A week ago I criticized an article in the Economist, which saw a “puzzle” in the co-existence of low unemployment and sluggish wage gains. I said there was no puzzle, as wage growth was slow because nominal GDP growth was slow. The labor market can eventually adjust to almost any (reasonable) trend rate of growth in NGDP.

Now the Economist has responded, and in doing so has somewhat misinterpreted my position. That’s actually not their fault–my post was very terse and the nuances of this issue are quite subtle, with many different interpretations. For instance, take their concluding paragraph:

Janet Yellen’s critics tend to say she is excessively devoted to the idea that low unemployment portends higher inflation. They characterize this as adherence to the Phillips curve, which is associated in many peoples’ minds with Keynesian thinking. But it was monetarists who first argued that policymakers ultimately cannot control unemployment, because if loose money drives unemployment too low, inflation will accelerate. It is right for the Fed to look for the labour market for signals as to whether monetary policy is tighter or looser than the economy can sustain. Wage growth is the clearest of those signals. And it suggests that we are not in the long run yet.

Many people will read this and infer that it was the monetarists who came up with the idea that the Fed should look to the labor market for signals about the appropriate stance of policy. That’s not the case. When Milton Friedman developed his Natural Rate Hypothesis, he argued that unexpectedly high inflation caused low unemployment, and unexpectedly low inflation caused high unemployment. Many Keynesians took that idea and reversed it—that low unemployment causes high inflation. That was not Friedman’s view (nor mine). In addition, many Keynesians came to believe that the natural rate of unemployment could be estimated, and used as a guide to policy. That was not Friedman’s view. Friedman believed (as do I) that the natural rate of unemployment changed over time, and was difficult to estimate. He favored steady growth in M, whereas I favor steady growth in MV. But neither of us have been supportive of using the natural rate as a guide to policy.

Now I don’t want to take this too far. I concede that if unemployment suddenly soars from 4.5% to 10%, as it did in 2007-09, and NGDP falls, that’s prima facie evidence that unemployment is above the natural rate. What I deny is that we can know whether unemployment is above or below the natural rate today, when unemployment is 4.4%. In between those two extremes we might have varying levels of confidence in estimating the position of the labor market. Both Friedman and I believe that the Great Inflation of 1966-81 was partly caused by people underestimating the natural rate of unemployment, and the central bank responding with an excessively expansionary monetary policy. I don’t want that to happen again.

That’s not to say I’m necessarily opposed to easier money. The Fed is falling short of its 2% inflation target, and you can make a good argument that easier money is needed to hit the target. What I deny is the claim that the labor market provides justification for an easier money policy today.

Mr Sumner’s view implies there is no output gap, the labour market is in equilibrium, and wage growth is low because inflation expectations have been low. I find this unconvincing, for two reasons. First, it means that unless the Federal Reserve brings job growth back in line with working-age population growth, inflation will soon rise. (Central banks cannot for long keep unemployment below its natural rate.) Yet inflation is in fact falling. Second, as Adam Ozimek at Moody’s Analytics has shown, wage growth as measured by the employment cost index is almost exactly where you would expect it to be given the employment-to-population ratio for 25- to 54-year-olds (see chart). If the rate of wage growth consistent with labour market equilibrium had changed to account for a shift in trend nominal GDP growth, you would expect this relationship to have broken down. It has not.

Actually, I would argue that we don’t know whether there is an output gap or not. Economics it too imprecise a science to make these sorts of fine distinctions. We underestimated the natural rate of unemployment in the 1970s and overestimated the natural rate of unemployment in the late 1990s. But I’m willing to play the devil’s advocate, and defend the hypothesis that we are at the natural rate of unemployment (and employment).

What is the Economist’s evidence against this claim? They point to the fact that employment is rising faster than expected, based on growth in the prime age labor force. And I plead guilty to not expecting this to occur this year. (Japan has also had more growth in employment than I expected.) Like many economists, I did not expect unemployment to fall to 4.4%. But contrary to the Economist, this does not show that we still have economic slack in the economy. The strongest argument for economic slack is a falling unemployment rate coinciding with a stable rate of wage inflation. We have that, so I’m happy to admit that it now looks like there was some slack a year ago. But will unemployment keep falling? Maybe, but I’m not convinced. If it’s about 3.5% next year then I was wrong. If it’s 4.2% to 4.5% next year then that would count in my favor.

A second (and more recent) argument for economic slack is that even if unemployment bottoms out, there are people on the sidelines just waiting to enter the labor force. According to this view, an easier money policy may not reduce unemployment much further, but will lead to more employment by expanding the labor force. This is basically a brand new theory, and I just don’t see the data to support this claim. I also find it hard to see the theoretical justification.

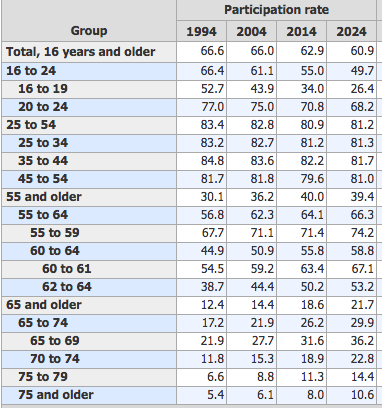

I find it much more plausible to assume that the rapid growth in employment reflects secular trends in labor force participation, especially among the elderly. Perhaps various social trends are leading to an extra 50,000 non-prime age workers each month, and these workers are entering the labor force for reasons unrelated to diminishing economic slack. If this seems implausible, let me frame it differently, and tell me which is more plausible:

1. Over a 12-month period, an extra 600,000 older people start working because boomers are retiring, they are still healthy, service jobs don’t require brute strength, and American pensions are often inadequate.

