eagerly await the publication of the book that he is working on.

PS. The fact that the crisis doesn’t seem to have been caused by a surge in risky lending does not mean that our financial system is fine. The system is still riddled with moral hazard, which creates a bias toward excessive debt. It’s just that this problem doesn’t seem to have gotten worse in the lead up to the Great Recession. Something else is to blame—presumably tight money (i.e. falling NGDP)

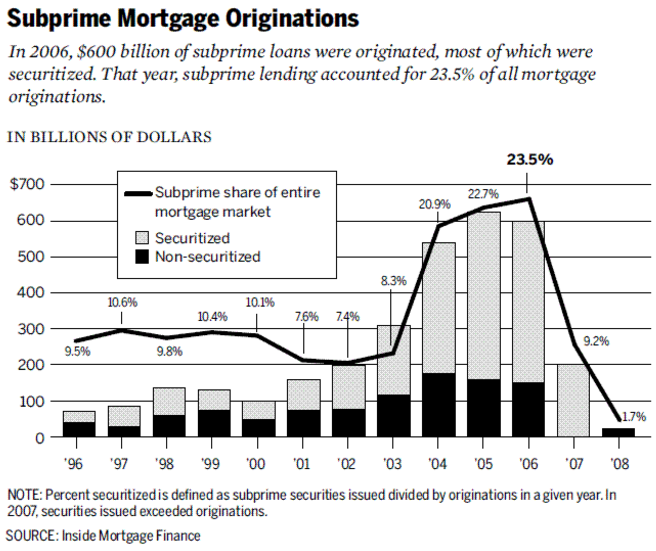

PPS. I’m sure that people will contest this study—it will be interesting to see how the debate plays out. The stylized facts do seem to point to a surge in subprime lending:

READER COMMENTS

Alan Goldhammer

Aug 30 2017 at 1:44pm

If this is so, then why was there a collapse of the CDO market and the companies that were blithely insuring the CDOs. The answer is in the graph that you show that comes from the inquiry paper done after the meltdown. The subprimes may have been constant but what was not constant was their repackaging into debt instruments that few understood. Furthermore, the worst afflicted areas were where subprime loans were highest (CA, FL, AZ).

Kevin Erdmann

Aug 30 2017 at 3:14pm

Whoa! What a find, Scott. Thanks!

I’ll be doing some reading and writing today with the Theme from Rocky playing at full volume, in case anyone wonders what that sound is….

Antischiff

Aug 30 2017 at 3:50pm

Dr. Sumner,

There seems little doubt to me that the financial system was too fragile at the time. Sure, at one point NGDP was falling at 2% quarterly in Q4 of 2008, if I recall correctly, but for so many institutions to fail or be near failure under those circumstances seems suspicious.

Antischiff

Aug 30 2017 at 3:53pm

Kevin Erdmann,

I look forward to reading your book.

Antischiff

Aug 30 2017 at 3:58pm

Dr. Sumner,

To clarify, if subprime wasn’t much of a problem, then perhaps leverage was. I believe you’ve commented before about how you thought moral hazard and ignorance on the part of management of big institutions was a problem.

magilson

Aug 30 2017 at 4:59pm

Alan Goldhammer:

I think you are misinterpreting the results of the study. CDO magnified the problem as you allude to but this article is simply looking at how sub-prime loans behaved in this time frame. In other words nearly any tranche of loan can cause a “failure” of a CDO. The popular theory is that it was the sub-prime. This study suggests that while sub-prime caused issues it may not have been the primary cause.

Also, if an entire housing market was failing (and/or financial market for that matter) it would only make sense that areas with high sub-prime would be hardest hit as sub-prime areas would indicate low-income and/or low savings areas. If you understand it differently I’m interested to hear it. But when an economy begins to fail it doesn’t have to fail evenly.

Michael Rulle

Aug 30 2017 at 5:02pm

I think it is much more accepted now that the Fed was tight in 2007-2008, and you certainly were at the front of the curve on that analysis.

