Here’s Bloomberg:

“We are in a pretty good place right now economically, but we’ve got a monetary policy that still seems like it is in the remnants of a Depression era,” Jes Staley, the chief executive officer of Barclays Plc, said in Davos, Switzerland, last week.

Perhaps he should replace “but” with “because”.

Bankers at the forum in the Alps sounded more worried about asset bubbles, and what happens when they pop, than an inflation rate that Fed officials have regarded as too low and meriting a go-slow policy.

“Bubbles are building,” Axel Weber, UBS Group AG chairman and former president of the German central bank, said in Davos. “The impact of this current monetary policy on markets, rather than just on inflation, is something central banks have to focus a bit more on at this point.”

The last time the Fed tried to pop a bubble was 1929. They succeeded.

“The issue is: Is the Fed nimble enough?” said Vincent Reinhart, chief economist at Standish Mellon Asset Management in Boston and a former senior Fed adviser. “They don’t give evidence of being data-dependent or making decisions meeting by meeting.”

This is a good point. One solution is to have the fed funds target follow something closer to a random walk. Don’t use quarter point increments—use all 100 basis points. And set the fed funds target at the preference of the median FOMC voter. The more that policy setting looks like a market-based approach, the more quickly we’ll get to an actual market-based approach.

There are few successful examples of a central bank smoothly warning markets it could shift to a more aggressive posture. The long shadow of the Fed’s 2013 Taper Tantrum cautions against abrupt moves. Yields on U.S. 10-year notes jumped by more than a percentage point over several weeks after then-Fed chief Ben Bernanke said it would start trimming its monthly bond purchase program.

This is a perfect example of why financial markets types should be kept far away from the Fed. To finance people, years like 1987, 1994, and 2013 loom large, as rising rates led to market turmoil. To macroeconomists, these years are utterly uneventful. Of course when it comes to monetary policy, it’s the macroeconomy that matters, not the financial markets. There was no “long shadow” in 2013; the long shadow of tight money occurred in 2008, when interest rates were falling. (That’s not to say the 2013 taper talk was appropriate—in retrospect it looks premature.)

Despite five rate increases under Yellen, who began the hiking cycle in late 2015, the Chicago Fed’s Financial Conditions Index is at the lowest levels since the early 1990s.

“We have had the opposite of a taper tantrum — a substantial net easing of financial conditions,” said Ethan Harris, head of global economics research at Bank of America. “The message of the Fed is starting to look a bit stale.”

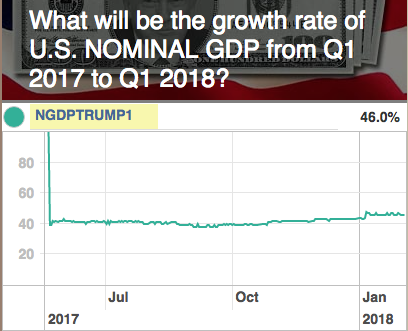

The financial conditions index is not particularly useful, but at least it’s not as bad as interest rates. Market participants do correctly intuit that the gradually rising rates don’t actually constitute money tightening. But they’d be better off relying on NGDP futures prices (which have also been trending up a bit in the Hypermind futures market.)

Comments are closed.