2. Over a 12-month period an extra 600,000 people enter the labor force because they think jobs are easier to find when the unemployment rate is 4.4% as compared to when it is 5.0% (a year earlier)

It’s quite possible that both of these are true to some extent. But I find the second one to be less plausible. I can understand “discouraged workers” when there is 8% or 10% unemployment—but 5%? Would a bit easier money by the Fed actually draw new workers into the labor market? Yes, a few, but how many? My hunch is that employment has been growing faster than working age population because unemployment is falling and because more older people are entering the labor force. I expect unemployment to stop falling soon, and I don’t think the recent trend of the elderly entering the labor force is any sort of “economic slack” phenomenon that can be sped up with easier money. Trying to do so risks destabilizing the economy.

As far as the wage/employment graph, I believe Phillips curves are roughly vertical in the long run. So I don’t see how that evidence refutes any of my arguments.

Again, a bit easier money might be appropriate—to hit the Fed’s 2% inflation target. But don’t try to target the labor market. That didn’t work out well in the 1970s, and there’s no reason to expect it would work any better today.

PS. I picked the assumption of more elderly people working as just one example of why the labor force might be growing faster than the working age population. There are many other possible assumptions. I picked the elderly because the data seems to point in that direction:

READER COMMENTS

David R. Henderson

Sep 2 2017 at 10:26am

Scott,

Your data on participation rate of the elderly (of whom I am now one) over time are amazing. Most striking are the 75 an up (and I not one of these.)

Jerry Brown

Sep 2 2017 at 12:15pm

Scott, this may be a silly idea but maybe the labor market is close to where economics assumes it is usually- where potential workers actually are considering their employment status as a tradeoff between leisure and the rewards that being employed and putting up with the hassles of a job entail. If that is the case then many people could decide to re-enter the labor market if those rewards get better or the hassles decline. Not all the rewards of being employed are monetary in nature and neither are the hassles, so there may not necessarily be much cost increases as the unemployment rate decreases.

Cloud

Sep 2 2017 at 12:27pm

You are saying the “Never retired” generation is the reason we can’t see the inflation going up under this level of the unemployment rate.

In this case, are we still talking under the Phillips Curve framework? Which I mean, prime-age unemployment can “predict” the inflation rate?

Scott Sumner

Sep 2 2017 at 1:30pm

Thanks David.

Jerry, The problem with that argument is that easier money makes the reward for working (real wages) lower, not higher.

Cloud, No, the “never retired” issue doesn’t affect the unemployment rate, it affects the rate of employment growth relative to growth in the working age population.

Jerry Brown

Sep 2 2017 at 4:15pm

I guess what I was trying to say is that not all the rewards for working are ‘real wages’ in a lot of jobs. Some particularly miserable jobs yes, but many,- I don’t know. Economists like to assume that all people are motivated by money alone all the time. Yes, I know they have their ‘utility’ theories as well sometimes, but those are frankly ridiculous.

It strikes me that for the last 30 years or so I have lived the economists’ dream life as far as theories about employment. I mean I am self-employed in an industry (construction) that has low barriers to entry, that is fairly competitive as far as price and quality, and where I have no ‘market power’ aside from my general personality and reputation. And in a part of the industry, (residential repair and renovation) that is really impossible to regulate for the most part.

Maybe I am just Abby Normal, but it seems to me that most economist’s ideas about what motivates me to take on any particular project miss many things, and it definitely is not always about the money, although that is always a concern at some point. And it turns out that my ‘real wage’ varies considerably from project to project, and unfortunately, it sometimes (rarely, thank goodness) approaches zero or even negative numbers.

Anyways, back to your reply- easier monetary policy might make the monetary rewards for my last project worth less, but it seems to have an effect on demand for my services going forward also. Especially in a highly cyclical and finance dependent field like I am in. Which sometimes spurs me to charge more for my labor or to just provide more of it, depending on many different considerations.

Rajat

Sep 2 2017 at 10:46pm

I’m keen to understand this because it’s really one of the difficulties that I think many people have with the monetarist perspective.

Following up on Cloud and Jerry’s comments:

Scott Sumner

Sep 3 2017 at 2:19am

Rajat, I am referring to both phenomena, although as you suggest it doesn’t really matter. I assume that in the majority of cases they would just keep working past 65.

I do think that decision might depend on the state of the labor market, but I don’t think monetary policy would have much impact when unemployment is down around 5%. Maybe monetary policy might be a factor when unemployment is 8% or 10%.

Dogberry

Sep 3 2017 at 1:11pm

The difficulty in precisely estimating the size of the output gap seems like a good argument in favor of erring slightly on the side of not tightening, so long as there’s going to be discretion at the Fed. Makes me think of the governors who wanted to tighten in 1996

Thaomas

Sep 4 2017 at 11:44am

We should have “erred on the side of not tightening” until the price level (or better, the NGDP level) was back on its pre 2008 trend. Now if we ever faced a situation of on-trend price level increases and high unemployment, that might be time to re-think the price level trend target. That is pretty unlikely, so the labor market is seldom a reliable guide to monetary policy.

Todd Kreider

Sep 4 2017 at 10:48pm

The projections for 2024 should be ignored.

1) $1500 of computer power that is now at around a “mouse brain” will be at a “monkey brain” soon and at a “human brain” level by 2022/2023. Here comes serious autmoation (Does the U.S. really need more than 20 econ profs?), and it isn’t at all clear which way that will push labor participation at different ages.

2) The coming health pills and other medical technology will make eveyone over 40 much healthier by 2024 and also change laborr participation. One example: far fewer jobs caring for the elderly in 2024.

This isn’t going to be a case of either Super A.I. or no changes.

Comments are closed.