Categories:

Finance: stocks, options, etc.

Macroeconomics

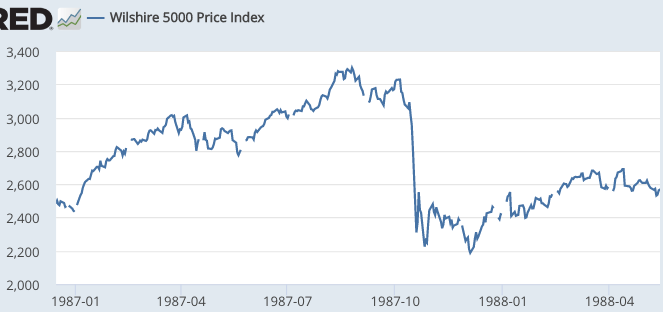

I have a new piece at The Hill discussing the 1987 stock market crash, as well as its implications for today’s economy:

The real lesson of 1987 is that all lessons are provisional, subject to revision as more time goes by and we gain a better understanding of the forces determining asset prices.

What looked in 1987 like a bursting bubble after a period of irrational exuberance, which was likely to trigger a recession, now looks like a period of irrational pessimism, which didn’t slow the economy at all.

READER COMMENTS

Garrett

Oct 23 2017 at 11:38am

1927’s market is viewed as irrational because of the Great Depression. 1987’s market is viewed as irrational because nothing happened. 2007’s market is viewed as irrational because of the Great Recession.

My takeaway: if stocks keep going up and we have a recession next year then 2017’s market will be viewed as irrational. If stocks crash and we don’t have a recession next year then 2017’s market will be viewed as irrational.

People simultaneously believe that markets are crazy and expect them to perfectly predict the future.

Grant Gould

Oct 23 2017 at 1:39pm

Perhaps “bubble” is not really an economic concept at all but a concept of the popular press that economists have unwisely adopted.

A “bubble” is a past time when the median investor remembers buying assets that he or she would soon afterward regret and would sell too early for too little.

Spencer

Oct 23 2017 at 1:39pm

[Comment removed for supplying false email address. Email the webmaster@econlib.org to request restoring your comment privileges. A valid email address is required to post comments on EconLog and EconTalk.–Econlib Ed.]

Scott Sumner

Oct 23 2017 at 3:29pm

Garrett and Grant, Good points.

Mark

Oct 23 2017 at 5:50pm

Wasn’t it Samuelson who said the stock market is so good at economic forecasting that it had successfully predicted 9 out of the last 5 recessions?

Of course this may not be that irrational. Sometimes type 2 errors are more dangerous than type 1 errors.

Larry

Oct 23 2017 at 9:21pm

At the NASDAQ level this works. At a sectoral l gel, I’m thinking not as much. Many/most of the tech firms are kaput.

Michael Sandifer

Oct 24 2017 at 8:58am

Scott,

I don’t think it’s a coincidence that both the Treasury market and the US stock market each behaved as if expecting a 1-2% recession in October of ’87. Asset markets around the world concurred.

I know you’ve stated that you think the drop in the stock indexes was too large to be explained by expectations of a relatively mild recession, but I point out that my story is very much consistent with what happened in 3 of the last 4 US recessions.

Starting with the Great Recession, the peak-to-trough drop in NGDP was about 3%. The S&P 500 lost over 50% of its value. In the 2001 recession, the S&P 500 lost more than 45% of its value, and the drop in NGDP was far milder. In the 1982 recession, adjusted for a lower P/E ratio, the drop in the S&P 500 was exactly what my model would predict.

In fact, my simple model predicts the relationship between pre-recession P/E, drop in NGDP, and drop in the S&P 500 for 3 of the last 4 recessions with some precision.

The 1991-’92 recession was deeper than asset markets predicted, but the Treasury market erred on the side of too much optimism to the exact same degree as the stock market, using my model. So markets were incorrect in that case, but the model held, as it really models market expectations.

The model is very consistent with market monetarist beliefs. It merely says that the percent dropin broad, representative stock index prices should be proportional to the percent drop in NGDP from trend, multiplied by the pre-shock P/E ratio of the index, adjusted for the fact that stock index prices won’t go to zero.

Why P/E? P/E is an indicator of expected rate of return. The inverse of the P/E ratio indicates expectations for near-term returns, which obviously loom larger than more distant returns. Hence, indexes with higher P/E’s will be hit harder by recessions.

Even if you continue to disagree, consider also that this simple approach also fits Great Depression data, in which the NGDP drop was an order of magnitude greater than in the Great Recession. It could be a coincidence, but how likely is that?

Scott Sumner

Oct 24 2017 at 11:23am

Larry, You said:

“Many/most of the tech firms are kaput.”