However, more than one thing can be true. I still find it amazing that the overwhelming percentage of troubled loans came from California, Nevada and Arizona. Throw in Florida and it just about covers the whole crisis.

Because the volume of transactions, primarily refinancings, was so high and the credit quality so low (due to FNMA’s decision (with full moral hazard in place) to concentrate almost exclusively on sub prime loans), and the securitized vehicles so poorly documented, market participants had trouble evaluating the securities and feared the worst.

Hence, at the time, many believed it was a true solvency crisis, when we now know it was really a liquidity crisis (yes, the latter can turn into the former, but for liquidity reasons!). So, from a micro perspective, so much was unknown about the instruments, yet from a macro perspective, it was relatively easy to back into an implied default rate to justify the low mark to market values.

The implied default rates were triple what they ended up being. The most conspicuous example of this was the value of AIG’s credit derivative portfolio—which ended up having virtually zero defaults.

So the tightening obviously contributed to the crisis, particularly when liquidity was needed. But the I think it was a contributing cause.

I still would like to see the definitive study of why the 3 western states’dominated the market. Obviously it had to do with policies in place etc.

scott sumner

Aug 30 2017 at 5:43pm

Everyone, Good comments. Just to be clear, the fact that subprimes were not “the problem” doesn’t mean that they were not “a problem.”

Alan Goldhammer

Aug 31 2017 at 8:47am

Regarding the experience in CA, AZ, NV, and FL, it is useful to contrast what happened in Texas and why there was not a similar implosion.

Kevin Erdmann

Aug 31 2017 at 12:48pm

Alan, that article is a great example of how credit explanations gained favor. I have seen versions of this article copied from several sources with little skepticism. But, the article and the Fed paper it references don’t present anything that would stand up to the slightest scrutiny. There is one basic fact – that mortgage growth scaled with home prices – and everything is built on that correlation, with little concern for the need to confirm causation.

During the housing boom, Texas actually had relatively high default rates.

Also, consider the 40 other states that didn’t have bubbles. Did they all have this rule?

In Texas, there is practically nothing you could do with credit markets to cause a price bubble, because if it costs $100,000 to build your house, then with the slightest increase in market prices, somebody down the road is going to build that house and sell it for $105,000. If anything, loose credit in Texas causes rents to decline.

I think if you take a step back and think about it, the idea that home prices didn’t go up by 50% or 100% and then collapse in Texas because they had a rule limiting home equity access is pretty ludicrous. But, there are thousands of these articles, presented with utter credulity, that have created a vague, bulging set of “facts” about what caused the bubble.

Thaomas

Aug 31 2017 at 2:26pm

Scott,

I get the idea that falling NGDP IS the “policy” that effectively results. Maybe if more people thought that way, things would be better. But give where the world’s thinking was in 2007 and still IS, why not criticize the specific actions and inaction that resulted in the falling NGDP.

On a slightly different note, I’d point to the problem of expectations or “animal spirits.” When a recession gets started, regardless of origin, that may change the relations between the instruments of monetary policy — how much of which assets need to be purchased — and NGDP.

Robert Dell

Aug 31 2017 at 11:43pm

Regardless of the relative growth of high-risk “prime” loans vs. subprime/Alt-A, wasn’t the chief concern among Wall Street bank creditors/depositors the highly leveraged systemic accumulation of subprime/Alt-A residential mortgage-backed securities (mis-rated AAA ex ante) and the prospect of a wave of large bank failures as a result of falling valuations and system de-leveraging? And after the Lehman bankruptcy, wasn’t the chief concern among Fortune 500 CEOs (who made the big lay off decisions) the prospect of falling aggregate spending in the wake of a severe credit tightening and no Fed commitment to maintain NGDP growth? Wasn’t this latter concern—or fear—or self-fulfilling prophecy essentially what produced the Great Recession?

Lorenzo from Oz

Sep 1 2017 at 7:35pm

You might want to change the NBER link to this, as the one you have has some weird Russian overlays.

Comments are closed.