Tyler Cowen recently linked to an interesting paper by Emi Nakamura and Jon Steinsson, which discusses the problem of identification in macroeconomics. One section looks at what we know about the monetary policy transmission mechanism:

What is the most convincing evidence we have for monetary non-neutrality? When we have asked prominent macroeconomists this question, the most common answers have been: Friedman and Schwartz (1963), the Volcker disinflation, and Mussa (1986). . . .

The fact that monetary economists point to these three pieces of evidence as most convincing is interesting and informative regarding the types of empirical methods that are influential in macroeconomics. Two of these three pieces of evidence are large historical events typically cited without reference to modern econometric analysis: the Great Depression and the Volcker disinflation. The third is essentially an example of discontinuity-based identification. Conspicuous by its absence is any mention of evidence from Vector Autoregressions (VARs) even though such methods have dominated the empirical literature for quite some time. Clearly, there is a disconnect between what monetary economists find most convincing and what many of them do in their own research.

Recall my recent post where I argued that economics PhD students need to spend more time studying monetary history and less time on highly technical models.

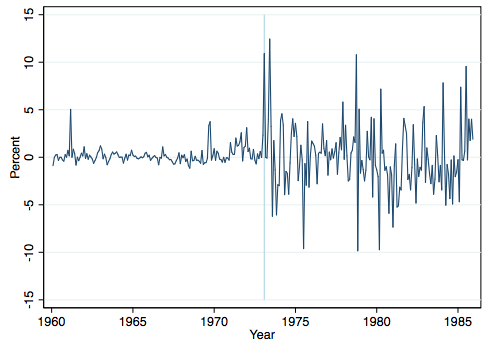

Some readers may be familiar with Friedman and Schwartz, and also the Volcker example, but not the Mussa study. Mussa showed that the real exchange rate became far more volatile after the Bretton Woods fixed exchange rate regime was abandoned. Here’s a graph of monthly changes in the US/German real exchange rate:

You might think it’s no big deal that exchange rates becomes more volatile after the end of Bretton Woods—after all, Bretton Woods was a fixed exchange rate regime. Actually, it’s a huge deal, as you’d expect the real exchange rate to be unaffected by a purely monetary change, like switching from a fixed to a floating exchange rate regime. (BTW, this claim has nothing to do with the concept of purchasing power parity–real exchange rates should not become more volatile regardless of whether PPP holds or not.)

So why do real exchange rates clearly become more volatile when you move to a floating exchange rate regime? The most likely explanation involves sticky wages and prices. Under a fixed exchange rate system, a change in the real exchange rate requires a change in the relative price levels. If prices are sticky, then the price level will respond slowly to a shock that impacts the equilibrium real exchange rate. Monthly changes in the real exchange rate will be small, because monthly changes in the nominal exchange rate are zero, and monthly changes in the price level are small (sticky prices.) By definition, the change in the real exchange rate is the change in the nominal exchange rate plus the change in the relative price levels.

After Bretton Woods was ended, nominal exchange rates became highly volatile. Prices remained sticky, so the nominal volatility turned into real exchange rate volatility.

Why is this powerful argument for monetary non-neutrality so important? Because it doesn’t just relate to real exchange rates, it also means that Fed policy can affect other real variables, such as real GDP, real interest rates, and real wages.

In the long run, money is roughly (not precisely) neutral. That means that printing money is not a path to prosperity for a country like India. But money is non-neutral in the short run, which means that printing money can boost real incomes when output is below potential.

Update: It occurred to me after I wrote this that my statement about PPP might have confused people. If PPP holds, the real exchange rate is always precisely one, under both fixed and floating rates. If it does not hold, and if money is neutral, then volatility of real exchange rates doesn’t change when you move from fixed to floating rates.

READER COMMENTS

Iskander

Oct 11 2017 at 1:51pm

Excellent Post!

You mentioned on TheMoneyIllusion that you were working on two book projects, would you mind revealing what they are about?

Nathan Smith

Oct 11 2017 at 2:35pm

When you say that “economics PhD students need to spend more time studying monetary history and less time on highly technical models,” do you mean:

(a) they would benefit their own careers more by reading history than honing technical models, or

(b) they would contribute more to the state of knowledge in the discipline of economics by reading history rather than honing technical models?

I’m sure (b) is true, but I’m not sure about (a). Vast quantities of peer reviewed publications are sheer deadweight loss and add nothing to the sum of human knowledge, but still get their authors a lifetime of taxpayer dollars on a university payroll. In general, I think the problem isn’t so much with the PhD students as with the tenure committees, and the exclusive focus on peer review in tenure decisions.

What would happen if tenure decisions were based 30% on peer reviewed publications, 30% on popular press publications and blogging, and 30% on performance on a nationally standardized knowledge exam, with 10% left for rapport with students etc.?

Alec Fahrin

Oct 11 2017 at 6:27pm

Has anyone calculated or quantified the significance of this effect? Has the significance decreased over time as the money market has become more electronic? Just a quick analysis of the chart provided shows about a tripling of the volatility in the real exchange rate after 1972.

Also, I realize you’re busy with your work, but if you can do a post on cryptocurrencies and their likely effect on money non-neutrality that’d be awesome.

Specifically, I’m focused on what will happen to these assumptions when Central Banks start releasing their own backed electronic currencies, but right now there’s very little (no) research to even point to.

Scott Sumner

Oct 11 2017 at 11:02pm

Iskander, One is a textbook for principles of econ, and the other book is based on my blogging about money.

Nathan, Good points.

Alec, Money neutrality does not apply to cryptocurrencies because they are not technically “money” (not a median of account.)

Steve F

Oct 12 2017 at 7:20pm

Could it be that the “potential, actual” distinction regarding output is an illusion? What I’m getting at is that if output results from AS and AD — and those both result from the current state of affairs, like monetary and regulatory policy — shouldn’t potential output always equal actual output?

Comments are closed.