How is that relevant? Most lottery tickets are also “kaput”.

Michael, Again, if your theory were true then we’d see those 20% declines more often, not just once in 100 years.

bill

Oct 24 2017 at 1:02pm

I liked this from Mark: “the stock market is so good at economic forecasting that it had successfully predicted 9 out of the last 5 recessions”

That ties in really well with a previous post about recessions that didn’t happen because the Fed realizes that NGDP is slowing and reacts accordingly. And stock market investors appropriately realize that sometimes the Fed reacts and sometimes they miss it.

scott sumner

Oct 24 2017 at 5:37pm

Bill. Good point.

Michael Sandifer

Oct 25 2017 at 8:38am

Scott,

What frequency of 20%+ single day drops should we expect if my claim about the 1987 crash is correct?

True, there isn’t another example of a percentage change in a single day that’s really even close, but there were at least a few days during the tumult in 2008-09 in which circuit breakers were triggered, so for all we know it may have happened again otherwise.

https://en.wikipedia.org/wiki/List_of_largest_daily_changes_in_the_S%26P_500_Index

There were even some double digit daily percentage moves during the 2008-09 mess, despite circuit breakers.

If you notice on the list there, the biggest percentage single day changes have overwhelmingly come within the last 30 or so years.

Scott Sumner

Oct 25 2017 at 12:30pm

Michael, No, the most frequent big drops occurred during the 1930s.

Circuit breakers would not prevent a big drop in stocks.

You’d expect 100s of 20% drops if your theory was correct, because there are 100s of days with more important new information about the future course of NGDP than what occurred on October 19.

Michael Sandifer

Oct 25 2017 at 3:18pm

Scott,

Thanks for the correction on the 30s having the most large single day index declines. Apparently the data I linked to were too limited.

I have to admit to some respect for the fact that you don’t lurch easily toward a simple market monetarist explanation in this case.

That said, perhaps due to naivete, it seems to me that Greenspan was inadvertently sending signals about tightening to the markets, as a newly appointed chairman. This is one of the four prominent explanations I’ve seen for the crash, with the other three having to do with portfolio insurance/settlement date mismatches/programmed trading, talk about new taxes on M&A activity from the House Ways and Means Committee, and talk from the Treasury about strengthening the dollar.

Correct me if I’m wrong, but you don’t accept any of these explanations. My impression is it’s still largely a mystery in your mind.

Perhaps it will always be a mystery.

Michael Sandifer

Oct 25 2017 at 3:28pm

I should have mentioned that circuit breakers can limit losses on single days in the market, even though it may ultimately only delay the reaction of stock indexes to falling NGDP expectations, for example.

Michael Sandifer

Oct 25 2017 at 3:32pm

Scott,

I just found this survey from Robert Shiller that was taken during the period of the ’87 crash and over 1000 investors seem to concord with what you say about no significant news driving trading decisions on Black Monday.

http://www.nber.org/papers/w2446

Matthew Waters

Oct 25 2017 at 3:56pm

To look at P/E, it’s best to invert it and get the earnings yield. The earnings yield has roughly tracked the 10-year rate since 1980. There are two exceptions where the earnings yield was 2 percentage points below the 10-year yield:

1. Right before 1987 crash.

2. 1999-2000 tech bubble.

http://blogs.reuters.com/felix-salmon/files/2011/08/US_SP10YT0811_SC.jpg

I think it’s safe to say that it was the market being overvalued before the crash rather than undervalued after the crash.

A lot of examples in the article have the fallacy of not adding in interest over time. For example, coastal homes are above their 2005 price, yes. But 10 year bonds were yielding 4% in 2005. Even without compounding, a 10 year bond bought in 2005 is automatically up 40%. With compounding, that bond is up around 45-50%.

For SF, the median home price went from $895k in 2005 to $1.2m. That was only a 34% price increase versus 40% for a 10 year Treasury and putting coupon payments under a mattress. I have to guess SF is the best performing 2005-15 home market and others have done even worse compared to 10-year Treasuries.

Matthew Waters

Oct 25 2017 at 4:06pm

Here is the source of the SF home price.

https://www.investsf.com/updated-sp-case-shiller-home-price-index-for-san-francisco-metro-area/

To be fair, a full comparison would use several other variables. On the plus for housing as an investment, you get the imputed or actual rent. Plus the US government nicely subsidizes buying 80% of your house on margin. On the negative side, you have far higher transaction fees and carrying costs (property taxes and rents).

But the short of it is I saw a similar statement throughout the article: “Asset X was high, then crashed, but is now trading high again 10-20 years later.” If you’re starting your time frame before 2007, even Treasuries yield significant interest.

Comments are closed.